Type of Refund Available Under GST Law

|

S. No. |

Type of Refund |

Section |

Time Line for apply refund |

Time Line for Passing Refund Order |

|

1 |

General Refund of any tax, interest or any other amount paid by applicant. |

54(1) |

2 years from relevant date. |

60 days from the date of receipt of application. (Section 54(7)) |

|

1A |

Any balance in the electronic cash ledger |

54(1) Proviso |

Can be claimed in return furnished under section 39 and within 2 years from relevant date. |

Do |

|

2 |

Refund of tax paid on inward supplies of goods or services or both by (See Note-1). |

54(2) and 55 |

6 months from last day of quarter in which such supply was received. |

Do |

|

3 |

Refund of unutilised ITC on zero rated supplies made without payment of tax. |

54(3) |

Refund application may be filed at the end of any tax period and within 2 years from relevant date. |

Provisional refund within 7 days as per rule 91(2) and section 54(6) and balance within 60 days. |

|

4 |

Refund of unutilised ITC accumulated on account of rate of tax on inputs being higher than the rate of tax on output supplies (other than nil rated or fully exempt supplies) |

54(3) |

Refund application may be filed at the end of any tax period and within 2 years from relevant date. |

1. 60 days from the date of receipt of application. (Section 54(7)) 2. Question whether applicable in case of ITC available on CG. |

|

5 |

Refund to Casual Dealer/Non Resident taxable person |

54(13) & 27 |

As per 4th proviso of rule 89(1),refund shall be claimed in last return. |

60 days from the date of receipt of application. (Section 54(7)) |

|

6 |

Amount of CGST and SGST paid instead of IGST and Vice Versa |

54(1) & 77 |

2 years from relevant date |

Do |

|

7 |

Refund of Tax paid on non taxable supply. |

54(1) & 76(11) |

2 years from relevant Date |

Do |

|

8 |

Refund of integrated tax paid on supply of goods to tourist leaving India. |

15 of IGST Act |

Rules not yet provided. |

Rules not yet provided. |

|

9 |

Refund amount of IGST in case of Zero Rated Supply of goods or services on payment of IGST. |

16(3)(b) |

2 years from relevant date |

Do |

|

10 |

Refund of Interest paid under section 42(9) or 43(9) due to mismatch of ITC. |

42(9) or 43(9) |

2 years from relevant date |

Do. As per rule 77, it may be credited in electronic cash ledger also. |

Conditions

A.General conditions for claiming refund

As per section 54(4), the application shall be accompanied by

(a) documentary evidence to establish that a refund is due to the applicant; and

(b) such documentary or other evidence to establish that the amount of tax etc. was collected from, or paid by applicant and the incidence of it had not been passed on to any other person.

Provided that where the amount of refund is less than 2,00,000/- then declaration, based on the documentary or other evidences available with him shall be sufficient.

(c) Section 54(8) specified cases where refund amount shall be paid to applicant instead credited to Consumer Welfare Fund.

(d) No refund if amount less than 1,000 rupees.

As per 54(14), no refund shall be paid to an applicant, if the amount is less than rupees 1,000/-.

B. Conditions for claiming refund of unutilized ITC u/s 54(3)

(a) As per 1st proviso of 54(3), no refund of unutilised ITC shall be allowed in cases where the goods exported out of India are subjected to export duty.

(b) As per 2nd proviso of 54(3), no refund shall be allowed, if the supplier of goods or services or both avails of drawback in respect of central tax or claims refund of the integrated tax paid on such supplies.

(c) As per section 54(6), in the case of any claim for refund on account of zero-rated supply of goods or services or both made by registered persons, the proper officer may refund on a provisional basis, 90% of the total amount so claimed, excluding the amount of input tax credit provisionally accepted.

