Paper Analysis / Suggested Answers / Common Mistakes - CA Final May 2016 Exams

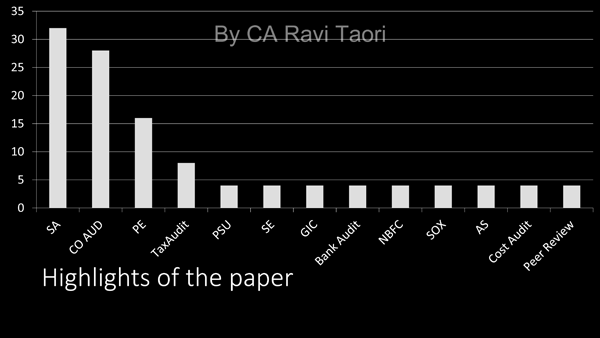

Generally audit paper from past 4 attempts was of 7 pages but this time it increase to 11 pages (57% increase)

Questions of around 50 marks were from PM rest of 70 marks questions were new from module / SAs

| Level of Questions | Marks |

| Easy | 61 |

| Medium | 22 |

| Difficult | 37 |

| Grand Total | 120 |

Highlights of the paper

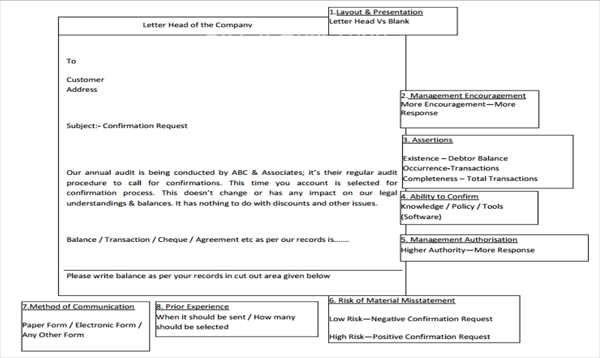

Factors to consider when designing confirmation requests include: (From SA 505)

a. The assertions being addressed.

b. Specific identified risks of material misstatement, including fraud risks.

c. The layout and presentation of the confirmation request.

d. Prior experience on the audit or similar engagements.

e. The method of communication (for example, in paper form, or by electronic or other medium).

f. Management's authorisation or encouragement to the confirming parties to respond to the auditor. Confirming parties may only be willing to respond to a confirmation request containing management's authorisation.

g. The ability of the intended confirming party to confirm or provide the requested information (for example, individual invoice amount versus total balance).

Video Representation of the Analysis of the Audit Paper

When a Response to a Positive Confirmation Request is Necessary to Obtain Sufficient Appropriate Audit Evidence

In certain circumstances, the auditor may identify an assessed risk of material misstatement at the assertion level for which a response to a positive confirmation request is necessary to obtain sufficient appropriate audit evidence. Such circumstances may include where:

i. The information available to corroborate management's assertion(s) is only available outside the entity.

ii. Specific fraud risk factors, such as the risk of management override of controls, or the risk of collusion which can involve employee(s) and/or management, prevent the auditor from relying on evidence from the entity.

To read the full article / view the suggested answers in PDF form: Click here

To view the question paper on Advanced Auditing : Click here

To enrol online class on Advanced Auditing of the author: Click here

CAclubindia

CAclubindia