As all of you may know that the Anti-Profiteering Provisions are now applicable to all Registered persons as per which the intent is to pass on the benefit of reduction of price to the End consumer. As this is something new introduced with GST and about 2 months have passed since the launch of GST we all must expect that this progressive approach must be functioning smoothly. However, the reality is far from our expectations.

After interacting with many Trade experts as well as some Trade persons, what I got to know that the Government is very serious on whether the Industry is reducing their prices after GST or not in this respect what they are inquiring is

• If prices are reduced due to GST, publicize it and let the public know that your prices are reduced due to GST

• If prices are not being reduced, then what are the reasons for the same

• If prices have increased which is in a very few cases due to some local grants being killed, let the public know that the increase in prices is not due to GST

So one might assume that the Government is very focussed on Anti-Profiteering and the next two years, all concerned stakeholders should be vigilant on Anti-Profiteering provisions and their compliance.

However, no law is first made without having any shortcomings and Anti-Profiteering in my opinion while made on a good Intent falls short on the implementation part. In this article let's go through the shortcomings which needs to be addressed right away for bringing the good intent in perspective, but first let's quickly go through Section 171, the Rules made in respect to Ant-Profiteering in GST and what points are in favour of Anti-Profiteering before jumping to the Shortcomings part.

Section 171 of GST - Anti-profiteering measure

(1) Any reduction in rate of tax on any supply of goods or services or the benefit of input tax credit shall be passed on to the recipient by way of commensurate reduction in prices.

(2) The Central Government may, on recommendations of the Council, by notification, constitute an Authority, or empower an existing Authority constituted under any law for the time being in force, to examine whether input tax credits availed by any registered person or the reduction in the tax rate have actually resulted in a commensurate reduction in the price of the goods or services or both supplied by him.

(3) The Authority referred to in sub-section (2) shall exercise such powers and discharge such functions as may be prescribed.

Anti-profiteering Rules, 2017

Power to determine the methodology and procedure:

The Authority may determine the methodology and procedure for determination as to whether the reduction in rate of tax on the supply of goods or services or the benefit of input tax credit has been passed on by the registered person to the recipient by way of commensurate reduction in prices.

Duties of the Authority:

It shall be the duty of the Authority:

(1) to determine whether any reduction in rate of tax on any supply of goods or services or the benefit of the input tax credit has been passed on to the recipient by way of commensurate reduction in prices; (2) to identify the registered person who has not passed on the benefit of reduction in rate of tax on supply of goods or services or the benefit of input tax credit to the recipient by way of commensurate reduction in prices;

(3) to order,

i. reduction in prices;

ii. return to the recipient, an amount equivalent to the amount not passed on by way of commensurate reduction in prices along with interest at the rate of eighteen percent from the date of collection of higher amount till the date of return of such amount or recovery of the amount not returned in case the eligible person does not claim return of the amount or is not identifiable, and depositing the same in the Fund referred to in section 57

iii. imposition of penalty as prescribed under the Act; and

iv. cancellation of registration under the Act

Order of the Authority:

(1) The Authority shall, within a period of three months from the date of receipt of the report from the Director General of Safeguards determine whether a registered person has passed on the benefit of reduction in rate of tax on the supply of goods or services or the benefit of input tax credit to the recipient by way of commensurate reduction in prices.

(2) An opportunity of hearing shall be granted to the interested parties by the Authority where any request is received in writing from such interested parties.

(3) Where the Authority determines that a registered person has not passed on the benefit of reduction in rate of tax on the supply of goods or services or the benefit of input tax credit to the recipient by way of commensurate reduction in prices, the Authority may order -

i. reduction in prices;

ii. return to the recipient, an amount equivalent to the amount not passed on by way of commensurate reduction in prices along with interest at the rate of eighteen percent from the date of collection of higher amount till the date of return of such amount or recovery of the amount including interest not returned in case the eligible person does not claim return of the amount or is not identifiable, and depositing the same in the Fund referred to in section 57;

iii. imposition of penalty as prescribed under the Act; and

iv. cancellation of registration under the Act.

A. The Pros

a) Intention by Centre

As I previously mentioned, the intention of the Government is that the End Consumer enjoys the reduction in price of a product due to GST. As reported by TOI, Even Kerela's Finance Minister T M Thomas Isaac told the assembly on the 17th August meeting "The price of branded products are determined by the manufacturers alone. Many see GST as an opportunity to increase profit margins,"

b) State Governments pushing on Anti-Profiteering even if against Centre

Again Kerala's Finance Minister, T M Thomas Isaac in the same meeting held that Kerala would press the Union government to strictly implement the anti-profiteering clause to put an end to the unrealistic price rise in the post GST regime.