(d) Proper officer may withhold refund

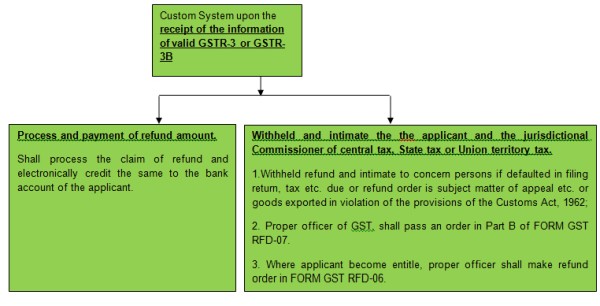

(i) if defaulted in furnishing any return or required to pay any tax, interest or penalty or deduct from the refund due, any tax, interest, penalty, fee or any other amount which the taxable person is liable to pay. (Section 54(10).

(ii) Where an order giving rise to a refund is the subject matter of an appeal etc. (Section 54(11)).

(e) No refund in case of notified supplies of goods or services or both as per section 54(3).

C.Conditions to claim refund by Casual Dealer/Non Resident taxable person

As per section 54(13), amount of advance tax deposited by a casual taxable person or a non-resident taxable person under section 27(2), shall be refunded only if all the returns required under section 39, furnished in respect of the entire period for which the RC granted to him.

Note-1:

A. A specialized agency of the United Nations Organization or

B. Any Multilateral Financial Institution and Organization notified under the United Nations (Privileges and Immunities) Act, 1947

C. Consulate or Embassy of foreign countries or

D. Any other person or class of persons, as notified under section 55

Note-2: Relevant date meaning is given in Explanation 2 of Section 54.

Note-3: Section 142 deals with cases of transitional phase refund.

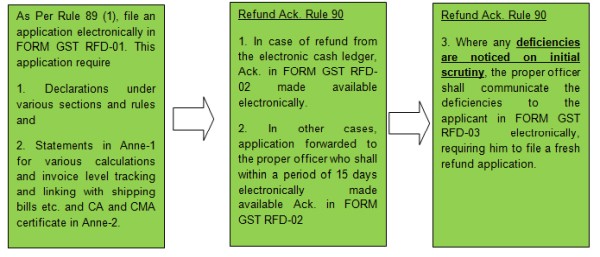

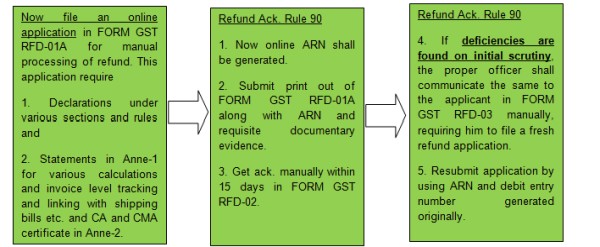

Process and Forms For Claiming Refund:

As per normal provisions, refund application shall be filed and processed online through Form GST RFD-01 to Form GST RFD-10. However, as it could not be implemented till date, vide NN 55-CGST dated 15/11/2017, CGST Circular No. 17/17/2017 – GST dated 15.11.17 & CGST Circular No. 24/24/2017 – GST dated 21.12.18, manual filing and processing of refund allowed through Form GST RFD-01A.

Chart-1 Online Filing and Processing of Refund Under GST

Chart-2 Manual Filing and Processing of Refund Under GST

Note: 1

In case of balance in the electronic cash ledger, refund may be claimed through the return furnished for the relevant tax period in FORM GSTR-3 or FORM GSTR-4 or FORM GSTR-7.

Note: 2

Refund to Casual Dealer/Non Resident Taxable Person

As per 4th proviso of Rule 89(4), refund of any amount, after adjusting the tax payable by the applicant out of the advance tax deposited by him under section 27 at the time of registration, shall be claimed in the last return required to be furnished by him.

