Social Welfare Surcharge @10% shall be levied on imported goods with effect from 2nd February, 2018, under clause 108 of the Finance Bill, 2018

What is meant by Baggage?

a. It is the luggage of the passenger travelling by air or sea from one country to another

b. It also means all dutiable goods imported by a passenger or a member of crew in his/her baggage

c. Baggage INCLUDES unaccompanied baggage (except where they are specifically excluded) but DOES NOT include motor vehicles

What is Unaccompanied Baggage?

a. It is the baggage which is not carried by the passenger at the time of her/his travel but sent before or after arrival

b. Time limit if the baggage is received before arrival: up to 2 months before arrival, or within such period (not exceeding 1 year) as allowed by Asst/Dy Commissioner of Customs (due to unavoidable circumstances)

c. Time limit if the baggage is received after arrival: 1 month of her/his arrival or such other period as may be allowed by Asst/Dy Commissioner of Customs

What are Green & Red Channels?

a. Green channel means if a person does not have any dutiable goods, he can go through it without undergoing any check, along with baggage. Hence no duty is applicable

b. Red channel means if a person is carrying dutiable goods, he should pass through it and submit declaration under section 77 mentioning the contents of the baggage to the proper officer for clearance and his baggage can be inspected by customs authorities

Determination of rate of duty & tariff valuation when dutiable goods are carried

a. Rate of duty & tariff valuation, if any, applicable to baggage shall be the rate & valuation in force on the date on which declaration is made u/s 77

b. Rate of duty on baggage is 35% + 2% EC + 1% SHEC = 36.05%

c. No additional customs duty u/s 3(1) or special CVD u/s 3(5)

Exemption:

1 laptop computer imported into India by a passenger of age of 18 years or above (other than member of crew) is exempted from whole of basic customs duty

Temporary detention of baggage – sec 80

The proper officer may detain baggage which contains any article which is dutiable or import of which is prohibited and in respect of which a true declaration has been made u/s 77. He may also do so, at the request of the passenger for returning to the passenger either

- At the time the passenger is leaving India or

- Through any other passenger authorized by the passenger & leaving India or

- As a cargo consigned in passenger’s name

Bona fide baggage exempted from duty – sec 79

The proper officer may pass free of duty

a. Any article in the baggage of passenger or member of crew in respect of which he is satisfied that it has been in his/her use for such minimum period as may be specified

b. Any article in the baggage of passenger in respect of which the officer is satisfied that it is for the use of passenger or his family or is a bona fide gift/souvenir, provided the value does not exceed the limit specified in the rules

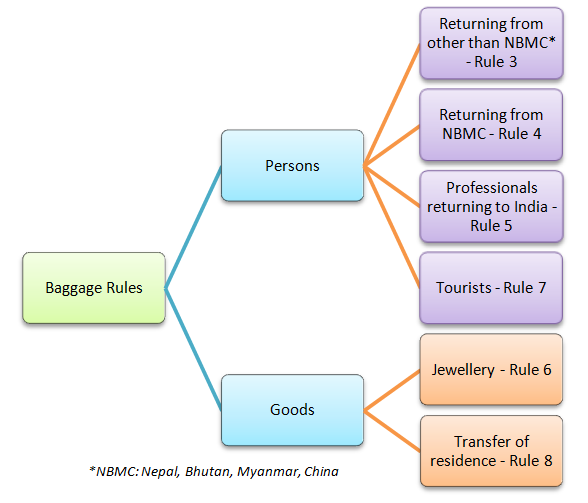

An Abstract of Baggage Rules

The provisions of baggage rules can be broadly classified into the following:

1. Provisions relating to persons coming into India

2. Provisions relating to goods brought into India

General Free Allowances for Passengers – Rule 3 & 4

|

Particulars |

Age <10 yrs |

Age 10 yrs or more |

||

|

Stay <=3 days |

Stay >3 days |

Stay <=3 days |

Stay >3 days |

|

|

Passenger returning from any country (other than NBMC) except by land route mentioned in Annex IV |

Up to Rs.3,000 |

Up to Rs.17,500 |

Up to Rs.17,500 |

Up to Rs.45,000 |

|

Passenger returning from any country (other than NBMC) by land route |

Nil |

Up to Rs.1,500 |

Nil |

Up to Rs.6,000 |

|

Passenger returning from NBMC other than by land route |

||||

|

Passenger returning from NBMC by land route |

Nil |

Nil |

Nil |

Nil |

Notes:

a. The above exemption limits are not applicable to articles which are mentioned in Annex I

b. Free allowance shall not be allowed to be pooled with free allowance of any other passenger

c. Used personal effects (excluding jewellery) required for satisfying daily necessities of life are not taxable

For example, Ms. X, aged 30 years, brought the following while returning to India from US after 6 days of stay:

1. Personal effects like clothes etc valued at Rs.35,000

2. A personal computer bought for Rs.60,000

3. A laptop computer bought for Rs.90,000

What is the amount of duty payable?

