An amount of Rs. 1,293/- was deducted by ICICIBank during the Financial Year 2023-24 as Income Tax at Source (TDS) from the interest payable to me on my investment in Senior Citizen Savings Scheme. The bank issued Form 16A to me for this deduction. This figure of Rs.1,293/- was shown in my form 26AS as well as in AIS as the TDSby theBank u/s 194A on 20-Mar-2024.The deduction was actually made on 1-Jan-2024 since the interest,after applying TDS,was paid to me on that date. The e-filing portal of the IT Deptt. was also showing this TDSon dashboard in my login.

However, I made a mistake in writing the TAN of thebank in Schedule TDS2of my IT Return. The correct TAN was MUMI10473B (ICICI Bank) but I mistakenly mentioned it as MUMH03189E (HDFC Bank). The IT Deptt. did not give me credit for this amount. They simply ignored it and did not give me the refund of this amount which was due.

I, therefore, filed a rectification request (grievance). In that grievance, I correctly quoted the TAN of ICICI Bank. I wrotethe following in my rectification request:

“Total tax paid by me (TDS+Advance tax) was Rs. 26,588/- but in my assessment order only Rs. 25,295/- has been shown. Thus, there is a shortfall of Rs. 1,293/- in my tax credit. This figure of Rs. 1,293/- has been shown in my form 26AS as the TDS by ICICI Bank (MUMI10473B) u/s 194A. Date of booking is 20-Mar-2024. This TDS has been ignoredby the deptt. Your own portal is showing on the dashboard that I have paid Rs. 26,588/-. Kindly rectify the error and issue a refund of Rs. 1,293/- ”.

However, I specifically could not mention that I have made a mistake in writing TAN in my IT Return since I had not noticed it by then.

Even with this rectification request in which I correctly mentioned the TAN of the deductor bank, the IT Deptt. did not give me any credit for this amount and gave no refund. The rectification order said –“ Form 26AS does not contain amount of TDS with respect to the TAN mentioned in schedule TDS 2. There is no payment due. ”

They just did not read the rectification request at all. They simply sent a copy of their original Assessment Order calling it Rectification Order.

In the next financial year, i.e. in 2024-25, I again made the same mistake. Actually, I have very little changes in my ITR data from year to year. I, therefore, do not fill the whole return again every year in order to save my effort. I, instead, pick-up the previous year’s JSON file, open it using a text editor, change the assessment year, and save it (JSON files which are created by the IT Return software of the IT Deptt. are human readable text files unlike binary files which can be read only by computer). I,then, open this modified JSON file with the current year’s offline JSON utility of the IT Deptt., make necessary changes, save it, and upload it on the e-filing portal. This is the reason that the mistake committed by me in 2023-24 was carried forward to 2024-25 also. However, this time my mistake caused me a bigger loss as described below.

During the financial year 2024-25, I had the followingtaxes deducted at source from my interest payments:

1. By ICICI Bank (TAN MUMI10473B) - Amount Rs. 16,432/-

2. By HDFC Bank (TAN MUMH03189E) - Amount Rs. 47,495/-

Total TDS = Rs. 63,927/-

As usual, both the banks issued me Form 16A for these deductions. My form 26AS and AIS were showing these figures as TDSby my Banks u/s 193 and 194A. The e-filing portal of the IT Deptt. was also showing these amounts on thedashboard in my login.

As I have written above, I made mistakes inquoting the TAN’s of the deductor banks and filled theschedule TDS2 as given belowwhile filing my return:

1. TAN - MUMH03189E (instead of MUMI10473B) -Amount Rs. 16,432/-

2. TAN - MUMI04813E (instead of MUMH03189E) -Amount Rs. 47,495/-

MUMI04813E is another TAN of ICICI Bank.

Due to this mistake, I was given credit of only Rs.16,432/- and the second amount was disallowed. My income duringthe Financial Year 2024-25 was non-taxable and, therefore, the whole TDS was due for refund. But IT Deptt. issued me a refund of only Rs. 16,432/- instead of Rs.63,927/-.

