Capital Budgeting

All of us, at one point in time or another, have prepared a budget in one form or another. The reason for this is primarily to find out if we can afford the costs/investments, where to get the money from, and how much would it give in return. In fact many of the households manage domestic expenses by way of having their own budgets.

In the corporate world, the businesses do the same thing. They budget for 'capital expenditure'. In simple words, this is called 'Capital Budgeting'. In the west, capital budgeting is also called as 'Investment Appraisal'.

In this article let us look at the fundamentals of capital budgeting for beginners.

Let us assume that I owe you $1,000,000. I offer you two options of repayment:

- Option 1: Repay $1,000,000 today or

- Option 2: Repay $1,000,000 after one year.

Which option will you choose?

Obviously $1,000,000today right? Because $1,000,000 received today can buy much more than what $1,000,000 can buy after one year.

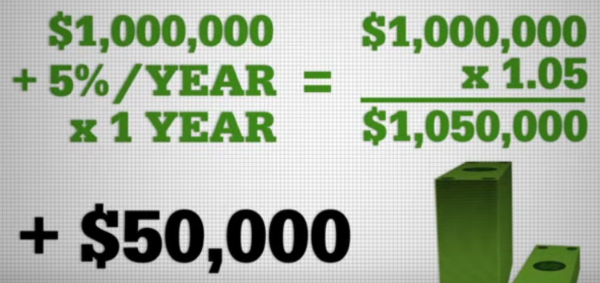

Moreover, if you invest the $1,000,000 received today in a bank deposit at 5% interest per annum, you will end up getting $50,000 as interest during the one year period.

In other words, the value of $1,000,000 falls as time progresses. This is called 'Time Value of Money'

In simple words, the Time Value of Money principle states that one dollar tomorrow is worth LESS than one dollar today.

Therefore from an investment perspective, any money spent or received in the future, is worth much than what it is worth today. In order to factor in this 'reduction in the worth of money', future cash flows are discounted to their present value (today's value) in order to take a meaningful decision.

This discounting of future cash inflows to the present day, and the future cash outflows to the present day, is called Discounted Cash Flow Technique or simply 'DCF'. Some professionals also call it NPV Analysis since you are netting off the present value of inflows and present value of outflows.

In the next article we will see how you can arrive at an NPV Analysis using a simple formula

The author is a Chartered Accountant, a Certified Public Accountant (CPA), a Certified Information Systems Auditor (CISA), and a Chartered Management Accountant (ACMA, UK) having close to a decade's experience in teaching and training students for professional examinations.

CAclubindia

CAclubindia