Answer:

|

Particulars |

Value Rs. |

Taxable Amt Rs. |

Remarks |

|

Personal effects |

35,000 |

Nil |

Exempt |

|

Personal computer |

60,000 |

60,000 |

|

|

Laptop computer |

90,000 |

Nil |

Exempt |

|

Sub Total |

60,000 |

||

|

Less: General Free Allowance u/r 3 |

45,000 |

||

|

Baggage taxable |

15,000 |

||

|

Duty payable |

5,408 |

@36.05% |

|

Annexure I

The articles mentioned in Annex I (to which exemption under rule 3 & 4 is not applicable) are:

a. Fire arms, cartridges of fire arms exceeding 50

b. Cigarettes exceeding 100 or cigars exceeding 25 or tobacco exceeding 125 gm

c. Alcoholic liquor or wines in excess of 2 ltr

d. Gold/Silver, in any form, other than ornaments

e. Flat Panel (LCD/LED/Plasma) Television

Annexure IV

Land routes mentioned in Annex IV (for the purpose of rule 3 & 4) is:

a. Amritsar: Amritsar Railway Station, Attari Road, Attari Railway Station, Kharla

b. Baroda: Assara Naka, Khavda Naka, Lakhpat, Santha Naka, Suigam Naka

c. Delhi: Delhi Railway Station

d. Ferozpur District: Hussainiwala

e. Jodhpur: Barmer Railway Station, Munabao Railway Station

f. Baramullah District: Adoosa

g. Poonch District: Chakan-da-bagh

Professionals returning to India – Rule 5

An Indian passenger who was engaged in his/her profession abroad is allowed clearance free of duty up to the following limits:

|

Particulars |

Used household articles |

Professional equipment |

|

Indian passenger returning after at least 3 months |

Rs.12,000 |

Rs.20,000 |

|

Indian passenger returning after at least 6 months |

Rs.40,000 |

|

|

Indian Passenger returning after a stay of minimum 365 days during the preceding 2 years on termination of his/her work & who has not availed this concession in the preceding 3 years |

Used household articles & personal effects (in possession and use abroad of the passenger or her/his family for at least 6 months), and which are not mentioned in Annex I, II or III, up to an aggragate value of Rs.75,000 |

|

Notes:

i. The above allowance is in addition to allowances given under rule 3 or 4

ii. Family includes all persons who are residing in the same house & forming part of same domestic establishment

iii. Professional equipment means

Portable equipments, instruments, apparatus & appliances required in his/her profession by a carpenter/plumber/welder/mason and the like and shall not include items such as cameras, cassette recorders, dictaphones, personal computers, typewriters & other similar articles

For example, Mr. Y, CA, Indian resident worked in Australia for 4 months and brought with him the following items on his return to India:

1. Personal effects valued at Rs.1,00,000

2. Professional equipments worth Rs.65,000

3. Household articles of Rs.40,000

4. A laptop worth Rs.80,000

What is the duty payable?

Answer:

|

Particulars |

Value Rs. |

Taxable Amt Rs. |

Remarks |

|

Personal effects |

1,00,000 |

Nil |

Exempt |

|

Professional equipments |

65,000 |

65,000 |

|

|

Household articles |

40,000 |

40,000 |

|

|

Laptop computer |

80,000 |

Nil |

Exempt |

|

Sub Total |

1,05,000 |

||

|

Less: General Free Allowance u/r 3 |

45,000 |

||

|

Less: Allowance u/r 5 |

32,000 |

(PE: 20,000 + HA: 12,000) |

|

|

Baggage taxable |

28,000 |

||

|

Duty payable |

10,094 |

@36.05% |

|

Annexure II

Articles mentioned in Annex II (to which exemption under rule 5 is not applicable) are:

a. Color/monochrome television, Digital video disc player, Video home theater system, Music system

b. Dish washer, Air conditioner, Domestic refrigerators of capacity above 300 ltr or its equivalent, Deep freezer, Microwave Oven

c. Video camera or the combination of any such video camera with one or more of the following: Television receiver, Sound recording/reproducing apparatus, Video reproducing apparatus

d. Word processing machine, Fax machine, Portable photocopying machine

e. Vessel, Aircraft

f. Cinematographic films of 35mm & above

g. Gold/silver, in any form, other than ornaments

Annexure III

Articles mentioned in Annex III (to which exemption under rule 5 is not applicable) are:

a. Video cassette recorder/player, Video television receiver or video cassette disk player

b. Washing machine

c. Electrical or LPG cooking range

d. Personal computer (desktop), laptop computer (notebook)

e. Domestic refrigerators of capacity up to 300 ltr or its equivalent

Tourist – Duty free allowance – Rule 7

A Tourist arriving in India shall be allowed clearance free of duty articles in her/his bona fide baggage to the extent of the following:

|

Case |

Duty free allowance |

|

Tourists of Indian origin (other than by land routes specified in Annex IV) |

i) Used personal effects & travel souvenirs, if -For personal use -Re-exported when tourist leaves India (other than those consumed during stay) ii) Articles as allowed under rule 3 or 4 |

|

Tourists of foreign origin (other than Pakistani origin coming from Pakistan) by air |

i) Used personal effects ii) Articles (other than those mentioned in Annex I) up to Rs.8,000 for personal use or as gifts/souvenir if carried with the person or in accompanied baggage |

|

Tourists of

|

i) Used personal effects ii) Articles (other than those mentioned in Annex I) up to Rs.6,000 for personal use or as gifts/souvenir if carried with the person or in accompanied baggage of the passenger |

