Cases where an employee work under two employer in a single financial year

Normally an employee is employed under employer during whole financial year and thus no problem arises in deduction of TDS from salary. In this case all information relating to income of employee is readily available with employer and computation task is easy to handle. However, complexity arise where employee work under two employer. This problem may arise in the following situations:

1. Where employee changes his job in the middle of year

2. Where employee is engaged in part time jobs or week end assignment

3. Where employee work under two employee simultaneously

Here, an attempt is made to explain the duties and responsibilities of employee and employer. Further this blog will explain you how to handle this situation.

More Than One Employer

Where an employee has more than one employer, he is required to furnish in Form No. 12B to one of the employers (as selected by the employee having regards to the circumstances of the case)the detail of salary due/received by him from one other employers.

Only after submission of information in Form No.12B, it becomes the obligation of the employer (to whom Form No.12B is submitted) to deduct tax at source after considering the information submitted by the employee.

For instance, if information is submitted in the month of October, only from October onwards, tax shall be deducted at the average rate determined after considering the details submitted in the Form No. 12B.

Case 1.

During the previous year 2015-16, Mr X is employed simultaneously by A Ltd.(salary: Rs.30,000) and B Ltd. (salary:Rs.42,000) on part-time basis. Mr X may select any of the two companies for deducting tax at source on aggregate salary.

Suppose, Mr X selects B. Ltd., then tax will be deducted as follows:

|

Tax deduction by A Ltd on salary paid by it. Rs. |

|

|

Tax salary by A Ltd. (Rs.30,000*12) |

3,60,000 |

|

Tax on taxable salary to be deducted at source by A Ltd. |

9,270 |

The above information pertaining to A Ltd will be submitted by Mr X to B Ltd in Form No.12B Ltdwill deduct tax on the aggregate salary as follows:

|

Tax deduction by B Ltd. Rs |

|

|

Taxable salary (Rs.30,000*12+Rs.42,000*12) |

8,64,000 |

|

Tax on taxable salary |

1,00,734 |

|

Less: Tax deducted by A Ltd. |

9,200 |

|

Tax to be deducted by B Ltd. |

91,464 |

Case 2:

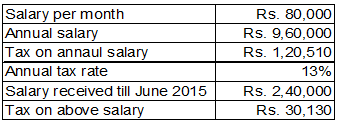

Mr Y is employed by C Ltd. Up to June 30,2015(salary being Rs.80,000 per month). On July 1,2015,he joins D Ltd. (salary being Rs. 95,000 per month). Tax will be deducted as source as follows:

|

Taxation deduction by C Ltd on salary paid by it Rs. |

|

|

Taxable salary by C Ltd. (80,000*3) |

2,40,000 |

|

Tax on salary deduction of source by C Ltd. (Tax will be calculated on monthly basis at annual average tax rate which is calculated as below:

|

30,130 |

The above information pertaining to C Ltd will be submitted by Mr Y to D Ltd. in Form No.12B. D Ltd. will deduct tax on the aggregate salary as follows(Mr Y should not select the old employer for deducting tax in respect of aggregate salary).

|

Tax deduction by B Ltd .Rs. |

|

|

Taxable salary (Rs. 80,000*3+ Rs.95,000*9) |

10,95,000 |

|

Tax on taxable salary |

1,58,105 |

|

Less: Tax deducted by C Ltd. |

30,130 |

|

Tax to be deducted by B Ltd. |

1,27,980 |

CAclubindia

CAclubindia