Now, compare the TDS in IT Deptt.’s records v/s my reporting in Schedule TDS 2.

|

Sl. No. |

Deductor’sTAN |

As per 26AS / AIS |

Reported in Schedule TDS 2 |

Credit Allowed by IT Deptt. |

|

|

|

(Rs.) |

(Rs.) |

(Rs.) |

|

1. |

MUMI10473B (ICICI Bank) |

16,432/- |

Nil |

Nil |

|

2. |

MUMH03189E (HDFC Bank) |

47,495/- |

16,432/- |

16,432/- |

|

3. |

MUMI04813E (Another TAN of ICICI Bank) |

Nil |

47,495/- |

Nil |

Now the question arises – When their own record shows that ICICI Bank (MUMI10473B) has deducted Rs. 16,432/- and deposited the amount in their account, why they are taking it as Nil? Because I have mistakenly specified it as Nil?

Similarly, when their record shows that HDFC Bank (MUMH03189E) has deducted Rs. 47,495/- and deposited the money with them, why they are allowing only Rs. 16,432/-? Because I have specified it as Rs. 16,432/- by mistake?

They have so much faith on me? They believe me more than themselves?

However, their faith on me completely evaporates as we proceed to the last (3 rd )row. Now they just don’t believe me at all and accept their own records.

Why these double standards?

All this is not even necessary. When the income is non-taxable, the full TDS shown in their records can/should be refunded. Simple. No complicated math required. No need to even compare what is in IT Deptt.’s records and what is reported by the taxpayer.

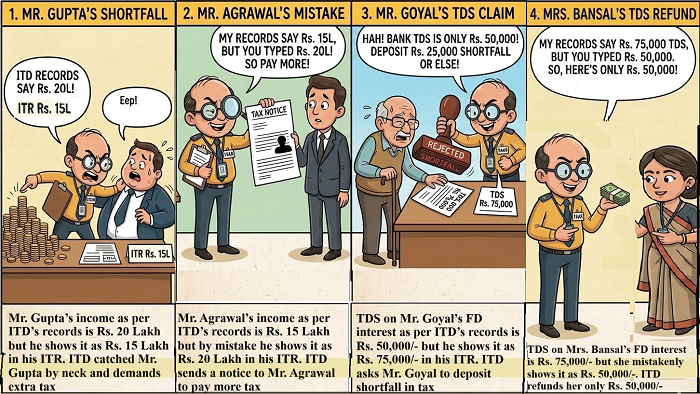

Now consider a case in which the taxable income of a taxpayer in their records differs with what he reported in his ITR. Let us assume that their record shows the income as Rs. 20 Lakh whereas the income reported in ITR is Rs. 15 Lakh. They will not lose even a single second and send a notice to the taxpayer with additional demand.

Not only this, if the actual income of a taxpayer in their records is Rs. 15 Lakh but by mistake he reports it as Rs. 20 Lakh, they will immediately send notice demanding extra tax.

But in case of taxes paid (TDS + Advance Tax) v/s taxes reported, their behavior will be exactly the opposite. Why?

This forces me to demand that Schedule TDS 2 should be scrapped from the Income Tax Return. If this schedule was not there in the ITR, I would not have filled in the wrong data and this catastrophe would not have happened to me. Even otherwise, what is the use of asking for the data which is already available to you?

True, various government and other departments often maintain important data coming from two different sources in their systems. They purposely have some redundancy in data. But their intention is different. They have a good intent. They do this to ensure data accuracy. They cross-check the data received from the two sources with each other and make certain that it matches. If any discrepancy is observed, they proceed to a stricter scrutiny. They examine whether someone made a mistake providing the data or forgot to supply any material information.

But, the IT Deptt. has already made a blind rule: if there is any mismatch between the TDS data available with them and that supplied by the taxpayer, then lower of the two values will be admitted without investigating why the mismatch occurred. Under this condition, abolishing schedules TDS 1, TDS 2, TDS 3, TCS, Advance Tax and Self-assessment Tax will control the damage.

However, such double standards are not beneficial for anybody.

Nor the trait of issuing rectification orders without paying any attention as to why the rectification is being requested!

CAclubindia

CAclubindia