The Asian equity market have started back it mad bull run from the past 2 months starting from September 2010.Pockets have filled up with soaring profits from lower level buyouts. The phase of the bull have so high that every one If we rewind back to the phase of 2008 when recession clouds were hanging over the world market, no body dreamt of that within 2 years time frame the Dow Jones , Nikke,Hangseng, Nifty all will rose up and scale back to 2008 January levels. I will not go with the traditional ways of identifying and elaborating the stories of growth juts like the famous speculators does. What I will try to show you the real growth behind the numbers and quarter results and vague speculators games.

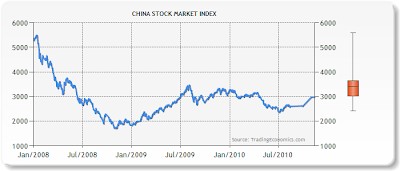

The below chart shows the bull run of the Indian and Chinese stock markets.

Standing on November 2010 its quite impossible to figure out what have really changed in the investors mind after taking lessons from the recession of 2008.We have again pumped up thousand billons of liquidity in the world market irrespective of cautious investment approach. In the era of 1980 and 1990 world investors pumped billion dollars in to Developed economies and made their profits gallop like an horse. In the period of 2000 the same liquidity changed its hands and came galloping to emerging economies .Emerging economies consists of BRIC put particular focus of investments was towards Asian Economies. The reason for the sudden shift from the traditional ways of investments strategy was that these developed economies came to stagnant phase of generating ROI. One fine morning the whole world turned the eyes towards Asian economies and its immense potentiality of growth. In 1980 India and China were each the recipient of 0.1% of global foreign direct investment (FDI). By 2008 India had welcomed 2.4% of overall FDI, China 6.4%.Today we find magnetic attraction of liquidity and other technical knowhow by India and China alone. In this article I will try to present the brief growth opportunities awaiting for Indian Economy with little bit of touch of Chinese economy. The US expanded its bilateral trade with India and China. U.S. merchandise exports to India quadrupled between 2002 and 2009 to $16.4 billion, while U.S. services exports increased from $3.3 billion in 2002 to more than $10.5 billion in 2008,

According to the Department of Industrial Policy and Promotion (DIPP) of Indias Ministry of Commerce and Industry, FDI flow into railway-related components was USD76.7 million from April 2000 to August 2009, a meager 0.08 percent of the total. This ranked the sector 47th among all the sectors that received FDI during the same period. Electrical multiple unit (EMU) trains and high-power electric locomotives loom as the next big investment themes in Chinese infrastructure. Urbanization requires more high-speed passenger lines, which, in turn, will create strong demand for EMU. China will experience an influx of EMU trains in the next three to four years, with around 800 sets expected to be in operation by 2012, up from 176. Indian railway is going to be the next hot destination of FDI investments Forty-six percent of FDI flow into India has been captured by five sectors: services, computer software and hardware, telecommunications, and construction, in this order. Power-related projects account for 4 percent, while port-related projects, another area were India needs a lot of improvement, ranked 18th with 1.5 percent of total FDI. When I found the flow of liquidity being absorbed after 2008 recession I find astonishing magnetic power attraction of liquidity by India and China alone. More than 60% of the funds included in the various stimulus packages introduced by emerging economies during 2008 were committed to infrastructure-related spending in 2009. China and India led the way, with 88% and 83%, respectively. In the next ten years emerging economies will spend between USD15 trillion and USD20 trillion on infrastructure projects. The China and Indian health sector will draw the most highest amount of Global liquidity and will provide immense growth of investments. China, for example, increased the number of vaccines included in its national immunization program from 5 to 15 in 2008 and boosted its budget for research and development from USD75 million to USD400 million. Indian and Chinese education sector will be next un-trapped huge potential investment destination. From 2013 to 2020, China will focus on implementing policies such as free primary education in rural areas, where 737 million. China economy is already heated up and process of cooling it is still on the way .In that term Indian economy has a long way to go. It bulls have just started warming up for the bull rally.