Note: 3

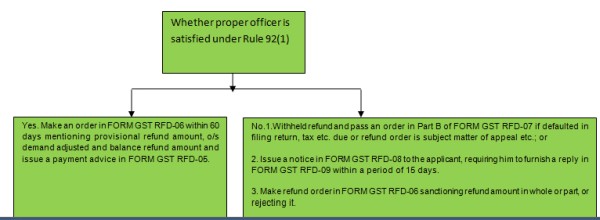

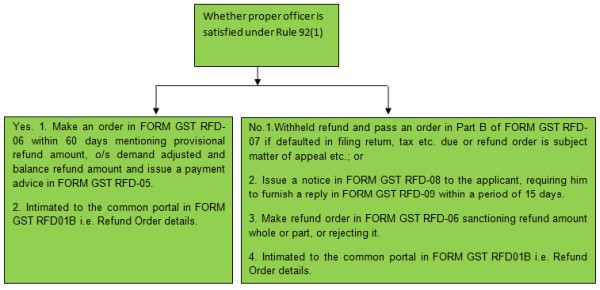

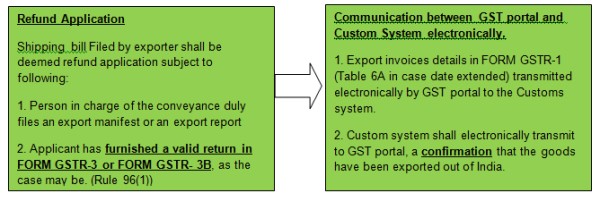

As per rule 91(2), the proper officer, on being prima facie satisfied, shall make an order in FORM GST RFD-04, sanctioning the amount of refund due to the said applicant on a provisional basis within a period not exceeding 7 days from the date of the acknowledgement in case of refund of unutilized ITC in case of zero rated supply.

As per rule 91(1), provisional refund shall not be granted if claimant prosecuted for any offence under the Act or under an existing law where the amount of tax evaded exceeds two hundred and fifty lakh rupees during any period of five years immediately preceding the tax period.

Note: 4

Where the amount of refund is completely adjusted against any outstanding demand under the Act or under any existing law, an order giving details of the adjustment shall be issued in Part A of FORM GST RFD-07.

Note: 5

As per Rule 95, in case of refund of tax paid on inward supplies of goods or services or both by a specialised agency of the United Nations Organisation etc., refund shall be applied in RFD-10 once in every quarter along with a statement of the inward supplies of goods or services or both in FORM GSTR-11.

Note: 6

Refund of unutilized ITC on zero rated supplies made without payment of tax. Refund amount shall be calculated as per formula given in Rule 89(4). (Rule 89)

In addition to chart given above, we need to ensure following documents and evidences with refund application:

|

Refund of unutilized ITC on Zero Rated Supply -Goods |

Refund of unutilized ITC on Zero Rated Supply- Services |

||

|

To SEZ Units or Developers |

Exported out of India |

To SEZ Units or Developers |

Exported out of India |

|

As per 2nd proviso to Rule 89(1), application shall be filed by supplier after goods have been admitted in full in the SEZ for authorized operations, as endorsed by the specified officer of the Zone; |

- |

As per 2nd proviso to Rule 89(1), application shall be filed by supplier along with such evidence regarding receipt of services for authorized operations as endorsed by the specified officer of the Zone: |

- |

|

a statement containing the number and date of invoices + evidence regarding the endorsement specified above. Rule 89(2)(d) |

a statement containing the number and date of shipping bills or bills of export +the number and the date of the relevant export invoices. Rule 89(2)(b) |

a statement containing the number and date of invoices + the evidence regarding the endorsement specified + the details of payment proof made by the recipient. Rule 89(2)(e). |

a statement containing the number and date of invoices + the relevant BRC* or FIRC** Rule 89(2)(c). |

|

a declaration to the effect that the SEZ unit or developer has not availed the ITC of the tax paid by the supplier of goods or services or both. Rule 89(2)(f) |

a declaration to the effect that the SEZ unit or developer has not availed the input tax credit of the tax paid by the supplier of goods or services or both. Rule 89(2)(f) |

||

*BRC = Bank Realization Certificates ** FIRC = Foreign Inward Remittance Certificates

Note: 7 Refund in case of deemed export.

As per 3rd proviso of rule 89(1), in respect of supplies regarded as deemed exports, the application may be filed by

(a) the recipient of deemed export supplies; or

(b) the supplier of deemed export supplies where the recipient does not avail of ITC on such supplies and furnishes an undertaking to the effect that the supplier may claim the refund.

As per Rule 89(2)(g) refund application shall be accompanied by a statement containing the number and date of invoices along with such other evidence as may be notified in this behalf.

