Source, Complexities, Analysis & What Next? (CA Final Audit May 17 Paper)

Hello everyone as a professor its very important to understand what material is being used for drafting papers, understand the trend so that I can make students hit bulls eye. So we worked for many hours to give you accurate and path breaking analysis. Last time it was out of box paper you can read analysis on this link - Out of the box Audit Paper CA Final Nov 16. Ok this time in May 17, ICAI drafted comparatively much easier paper. Few questions were tricky and some were again from remote corners of module.

Source of Drafting Paper

You will be surprised to see many of below facts. (Paper was of 120 marks) (Don't add up below marks there is overlapping of the source)

1. After last times analysis, I saw a trend that many questions were asked from module and PM which were in bold & italics, has diagram, chart or highlighted as case study. We even identified all such areas and uploaded important file online. So we suggested all students who came in touch that target such areas.

Bingo guys this time 25 Marks paper was from such areas. May be ICAI wanted target changes or it was natural human behaviour to pick such questions. So those who followed this strategy got rich dividends with very low time investment.

2. ICAI has a problem it has 2 materials for same topic with little bit of difference, in this exam 3 questions were asked on sampling, now sampling is covered in SA 530 also and special audit technique also. I personally feel content in SA is better more logical, better expressed and easy to retain. SO if students follow SA 530 content it will be fine. These 3 questions accounted for 14 Marks on only one point related to sampling. All these points were one below another in special audit chapter 5.2.1 / 5.2.5 / 5.2.6

3. Last 5 years RTPs contributed to 75 Marks of paper. May 17 RTP contributed around 20 marks, that is superb number. And surprisingly Nov 15 RTP contributed highest 20 marks. (Last time no questions were asked from recent RTP)

4. Last 10 years papers contributed to 60 Marks of paper.

5. PM contributed to 59 Marks paper, last time it was 37. So this time there was drastic increase. This also indicates PM doesn't cover all RTP questions.

6. There were questions of 29 Marks exclusively (Not Covered in PM / RTP) from module.

7. We have linked our notes to all PM questions, through PM analysis file so that you can covers PM along with notes efficiently and effectively. Students those who followed our notes and covered PM could target 111 marks.

I will suggest follow your class notes as base, very important for understanding and retention + PM for practicing questions. You should keep Module & Collection of past 5 year RTPs to see if any particular topic is left out, just see headings and topic questions are targeting.

Click here to view the file explaining source of each question.

Complexities / Accident Points / Traps

Q1(a) - Rotation Applicable to Company / OLD Audit firm finished their maximum tenure / New Audit Firm Appointed and then twist, one of the partner from OLD Audit firm joins new audit firm 3 months after appointment.

Now similar question but not the same was there in May 16 RTP Q7(a), but in this question, it was clearly specified that partner retires from OLD Audit firm and he is signing partner.

So our exams question was different. If we assume that partner who joins NEW Audit Firm has retired from old firm and he was signing partner then we can say that as per Rule 6 (3)(ii) Explanation II of Sec 139(2) such new firm will also be ineligible / disqualified for such 5 years.

But one more possibility is there if don't assume he retired from old firm then it will become case of common partner, As per 2nd proviso to sec 139 (2) we have to see situation of common partner at the date of appointment, in this case common partner situation arises 3 months after appointment so this position is absolutely fine, so new firm will not be disqualified.

So 2 answers are possible for above company audit question. Because certain things are missing and it is explicitly said that joining is after 3 months I prefer 2nd as more appropriate answer.

Q2(c)- Question looks simple straight forward, we all know that sample should be representative of population. But problem is what to explain in this question, out of loads knowledge we have. Now as per module students are suppose to explain types of sampling methods here, some students would have missed it.

Q3(b)- Initial it looks as PE question, as ditto question exists in PM in PE chapter. Only difference is they ask treatment as per income tax act, so this was the twist. We have to answer it as per income tax act and also professional ethics both. This was highlighted in module, we marked it as imp point in imp list.

Answer is as per Rule 12A of Income Tax if CA knowingly supplies false information then he can be punished up to 7 years. Further as per Sch 2, Part 1, Clause 6 it should be professional misconduct.

Q5(c)- Interesting one, company has separate statutory auditor and separate tax auditor, statutory auditor has not submitted their audit report, so what will tax auditor do, in such scenario tax auditor as no audit is conducted as per company act, he will have to perform audit of financial statement and give his report in Form 3CB, it was a new one, students those who gave a proper thought would have cracked it.

Q6(a)- is Quick Response Code allowed on visiting card of practicing CA. It is a black berry like code, once you scan information in visiting card gets saved automatically in mobile phone. As per ICAI clarification such quick response code is allowed provided only that information should get saved which is allowed on visiting card. Module has included this explanation below Sch 1 Part 1 Clause 7. Students could have explained clause 6 as well.

Further some students thought that he is promoting his website, this is not correct, writing name of website on visiting card is allowed, writing please visit website is not allowed. Which was not the case here. (Bold / Highlighted in module)

Q6(b)- Misconduct under Sch 2 Part 1 Clause 3

Q6(c)- Misconduct under Sch 1 Part 3 Clause 2

Q6(d)- Misconduct under Sch 1 Part 1 Clause 11 (Bold / Highlighted in module)

Q7(a)- Right on Lien on books of accounts is concept from UK, provided certain conditions are satisfied, there is no such reference in Indian law, in fact as per Sec 128 as explained in module such thing is not practical. Further as per Saxena Vs Sharma case supreme court prohibits professionals from doing this.

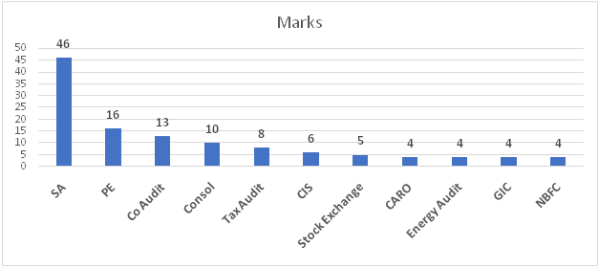

Marks Allocation

*If we assume that sampling related questions are from Special Audit Technique Chapter then 14 marks from SA will be reduced and a new bar with special audit may appear.

Scoring

I expect students will score comparatively higher marks as compared to Nov 16 as many questions were from PM / RTP, so they had a over view. As a professor I will tell exact answers, but you will get 50-60% marks even if content is not bang on target but relevant.

What Next?

1. As May 17 was on easier side, Nov 17 can be challenging. Take audit seriously, allocate sufficient time 100-120 hours for classes and then 50-60 hours for self study and 25-30 for 1st revision.

2. Study from notes and then go to PM, use our PM analysis file. PM is must but PM should not be the starting point.

3. We will be uploading question bank on past 5 years RTP soon, use it.

4. Conceptual understanding + shortcuts, charts etc are must to excel in subject.

5. Do daily writing practice religiously, without exception.

Be in touch we will be uploading many important files for Nov 17 soon.

To view the question paper on Advanced Auditing (CA Final) : Click Here

To enrol Advanced Auditing (CA Final) subject of the author : Click Here

CAclubindia

CAclubindia