He said "Prices are supposed to come down with the advent of GST. But it's just the reverse that is happening. Majority of the state's representatives in GST council are still opposed to the strict implementation of the anti-profiteering clause, with immediate effect. The economic adviser to the Union government too was against the anti-profiteering, for which we pushed a lot. The price rise is up by 2.13% in the post GST regime. The attitude of the Centre in this regard is regressive."

Now let's discuss the Shortcomings part which you all are here for.

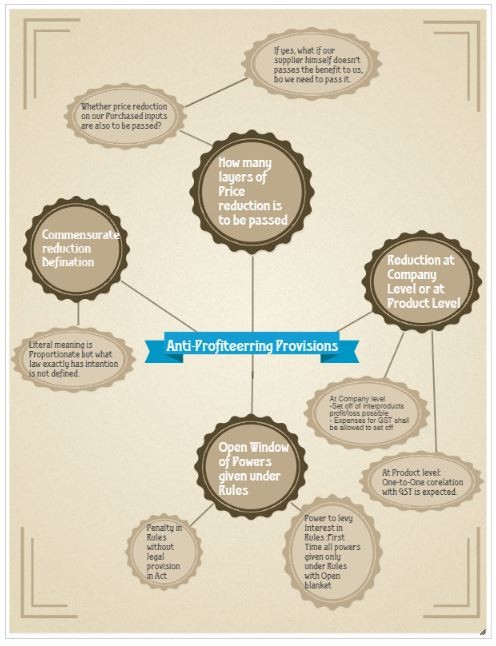

B. The Problem(s)

The anti-profiteering provision was for the first time inserted in the draft GST law in the November 2016 version. Since then the Trade and the Industry were in wait of clarity on the mechanism of how they need to follow the Anti-Profiteering sections in form of Rules, as in Rules generally if there is something to be implemented in the Act, its procedure and other details are mentioned in form of Rules and all their expectations went in vain when GST Council in its meeting on June 18, 2017, finally announced that the rules have been cleared.

So what happened after the Rules were in place, the matter would have been settled, Right?

Sadly, there is still no clarity on exactly know what one is required to do if one has to be GST compliant from price perspective. So let's discuss the Price perspective first.

a) Price Reduction not defined

i. Commensurate Reduction:

Commensurate literally means Proportionate however the term 'commensurate reduction in the price' is not defined or discussed in the Act or under the Rules. In the absence of a definition or guidance on 'commensurate reduction', the industry will follow its own economics to determine the commensurate reduction in price of goods or services. As this matter is subjective and will depend on Assessee to Assessee this will definitely result in rise of disputes and thus you will always be under the Wrath of the Tax Authorities.

Why I say that, It's because:

The Rules merely state that the authority may determine the methodology and procedure for determination - whether the reduction in rate of tax on supply of goods or services or the benefit of input tax credit has been passed on by way of commensurate reduction in prices or not. The establishment of an authority and the power to make its own procedures, is apparently a means to determine whether the commensurate reduction has actually happened or not and not what you need to follow.

ii. Enterprise/Company Level or Product Level

The question being asked here with Practical examples are:

a. How will businesses compute the benefit resulting from increased credits and reduction in rates? Will it be calculated at a company level or product level?

b. Will it be a net profit or gross profit?

c. Can I add additional expenses which I am required to incur due to GST while computing the cost and then arrive at the benefit?

Let's say there is a company called Hindustan Lever Ltd. Which has its roots in all products of FMCG and is also into Beverage and Health Drinks involving Aerated Water. Now post GST, Hindustan Lever Ltd. Will have a much lower burden on Toothpastes by 8-9% however on its Coconut flavoured low-fat Aerated Water Drink, the effective tax on this Drink has increased much higher than before. So now should the Company pass on the benefit on a Product to Product level and pass on the 8-9% of value of Toothpaste and bear the losses on the Healthy Drink business.

Or it should see at its Income statement as what most companies do and the increase in Profits if everything remains constant should be passed on to the Consumer. This way if we are talking on an Enterprise level the expenses on compliance of GST will also be expensed in the Income statement and thus the net benefit if any is passed onto the consumer.