Further NN48-CGST dated 18.10.2017, notified following category of supply as deemed export:

|

S. No. |

Description of supply |

|

1 |

Supply of goods by a registered person against Advance Authorization |

|

2 |

Supply of capital goods by a registered person against Export Promotion Capital Goods Authorization |

|

3 |

Supply of goods by a registered person to Export Oriented Unit |

|

4 |

Supply of gold by a bank or Public Sector Undertaking specified in the notification No. 50/2017-Customs, dated the 30th June, 2017 (as amended) against Advance Authorization. |

Above notification is applicable wef 18.10.2017 means upto 17.10.17 these supplies was considered as normal supply and GST was applicable as normal supply.

Note 8 Currently refund can be applied in following cases only:

Select the Refund type:

Indicates Mandatory Fields

|

Refund of Excess Balance in Electronic Cash Ledger |

CREATE |

|

|

Refund of ITC on Export of Goods & Services without Payment of Integrated Tax |

CREATE |

|

|

On account of supplies made to SEZ unit/ SEZ developer (without payment of tax) |

CREATE |

|

|

Refund on account of ITC accumulated due to Inverted Tax Structure |

CREATE |

|

|

Recipient of Deemed Exports |

CREATE |

|

|

On Account of Assessment/Provisional Assessment/Appeal/Any other order |

CREATE |

|

|

Refund on account of Supplies to SEZ unit/ SEZ Developer (with payment of tax) |

CREATE |

|

|

Export of services with payment of tax |

CREATE |

Chart-3 Online process of refund of IGST paid on Export of Goods Rule 9

Note-1

As per rule 96(8), The Central Government may pay refund of the integrated tax to the Government of Bhutan on the exports to Bhutan for such class of goods as may be notified in this behalf.

Note-2

The persons claiming refund of integrated tax paid on exports of goods or services should not have received supplies on which the supplier has availed the benefit

|

S. No. |

NN |

Nature of transactions |

|

1 |

48/2017-Central Tax dated the 18th October, 2017 |

Deemed Export |

|

2 |

40/2017-Central Tax (Rate) dated the 23rd October, 2017 |

Merchant Exporter |

|

3 |

41/2017-Integrated Tax (Rate) dated the 23rd October, 2017 |

Merchant Exporter |

|

4 |

78/2017-Customs dated the 13th October, 2017 |

Allows import by SEZ in custom without payment of IGST. |

|

5 |

79/2017-Customs dated the 13th October, 2017 |

Allows import by Deemed Exporter in custom without payment of IGST. |

Note-3

Vide circular no. 42/2017-Customs dated 7/11/2017, customs department, analysis the common errors that are hindering the disbursal of IGST refund and decisions taken to address such errors.

Note-4 Refund of amount of IGST paid on Zero rated Supply of goods or services. Rule 96

|

Refund of IGST Paid on Zero Rated Supply of Goods |

Refund of IGST Paid on Zero Rated Supply of Services |

||

|

Export out of India |

Supplied to SEZ Units or Developers |

Export out of India |

Supplied to SEZ Units or Developers |

|

See Chart-3 above. |

See Chart-1 &2 and See Note 6 above. |

See Chart-1 & 2 and See Note 6 above. |

See Chart-1 & 2 and See Note 6 above. |

Refund Meaning:

As per Explanation of Section 54. - For the purposes of this section,-

(1)"refund" includes

- refund of tax paid on zero-rated supplies of goods or services or

-

both or on inputs or input services used in making such zero-rated supplies, or

-

refund of tax on the supply of goods regarded as deemed exports, or

-

refund of unutilized ITC as provided under sub-section (3).

I hope above blog is useful for you. Your valuable feedback in respect of same would be highly appreciated.

The author can also be reached at Capuneetgoyal.delhi@gmail.com

Disclaimer: The above write up has been compiled from various provisions of CGST Act 2017, IGST Act 2017 and rules and notifications issued there under. The compilation may not be entirely correct for reader to reader due to different interpretations by different readers. The readers are advised to take into the consideration the prevailing legal position before acting on any of the comments in this write up. Readers are also requested to convey the correct position as per their interpretation of the provisions of CGST Act 2017, IGST Act 2017 and rules and notifications issued there under which shall be most welcome for correcting this write up.

CAclubindia

CAclubindia