In this article, I will be going through the tip of Iceberg and provide more clarity on some of the building blocks in Financial Management paper (FM) or Strategic Financial Management (SFM) Paper which usually makes or break our concepts.

USING LIBOR:

Used in Foreign Exchange Exposure & Swaps at CA-FINAL level

Used as a Building block at CA- Intermediate level

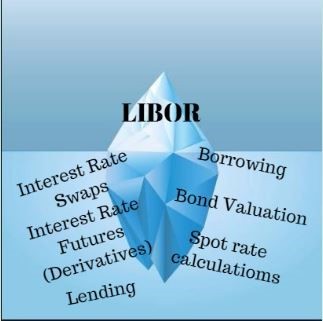

LIBOR or more broadly speaking Inter-Bank lending rates are most important interest rates in Finance. It is responsible for trillions of financial contracts which rely upon it for lending/borrowing rates. It is used in contracts for deciding rates on Mortgages, Other Loans, Inter-bank lending (Call money etc.) as it is also an Indicator of trust on the banking system which the public place.

In our course under the Strategic Financial Management Paper we have seen using LIBOR in many ways such as

- Foreign Exchange Exposures

- Interest Rate swaps

- Interest rate Futures(Derivatives)

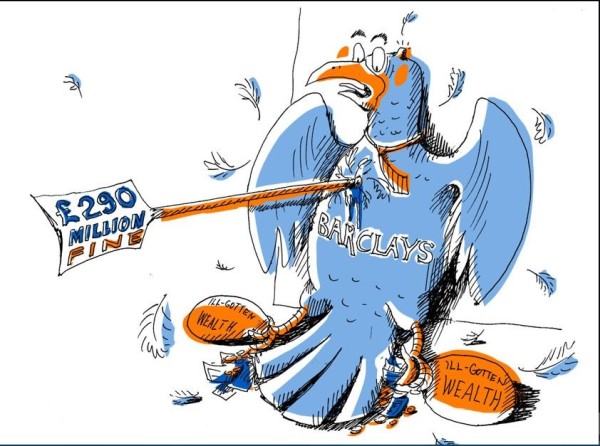

But many of you may not be aware of that the system which provides for LIBOR was held to be rigged and collusive.

|

What we are studying in our Books |

What actually is happening |

|

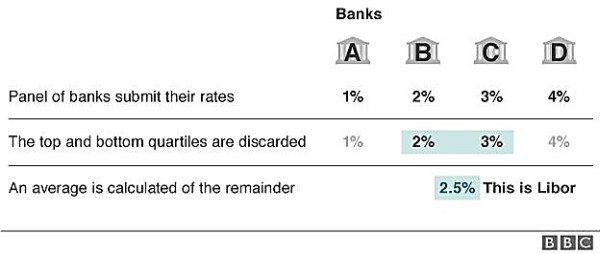

How is LIBOR calculated?

Picture Source: BBC |

Picture Source: Google It was suggested that Leading Banks had submitted false figures that results in influencing, the official Libor rate by forming a Cartel amongst themselves and make any rate they want. Since last 5 years Leading Banks such as Barclays, JP Morgan, Swiss bank UBS, Royal Bank of Scotland and Deutsche Bank have all been fined by financial regulators for this practise specifically cartel formation and market manipulation But the big blow came when in August 2015, former city trader Tom Hayes was convicted of conspiracy to defraud for manipulating Libor. |

End Result

- After the allegations came to light London government commissioned a major review of Libor and how it was set. Oversight of Libor was passed from the British Bankers' Association to the Intercontinental Exchange - ICE. Rates are now based on actual transactions for which records are kept.

- Another key change is that there are now specific criminal sanctions for manipulation of benchmark interest rates in the Law.

USING FLOATATION COST:

Used in Dividend Decisions Capital Budgeting at CA-FINAL level

Used in Cost of Capital at CA- Intermediate level

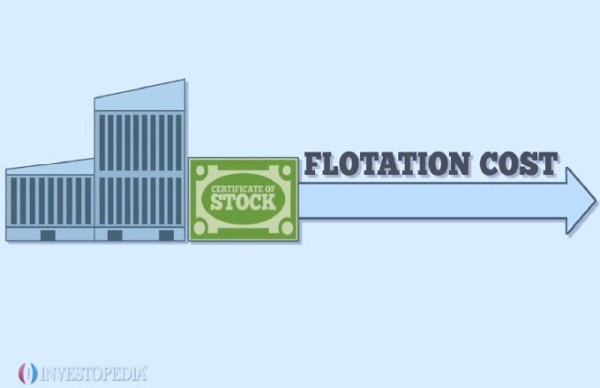

Picture Source: Investopedia

When a company raises new capital, it is generally seeking the assistance of Investment Bankers who themselves charge the company a fee based on the size and type of the offering. This is Flotation Cost. In the case of Debt or Preference share capital issue, such costs are very minimal. However, with equity issuance, these costs may be substantial and thus accordingly needs to be incorporated in the costs.

|

What we are studying in our Books |

What actually is done |

|

Whenever we are calculating cost of our equity capital we mostly used Dividend Discount Model or most commonly known as Gordon Model. And most probably whenever you have encountered with Flotation cost while issuing the shares you would have simply deducted it from the Price at which the shares were issued without actually knowing that this treatment is conceptually wrong and is there to calculate our Cost of Equity(Ke) in simple terms. As per Dividend Discount Model,

The problem with this approach is that the Flotation Costs are a cash flow at the initiation of the Project and affect the value of any Project by reducing the initial cash flow, Adjusting the cost of capital for Flotation costs are incorrect because by doing so we are adjusting the Present Value of Future cash flows by a fixed Percentage. |

What actually is done is also a recommended approach by the CFA institute for its member which later on take up the posts of Equity fund managers is To make the adjustment to the cash flows in the valuation computation. |

End Result

For Example

Correct Way

Consider a project that requires an initial cash outlay of Rs. 60,000 and is expected to produce a revenue of Rs. 10,000 each year for 10 years. And the Dividend next year is Rs 1, Current Price is Rs. 20 and growth rate of 5%. Flotation costs are 5% of the issuance.

Tax rate and cost of Debt(pre-tax) is 40% and 5% respectively. And the target weights are 0.6 and 0.4 for Equity and Debt.

Thus,

|

Costs |

Working |

WACC |

|

KD |

{5%(1-0.40)}*0.40 |

1.2% |

|

Ke |

(1/20*100+5%)0.6 |

6% |

|

Ko |

7.2% |

|

Ignoring FC we have a NPV of

= 69,591-60,000= Rs. 9,591

Considering FC we have a NPV of

= 69,591-60,000(1+5%)=Rs. 7,791

Wrong Way

But if instead of considering Flotation costs part of the cash flows, we had adjusted it in cost of equity like the traditional norms then our cost of capital would have been 7.3578% and thus it would have a NPV of

= 69,089-60,000=Rs. 9,089

- Thus our Investment would have had a higher NPV than what actually the NPV should have been which could lead to wrong Investment decisions.

- While the figures used in the example are for easy understanding, actual scenarios might have this difference in NPV in huge value ranging from lakhs to crores.

Thus why do we still have the wrong treatment in our text books?

The answer is because,

a. It is easier to demonstrate how costs of financing in a company change as a company exhausts its Retained Earnings and switches over to new stock issue.

b. It is difficult to identify particular financing specific to a project, using the adjustments in cost of equity makes things simple in general if specific costs can’t be allocated to it.

CAclubindia

CAclubindia