Paper Analysis / Suggested Answers / Common Mistakes - CA IPC May 16

Highlights

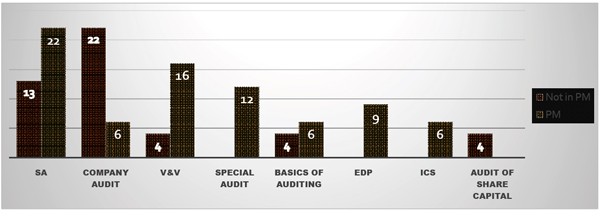

• Around 50 marks paper was not from PM, they were new questions

• 35 Marks from SA, 28 Marks from Company Audit, 20 Marks from Vouching & Verification, 12 Marks from Special Audit

1. Discuss the following:

Q. (a) W.r.t SA-550,"Identification of significant related party transaction outside the entity's normal course of business."

Identified Significant Related PartyTransactions outside the Entity’s Normal Course of Business

For identified significant related party transactions outside the entity’s normal course of business, the auditor shall: (Sale to subsidiaries in Mauritius and Dubai then export to various countries for tax saving)

(a) Inspect the underlying contracts or agreements, if any, and evaluate whether:

(i) The business rationale (or lack thereof) of the transactions suggests that they may have been entered into to engage in fraudulent financial reporting or to conceal misappropriation of assets;

(ii) The terms of the transactions are consistent with management’s explanations; and (But goods are not exported but sold to local manufacturer)

(iii) The transactions have been appropriately accounted for and disclosed in accordance with the applicable financial reporting framework; and (Sales were recorded when goods move out of factory gates, but it should be when they are delivered)

(b) Obtain audit evidence that the transactions have been appropriately authorised and approved. (Many BOD members were not aware about such arrangement and no BOD resolution to support it

Q. (b) W.r.t SA-530, meaning of audit sampling and requirements relating to sample design, sample size and selectin of items for testing.

Audit Sampling: As per SA 530 on “Audit Sampling”, the meaning of the term “Audit Sampling” is the application of audit procedures to less than 100% of items within a population of audit relevance such that all sampling units have a chance of selection in order to provide the auditor with a reasonable basis on which to draw conclusions about the entire population.

According to the said SA, requirements relating to sample design, sample size and selection of items for testing are explained below

Sample Design - When designing an audit sample, the auditor shall consider the purpose of the audit procedure and the characteristics of the population from which the sample will be drawn.

Sample Size -The auditor shall determine a sample size sufficient to reduce sampling risk to an acceptably low level.

Selection of Items for Testing - The auditor shall select items for the sample in such a way that each sampling unit in the population has a chance of selection.

Q. (c) How does an audit programme help to plan and perform the audit?

(a) The Role of Audit Programme in Audit Plan and Performance: The audit programme is helpful both in planning and performance stages of audit-

(b) (i)The audit programme lists down areas of audit before commencement.

(ii)The audit timing is built therein; thereby it becomes a schedule of audit plan.

(iii)The staff who are entrusted with the audit assignment is also specified. It is a plan of resource allocation of the firm.

(iv) It specifies the procedures to be checked during the audit.

(v) As the audit work is split into various elements of procedures to be performed, the audit programme acts as a guiding chart or check list during the performance of audit.

(vi) Since the staff in charge of each work is specified and they sign the programme, it extracts the responsibility from the audit assistants.

(vii) The working papers of the audit staff can be reviewed against the audit programme which helps a base of reference for evaluation of the performance before reporting on the financial statements.

(viii) It also helps in preparing a diary of the performance and plan and also base for billing the clients for the time and manpower involved in the audit.

To read the full article / view the answers in PDF Form : Click here

To view the question paper : Click here

To enrol online class on Auditing & Assurance of the author : Click here

CAclubindia

CAclubindia