While the second method will be more favourable to the Trade and Industry however in my opinion as the section mentions at goods/services thus Product Level approach is to be followed. Thus one-to-one correlation on Products before and after GST will be required and if there any benefit arises without including the extra Compliance cost due to GST is to be passed

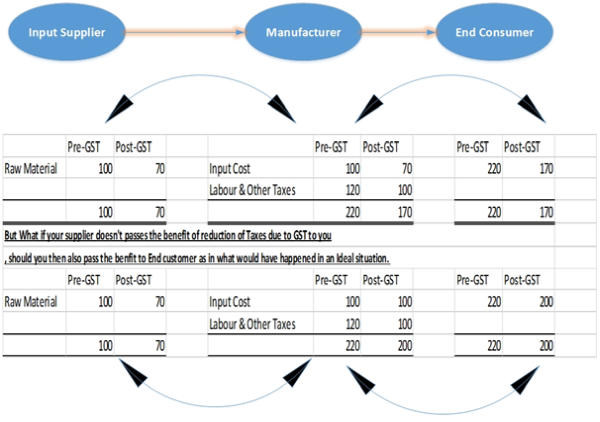

iii. How many layers of Price Reduction do we need to monitor and then to be passed?

Assume a case where I purchase my Input Raw material from a supplier who is a Registered supplier for Rs.100 p.u. Pre-GST Rate. I after Incurring Labour, Other Overheads and all taxes of Rs.120 p.u sells the goods at Rs.220 again Pre-GST Rate. After Implementation of GST, ideally due to lowering of effective taxes as many taxes subsumed under GST. My input should be at Rs 70 p.u. Post-GST rates and after Incurring Labour, Other Overheads and all taxes which has fallen to Rs.100 p.u. due to the same reason, I should be ideally selling the goods at Rs.170p.u. Post-GST Rate. However, My Input supplier does not pass on the benefit to me and my price actually comes out to Rs. 200 p.u. Post-GST Rate.

a. Should I also pass on the benefit which should accrue to me however was never realised on my Input Purchases?

b. If Yes, then how many layers of Input purchase should I monitor and ultimately pass on the Benefit?

These questions are there yet no procedure was prescribed as to what businesses should do.

(See Figure Below)

b) Open Window of Powers given under Rules

i. Penalty without provision of levy under Sections

If you go through Section 171 and the Rules which are to be read in its support, you will observe that the Authority shall exercise such powers and discharge its functions to see that whether input tax credits availed by any registered person or the reduction in the tax rate have actually resulted in a commensurate reduction in the price of the goods or services or both supplied by him. There is no mention on Penal provisions if the assessee fails to pass on the benefit.

One should understand that there is a simple difference on Ground Rules prescribing how to follow something and Rules on what if one fails to follow that thing. The Section gives powers on the 'How to follow' Question and not on 'What If' situation. So as if the Section doesn't prescribe the levy of Penalty the Rules which mentions that Order can be given on imposition of penalty as prescribed under the Act, the Rules Are Void-ab-initio.

ii. All powers given under rules itself

On all the laws I have studied till date, there is one thing common in them. Rules are made for better understanding for what is already mentioned in the section itself. If the section provides that a penalty will be levied as a penal provision on noncompliance of the relevant section then the amount of Penalty is prescribed under the Rules, as Rules are what can be changed easily by the Central Government vis-à-vis changing the Act & its sections as Parliament approval is needed then.

However, the Rules on Anti-Profiteering has everything stuffed into them, even some penal provisions which the Section (or the Act) never mentions of which Prima-facie shows a last minute patch-up work was done by the Government as GST was to be implemented by D-Day 01st July.

While these issues are not which cannot be rectified and what we need is an Amendment act which puts all these provisions into the Act where it should have been in the first place.

iii. The Process is not practical

A multi-step approach has been detailed starting with each state constituting a screening committee that will examine written complaints made about any entity or business earning undue profit. While a sunset clause of two years has been inserted, a period of 8-11 months has been provided for the whole process involving screening of the complaint and subsequent investigation and action, if any, by the anti-profiteering authority.

As there is a lot of confusion on the basics of Anti-Profiteering itself, expect to many litigations in near future. And if this probability might actually come true then by the time the Final resolution comes the Anti-Profiteering Provisions might not be in practise then.

Latest Update

'The GST Council, at its next meeting later this week, will finalise a mechanism to operationalise anti-profiteering clause which seeks to protect consumers interest', Honourable Finance Minister Arun Jaitley told the Lok Sabha on Tuesday, 1st August.

C. Conclusion

The Government should release some guidance regarding methodology, including calculations and periodicity, to reflect such commensurate reduction, before it's too late as almost 2 months have been passed since GST is implemented. The release of clear guidance will help the industry to comply with the anti-profiteering provisions.

Let's wait for decisions in the next Council meeting and see where it goes.

CAclubindia

CAclubindia