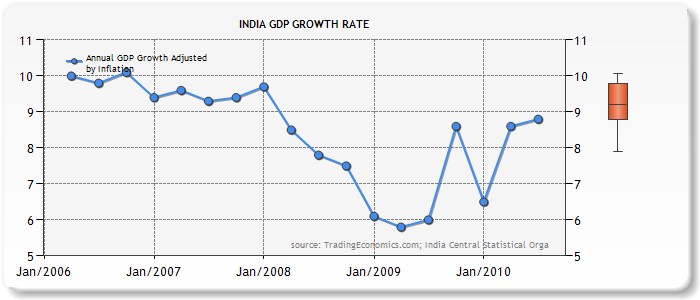

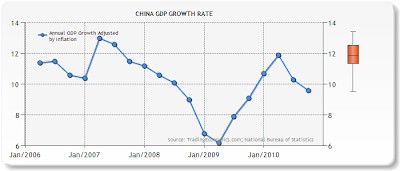

The below chart shows the Growth of the GDP of India and China from 2006

India recorded a GDP growth of 7.4% in 2009-10. It has been further consolidated in the current fiscal year with growth in the first quarter estimated at 8.8 per cent. This is in line with the GDP projections of 8.5 0.25% growth in 2010-11, made in the Economic Survey. The recovery is broad based with growth improving in all the three sectors, industry, services and agriculture. The pick up in investment growth in 2009-10 seems to be continuing in the first two quarters of the current fiscal. There are also signs of consumption growth moving towards its trend rate. The recovery is led by industry and with improved growth in services. The partial restoration of the tax cuts, compression in expenditure and revenue from 3G auction and disinvestment will help India in meeting our fiscal targets for the current year. This makes the Indian economy more prunes to investments as less fiscal burden on its shoulders. In the coming years the Indian economy is poised for more growth due to radical policy changes like a nutrient based fertilizers subsidy regime culminating in direct transfers to farmers at a later date; flexible petroleum pricing policy with levels of subsidy calibrated to international crude prices; public expenditure management; a new Direct Tax Code; and progress towards goods and services tax. Among all these the biggest boost will be the New Direct Tax Code which will increase the per-capita savings rate of Indian households which is currently pegging at 36.6% climbing from 28.4%.The new GST regime will also make the Indian trade practices left with huge margin of profits and investments surplus. The medium term Fiscal Policy Statement 2010-11 has outlined a decline in fiscal deficit to 4.8% of GDP in 2011-12 and 4.1% of GDP in 2012-13. The only problem the India economy and china are having is the Inflation devil. Indian economies have taken adequate steps to control the inflation. These include: selective ban on exports and futures trading in rice and some pulses, zero import duty on select food items and removal of restrictions on licensing, stock limits and movement of food articles under the Essential Commodities Act of 1955. Permission was given to import of pulses and sugar by public sector undertakings. Distribution of imported pulses and edible oils was permitted through the Public Distribution System (PDS) and a higher quota of non-levy sugar was released. Along with all these the RBI have taken adequate steps to control the inflation through repo and reverse repo rates. The economic trade balance and currency have also went through some turbulent times. A robust domestic demand coupled with a weak global demand has resulted in a widening of the trade deficit, which has spilled over into higher levels of current account deficit. The current levels of capital inflows, which exceed financing requirements of our current account deficit, have put pressure on the Rupee, resulting in its appreciation in the last few months. This has implications for India exports. But apart from all these the Indian economy and China are poised for further upside growth. Flow of funds will dry up some times and again it will flood but the thing which will never be erased will be the immense growth story and the resources yet to found from the Asian economies. Indian Bull is yet to begin its chase. Whatever has been happening till now can only be called as warm up phase. But the Asian Tiger has made lot of chase and needs some relaxation to begin another round of chase. The conclusion of the Bull and the Tigre is that they have more steams lefts month themselves to fire up and move a head, Investors should not panic to sell off or neither should develop the thought that they are investing at higher levels. We are in the new phase of changeover of mind where new highs will be our base line .What has happened in the previous phase does not necessarily means we will have to continue and settle with low. We are in the journey of asking more and stretching our outlook beyond the ordinary means. We should now understand that Indian stock market growth is linked with the internal growth of the streets of India. Its not dependent on borrowed capital of Developed economy. Indian growth resources have been identified by Developed and world economy. The Asian economy will see new sunshine which is yet to come in the coming decades. Just remember everything has a time to come and when it comes it comes in uncountable numbers

CAclubindia

CAclubindia