Introduction:

Charging section of the CGST act only deal with collection of CGST. As per CGST Act 2017 there shall be levied a tax called 'Goods and Service Tax' on all the Intra state supplies of goods and services on the value determined u/s 15 of the CGST Act 2017. There are also such exclusion from levying CGST on which GST is levied by the Central government on the recommendation of the council.

However intra-state supply of alcoholic liquor for human consumption is outside the purview of CGST.

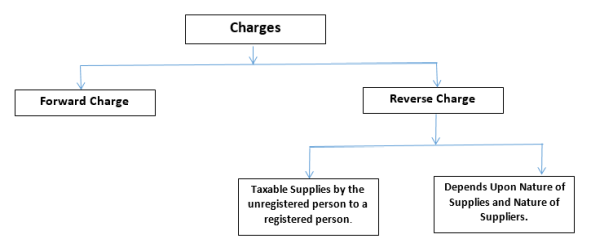

There are two types of Charges under GST.

1. Forward Charge: Section 9(1) deals with forward charge.

2. Reverse Charge: Section 9(3) and 9(4) deals with reverse charge.

What is Forward charge?

Forward charge or direct charge is the mechanism where the supplier of goods or services is liable to pay tax.

For example: -

- If a chartered accountant provided a service to his client, the GST will be payable by the chartered accountant.

- If a car manufacturing company sold some auto parts to a trader and collected tax from the trader, the manufacturing company remits the tax to the government.

Note: Under the current tax system, most transactions are covered under the forward charge mechanism.

Exclusion from GST:-

CGST on supply of following items has not been levied immediately. It shall be levied with effect from such date as may be notified by the Government on the recommendation of the GST council:

- Petroleum crude

- High speed diesel

- Motor spirit (commonly known as petrol)

- Natural gas

- Aviation turbine fuel.

Rates of CGST under CGST Act 2017.

Rate of CGST are 0%, 0.125%, 1.5%, 2.5%, 6%, 9%, 14%. Maximum rate of CGST will be 20%.

What is Reverse Charge?

In reverse charge liability to pay tax by the recipient of goods or services or both instead of supplier of such goods or services or both. The purpose of applying reverse charge is to increase compliance by unorganized sectors, such as transport, and to increase tax revenues.

There are two type of reverse charge in GST Law.

First is dependent on the nature of supply and/or nature of supplier. This scenario is covered by section 9 (3) of the CGST Act 2017.

Government has notified the following categories of services wherein whole of the CGST shall be paid on reverse charge basis by the recipient of services:

- Supply of Services by a goods transport agency (GTA)

- Services supplied by an individual advocate including a senior advocate.

- Services supplied by an arbitral tribunal.

- Services provided by the way of sponsorship.

- Services provided by Central Government, State government, Union territory or local authority to a business entity.

- Services provided by the director of a company or body corporate to the said company or body corporate.

- Services provided by the insurance agent.

- Services provided by the recovery agent.

- Services provided by the author, music composer, photographer, artist.

Note: For the detailed study of the notified services refer Notification No. 13/2017 Central Tax (Rate) Dated 28.06.2017 or download the notification from the link http://www.cbic.gov.in/resources//htdocs-cbec/gst/51_GST_Flyer_Chapter12.pdf;jsessionid=11AC72B209AB69893D73757963475D79

Second scenario is covered by section 9 (4) of the CGST Act where taxable supplies by any unregistered person to a registered person.

Intra-state supply of taxable goods or services or both by an Unregistered supplier to a registered person are exempt from CGST provided the aggregate value of such supplies of goods or services or both by the registered person from any or all the unregistered suppliers does not exceed Rs. 5000 in a day.

Example 1: Mr. P, a manufacturer, buys stationery worth Rs. 1000 from a shop near to his plant, which is not registered under GST. In this case Mr. P would not be liable to pay GST on such purchase because total supplies from unregistered persons shall not exceed Rs. 5000 on that day.

Example 2: Mr. P, a manufacturer, buys stationery worth Rs. 1000 from Mr. J and worth Rs 4000 from Mr. K, both are not registered under GST. In this case Mr. P would liable to pay GST on such purchase because total supplies from unregistered persons shall exceed Rs. 5000 on that day.

POINT TO BE CONSIDERED FOR THE RCM:-

1. Registration Compulsory to pay tax under reverse charge.

2. A supplier cannot take ITC of GST paid on goods or services used to make supplies on which the recipient is liable to pay tax.

3. Self-invoicing is to be done.

Who is Electronic commerce operator?

Electronic commerce operator display products or services which are actually supplied by some other persons to the consumer on their electronic portal. The consumer buy such goods or services through these portals. On placing the order for a particular product the actual supplier supplies the product or services to the consumer. The price for the product or service is collected by the ECO from the consumer and passed on to the actual supplier after the deduction of the commission by the ECO.

In short 'Electronic commerce operator' means any person who owns, operates or manages digital or electronic facility or platform for electronic commerce.'

For Example: Amazon, Flipkart, Myntra, Shopclues are E-commerce operator because they are facilitating actual suppliers to supply Goods through their platform.

What is Electronic commerce?

Electronic commerce' means the supply of goods or services or both, including digital products over digital or electronic network.

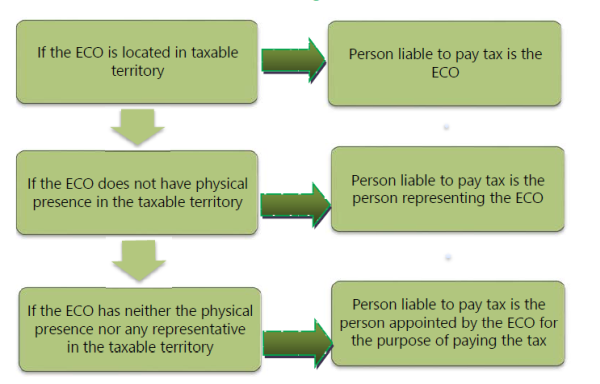

Persons liable to pay GST when services supplied through ECO:

- The Government may, on the recommendations of the GST Council, by notification, specify categories of services the tax on Intra-State supplies of which shall be paid by the electronic commerce operator if such services are supplied through ECO, and all the provisions of this Act shall apply to such electronic commerce operator as if he is the supplier liable for paying the tax in relation to the supply of such services.

- Where an electronic commerce operator (ECO) does not have a physical presence in the taxable territory - The person representing ECO shall be liable to pay tax:

- Where an electronic commerce operator (ECO) does not have a physical presence in the taxable territory and also he does not have a representative in the said territory - In such case ECO shall appoint a person in the taxable territory for the purpose of paying tax and such person shall be liable to pay tax.

Disclaimer: The contents of this document are solely for informational purpose. It does not constitute professional advice. Neither the authors accept any liabilities for any loss or damage of any kind arising out of any information in this document nor for any actions taken in reliance thereon.

CAclubindia

CAclubindia