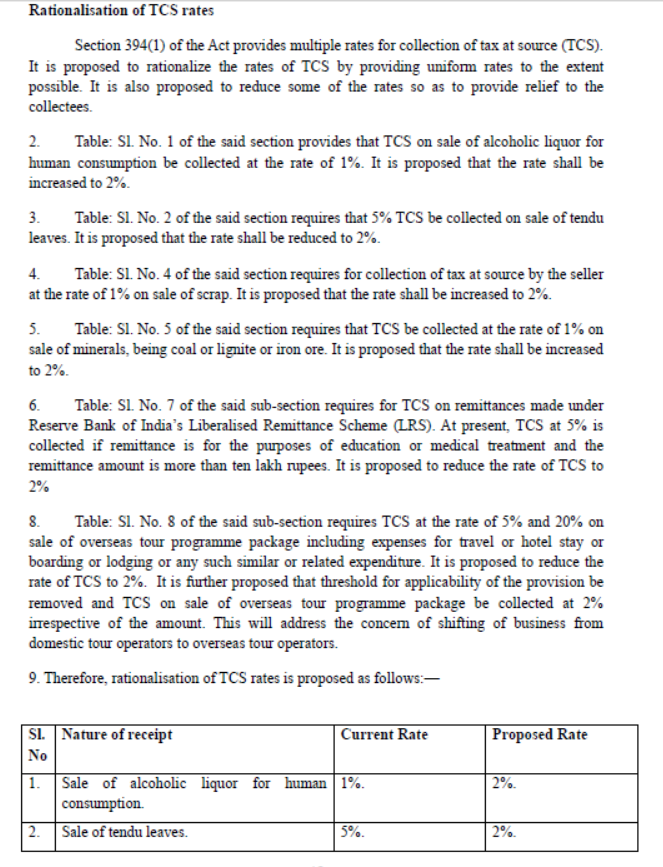

The Finance Bill, 2026 has proposed a comprehensive Rationalisation of Tax Collected at Source (TCS) rates under Section 394(1) of the Income-tax Act, 2025. The proposal aims to bring greater uniformity in TCS rates, reduce compliance complexity, and provide targeted relief to taxpayers, while also enhancing collections in certain high-value or sensitive sectors.

The amendments are scheduled to take effect from 1 April 2026.

Objective Behind TCS Rationalisation

At present, Section 394(1) prescribes multiple TCS rates for different categories of transactions , leading to operational complexity for sellers and confusion for collectees. The proposed changes seek to:

- Introduce uniform TCS rates wherever feasible

- Reduce rates in select cases to provide relief

- Increase rates in specific sectors to align with revenue considerations

- Address structural issues such as business shifting to overseas operators

Key Changes in TCS Rates: Category-Wise Analysis

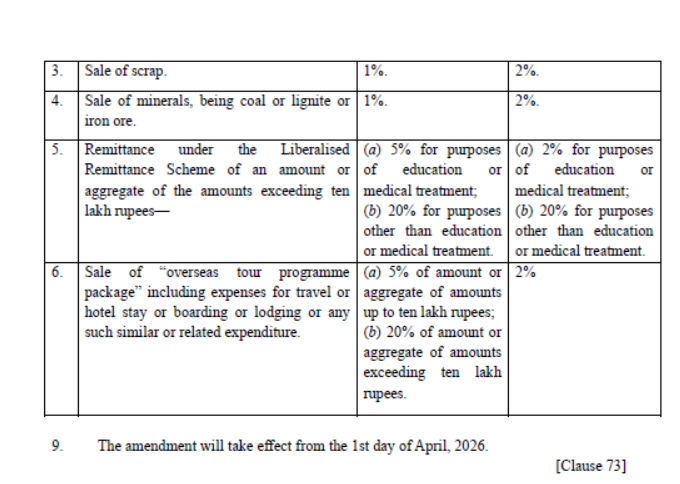

1. Sale of Alcoholic Liquor for Human Consumption

- Current Rate: 1%

- Proposed Rate: 2%

The TCS rate on sale of alcoholic liquor is proposed to be doubled, indicating a calibrated increase in tax collection from this sector.

2. Sale of Tendu Leaves

- Current Rate: 5%

- Proposed Rate: 2%

This reduction brings significant relief to traders and businesses dealing in tendu leaves, aligning the rate with the broader rationalisation objective.

3. Sale of Scrap

- Current Rate: 1%

- Proposed Rate: 2%

The increased rate is expected to improve tax tracking and compliance in a sector traditionally prone to revenue leakage.

4. Sale of Minerals (Coal, Lignite and Iron Ore)

- Current Rate: 1%

- Proposed Rate: 2%

The hike reflects the government's intent to strengthen tax collection in core mineral sectors.

5. Remittances under Liberalised Remittance Scheme (LRS)

For remittances exceeding Rs 10 lakh in a financial year:

Education and Medical Treatment

- Current Rate: 5%

- Proposed Rate: 2%

Other Purposes

- Current Rate: 20%

- Proposed Rate: 20% (No change)

The reduced TCS rate for education and medical remittances provides welcome relief to individuals making genuine overseas payments for essential purposes.

6. Overseas Tour Programme Package

Current Rates:

- 5% up to Rs 10 lakh

- 20% beyond Rs 10 lakh

Proposed Rate: Uniform 2% (No threshold)

A major reform, this change removes the threshold limit and applies a flat 2% TCS irrespective of the amount. The government has specifically noted that this measure aims to prevent the shifting of business from domestic tour operators to overseas operators .

Summary of Proposed TCS Rate Changes

| Nature of Transaction | Current Rate | Proposed Rate |

|---|---|---|

| Sale of alcoholic liquor | 1% | 2% |

| Sale of tendu leaves | 5% | 2% |

| Sale of scrap | 1% | 2% |

| Sale of coal, lignite, iron ore | 1% | 2% |

| LRS - education/medical (above Rs 10 lakh) | 5% | 2% |

| LRS - other purposes | 20% | 20% |

| Overseas tour programme package | 5% / 20% | 2% |

Effective Date

All the above amendments will come into force from 1 April 2026 , subject to enactment of the Finance Bill, 2026.

Conclusion

The proposed rationalisation of TCS rates reflects a balanced approach, simplifying the rate structure, providing relief to individuals and specific sectors, and strengthening compliance in high-value transactions . Businesses, tour operators, and individuals undertaking foreign remittances should proactively assess the impact of these changes and update their systems well before the effective date.

Official copy of the Clause is as follows

CAclubindia

CAclubindia