Bahubali is a title character in a hugely popular Indian movie. This warrior hero, amidst managing his internal emotions and external aberrations, demonstrates highly innovative combat skills at the battlefield.

Today, an Indian tax paying individual is a Bahubali in this own way. By fighting with the complexities of archaic direct tax law, demonstrating innovative tax planning and savings skills, he has been effectively managing the compliances over 50 years now.

Charging section, definitions, residential status, exempted income, perquisites, allowances, statutory deductions, Chapter VIA deductions, rebates, tax rates, forms, returns, advance tax, withholding tax, assessments, refunds; if an individual has to dissect all these from the Income tax act and file his tax returns, he has to be a Bahubali.

Some, who are adventurous, get in to it and become honest tax payers of this country. Rest, happily watch others playing this role and enjoy the movie.

This is the reason why in a nation with 1.2 billion people only 12 mil are tax paying individuals and of which most of them are people earning income from salaries. If the provisions of tax withholding through employer were not existing then these numbers would have been drastically lower.

The employers also have to go through a lot of agony to meet the tax intricacies in the form of structuring the salaries to its employees, ensuring tax compliances, documentation, filing returns, handling assessments, managing notices, filling appeals and so on, leading to increased compliance costs and impacting business performance.

Katappa is another interesting character in the movie. The only thing he knows is being loyal to the throne and following the orders of his masters. He does not have any family complications, wears a pretty simple attire, eats simple food, overall a critical, but jolly good character.

Typically this is how a common tax payer of this country would like to be, when it comes to paying taxes, for nation building. Engulfed with several personal and official matters to manage on a daily basis, an Indian tax payer does not want to add more woes in the form of complex tax compliances and fears associated with its non compliance. He is more than willing to be a loyal tax payer and comply with the laws of the land and be Katappa in his own ways, provided the law allows him to be so.

Income from Salary, the income which matters most to the common man and also to the tax administration. Hence lets focus on how this law should look like so that the Katappa of our world, embrace it whole heartedly and thereby helping the nation to build better tax base and tax collections

Below is the most ambitious narration of the tax structure. Focus is more on the change principles and not much on the technical nuance.

Categorization of benefits and its taxability.

- Statutory Benefits

- Non Statutory Facilities

- Salary & Other Emoluments

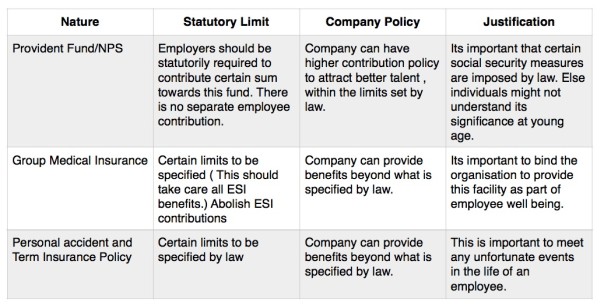

1. Statutory Benefits: (Employer to provide)

The law should provide for below benefits to the employees by employers. These spends should be allowed as business expenditure and non taxable in the hands of the employees.

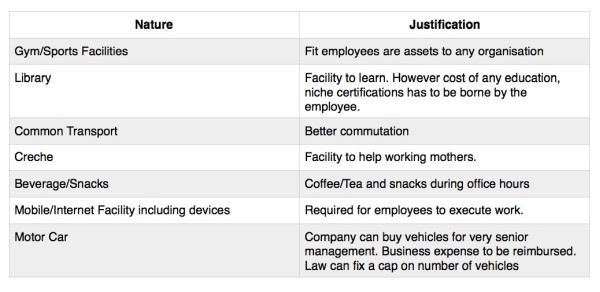

2. Non Statutory - Facilities (Employer may provide)

As part of business operations, organization should be allowed to provide certain employee benefits. Such benefits should facilitate better employee morale and performance at workplace. Hence they are to be treated as business expenditure and not as perquisites taxable in the hands of employees.

3. Salary and any other emoluments: (Taxable as Income from Salary for employees)

Salary is the compensation the employee gets monthly. Companies to keep other emoluments as less as possible in number and specific to its business needs.

a. Salary: Single component no structuring

b. Emoluments (Cash or Kind): Company based on its style of operations might provide different emoluments in the form of allowances or other perks, such as night shift, bonus, festival bonus, shares based payments, food allowance, joining bonus, leave encashments, retrenchment compensation, retirement bonus, referral bonus, all gifts & rewards , uniform allowance, books and periodicals allowance, notional interest on interest free loans etc.

c. Deduction: In a normal situation employees will see only ONE deduction in their payslip, that is towards Income Tax.

d. Tax Rate: Tax rate should be pretty simple and low. Something like 10% flat irrespective of income earned. There is a need to provide basic tax exemptions limits. Ideally Rs. 30,000 per month or Rs. 3.6 lac per annum should help keep low income earning individuals out of tax net. No concept of cess, surcharge and other additional tax slabs. If super rich needs to taxed at higher rate, that can be debated.

Now imagine how the payslip and tax would look like in this scenario

Payslip (Without any specific emoluments)

1 Income more than Rs.30000/-per month attract Income Tax at 10%.

In a nutshell,

- Lower tax rate, simplified salary definition

- Retirement, Risk & Medical, company will take care

- Only deduction on payslip is tax, unless you break a company property intentionally.

- No tax planning, no documentation, no proof submission, no bills submission.

- You manage your housing, investments, personal expenses and savings as per your needs.

- Associated laws such as Bonus, Gratuity, ESI, Profession tax, would no longer be relevant.

- Salary taxation law would be a 2 page handout.

Isn't this the law which everyone would feel like complying with?

Instead of making people, resources, infrastructure, Judiciary, tax advisors, professionals run behind 1% tax compliance; can we divert all these resources to reduce 99% non compliance rate.

We are tired of living the life of Bahubali. Can someone kill the Bahubali in us by bringing in simpler tax laws and help us to become Katappa, a loyal tax paying citizen of this country.

CAclubindia

CAclubindia