Notes:

Tourist means

a. One who is not normally resident in India,

b. who enters India for a stay of not more than 6 months in the course of any 12 months period,

c. for legitimate non-immigrant purposes such as touring, recreation, sports, health, family reasons, study, religious pilgrimage or business

For example, Ms. A, tourist of UK origin, arrives in India carrying the following items:

1. Used personal effects valued at Rs.30,000

2. Articles for personal use (other than those mentioned in Annex I) worth Rs.8,000

What is the duty liability?

Answer:

|

Particulars |

Value Rs. |

Taxable Amt Rs. |

Remarks |

|

Used personal effects |

30,000 |

Nil |

Exempt |

|

Articles of personal use |

8,000 |

8,000 |

|

|

Sub Total |

8,000 |

||

|

Less: Allowance u/r 7 |

8,000 |

||

|

Baggage taxable |

Nil |

||

|

Duty payable |

Nil |

||

Jewellery – Duty Free Allowance – Rule 6

A passenger returning to India having resided abroad for more than 1 year shall be allowed clearance free of duty jewellery in his/her bona fide baggage to the extent of following:

- Gentleman passenger: Rs.50,000

- Lady passenger: Rs.1,00,000

For example, Mr. P, an Indian entrepreneur, went to Germany to explore new business opportunities on 1/1/2014. The following details are submitted by him on his return to India on 31/1/2015:

1. Used personal effects worth Rs.1,00,000

2. Music system worth Rs.45,000

3. Jewellery brought for Rs.50,000

What is the duty liability?

Answer:

|

Particulars |

Value Rs. |

Taxable Amt Rs. |

Remarks |

|

Used personal effects |

1,00,000 |

Nil |

Exempt |

|

Music system |

45,000 |

45,000 |

|

|

Jewellery |

50,000 |

50,000 |

|

|

Sub Total |

95,000 |

||

|

Less: General Free Allowance u/r 3 |

45,000 |

||

|

Less: Allowance u/r 6 |

50,000 |

(stay > 1 year) |

|

|

Baggage taxable |

Nil |

||

|

Duty payable |

Nil |

||

Transferring residence to India – Rule 8

A person transferring her/his residence to India shall be allowed clearance free of duty, in addition to allowance under rule 3 or 4, articles in her/his bona fide baggage to the extent of the following:

a. Used personal & household articles including articles listed in Annex III (but not listed in Annex I & II)

b. Jewellery to the extent mentioned in Rule 6

Conditions:

a. Minimum stay of 2 years immediately preceding the date of her/his arrival on transfer of residence (shortfall of up to 2 months in stay abroad can be condoned by Asst/Dy Commissioner of Customs, if early return is on account of terminal leave or vacation being availed or any other special circumstances)

b. Total stay in India on short visit during 2 preceding years should not exceed 6 months (Commissioner of Customs may condone short visits in excess of 6 months in deserving cases)

c. Passenger has not availed this concession in the preceding 3 years

Note:

Jewellery brought back which was taken earlier by the passenger or her/his family from India shall be allowed clearance free of duty, if Asst Commissioner of Customs is satisfied

For example, Ms. S, an Indian citizen, residing in London since last 3 years, has transferred her residence to India. On arrival, the details given by her are as follows:

1. Used personal and household articles worth Rs.3,00,000

2. Domestic refrigerator of capacity 250 ltr worth Rs.25,000

3. Jewellery worth Rs.90,000

4. LED TV worth Rs.50,000

Compute duty liability assuming that she has not visited India during these 3 years.

Answer:

|

Particulars |

Value Rs. |

Taxable Amt Rs. |

Remarks |

|

Used personal & household articles |

3,00,000 |

Nil |

Exempt |

|

Domestic refrigerator |

25,000 |

25,000 |

|

|

Jewellery |

90,000 |

90,000 |

|

|

LED TV |

50,000 |

50,000 |

|

|

Sub Total |

1,65,000 |

||

|

Less: General Free Allowance u/r 3 |

45,000 |

||

|

Less: Allowance u/r 6 |

90,000 |

||

|

Less: Allowance u/r 8 |

25,000 |

||

|

Baggage taxable |

5,000 |

||

|

Duty payable |

1803 |

@36.05% |

|

Application of baggage rules to the members of the crew – Rule 10

a. Provisions shall apply to crew members engaged in foreign going vessel or aircraft for import of their baggage at the time of final pay off on termination of their engagement or at the time of returning of the aircraft from foreign journey

b. However, a crew member shall be allowed to bring items like chocolates, cheese, cosmetics & other petty gift items for their personal/family use, the value of which shall not exceed Rs.1,500

CAclubindia

CAclubindia