The clarifications issued in GST are being welcomed as they have the effect of resolving confusions and reducing litigation. However, sometimes the clarification tend to give rise to more disputes and more confusions. In this update, we wish to highlight the contradiction created by the recent clarification issued vide Circular No. 80/54/2018-GST dated 31.12.2018 with respect to inter-state movement of cranes, rigs, tools and spares and other machinery by a person on his own account for their supply of service. The language of the clarification is produced for the sake of easy understanding as follows:-

13.1 As per Circular No. 21/21/2017-GST dated 22.11.2017, it was clarified that no IGST would be applicable on such interstate movements of rigs, tools & spares and all goods on wheels. Doubts have been raised regarding applicability of GST on inter-state movement of machinery like tower cranes, rigs, batching plants, concrete pumps and mixers which are not mounted on wheels, but require regular means of conveyance (used by companies in Infrastructure business).

13.2 Any inter-state movement of goods for provision of service on own account by a service provider, where no transfer of title in such goods or transfer of goods to the distinct person by way of stock transfer is not involved, does not constitute a supply of such goods. Hence, it is clarified that any such movement on own account (not involving distinct person in terms of section 25), where such movement is not intended for further supply of such goods does not constitute a supply and would not be liable to GST.

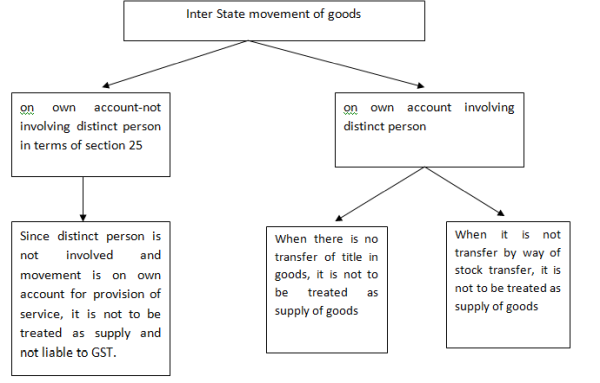

The clarification stated above can be presented as follows:

If we analyse the clarification, it is observed that the first line of the clarification given in para 13.2 indicates that if there is any inter-state movement of goods for provision of service on own account by a service provider, then the inter-state movement would not constitute supply of goods in following situations:-

- If the goods are being supplied to distinct person but there is no transfer of title in such goods.

- If the transfer of goods to the distinct person by way of stock transfer is not involved.

This indicates that the inter-state movement of machinery to distinct person, if there is no transfer of title or if there is no stock transfer does not constitute supply. However, the very next line of the clarification states that any movement on own account, not involving distinct persons in terms of section 25 would not constitute supply where the inter-state movement of machinery is not intended for further supply of goods. The wordings of the clarification in the first line say that the movement of goods would not constitute supply if there is no transfer or there is no stock transfer in case of distinct persons. However, the very next line excludes distinct persons for the purpose of inter-state movement of goods on own account and clarifies that such movement would not constitute supply. The language of the clarification is confusing and raises doubt as regards the intention of the government whether the clarification pertains to inter-state movement between distinct persons or not. The last line of the clarification that the inter-state movement of goods on own account not involving distinct person where such movement is not intended for further supply of goods is not to be considered as supply is absurd because practically if the distinct person is not involved, there cannot be supply on own account as two persons are necessary for any supply to take place. This can be explained with the help of an example-suppose Mr. A is registered assessee providing construction services in the State of Rajasthan. Mr. A wants to move machinery to Gujarat for a small project but Mr. A is not registered in Gujarat. In such a case, the last line of the clarification says that such movement of machinery to Gujarat by Mr. A who is registered in Rajasthan would not constitute supply. But, we say that there was no need to clarify this point as even otherwise, two persons (registrations) are required for making supply and Mr. A cannot supply machinery to himself. Taking the example further, if Mr. A has registration both in Rajasthan and in Gujarat, then in that case, it is clarified in the circular that if the title of machinery is not transferred to Gujarat registration or if the machinery is not sent as stock transfer, then such movement would not constitute supply. This clarification is beneficial as it seeks to clarify that mere movement of machinery between two registrations of a same person (called distinct person) cannot be reason to levy GST if there is no transfer in title to the goods or there is no stock transfer. However, the manner in which the clarification has been issued creates lot of confusion in the minds of assessee.

The content of this GST update is for educational purpose only and not intended for solicitation.

The author can also be reached at www.capradeepjain.com

CAclubindia

CAclubindia