First Bi-monthly Monetary Policy Statement, 2016-17

|

By Dr. Raghuram G. Rajan, Part A: Monetary Policy Monetary and Liquidity Measures On the basis of an assessment of the current and evolving macroeconomic situation, it has been decided to:

Consequently, the reverse repo rate under the LAF stands adjusted to 6.0 per cent, and the marginal standing facility (MSF) rate to 7.0 per cent. The Bank Rate which is aligned to the MSF rate also stands adjusted to 7.0 per cent. Assessment 2. Since the sixth bi-monthly statement of February 2016, global economic activity has been quiescent. Perceptions of downside risks to recovery in some advanced economies (AEs) at the beginning of 2016 have eased, while major emerging market economies (EMEs) continue to contend with weak growth and still elevated inflation amidst tighter financial conditions. World trade remains subdued due to falling import demand from EMEs and stress in mining and extractive industries. In the US, consumer spending was underpinned by a strengthening labour market, but flagging exports proved to be a drag on growth in Q4 and cloud the near-term outlook. In the Euro area, tailwinds in the form of aggressive monetary policy accommodation and still low energy prices have supported activity in an environment beset with uncertainties from the migrant crisis, intensifying stress in the banking sector, and possible Brexit. While Japan escaped recession in Q4 of 2015, a combination of weak consumer spending, business investment and exports has slowed the economy in Q1 of 2016. In China, sluggish industrial production, contracting exports, capital outflows and substantial excess capacity in factories and the property market remain formidable headwinds, notwithstanding significant monetary and fiscal policy stimulus. EME commodity exporters have benefited recently from the firming up of commodity prices and risk-on investor sentiment has appreciated their currencies. Across EMEs, however, weak domestic fundamentals, lacklustre external demand and country-specific constraints continue to restrain growth. 3. Global financial markets have recouped the losses suffered in the turbulence at the beginning of the year. From mid-February, a firming up of crude prices buoyed market sentiment, allaying fears of global recessionary risks. With China reducing reserve requirements, the ECB expanding accommodation and the Fed providing dovish guidance while staying on hold, equity markets rallied. In bond markets across AEs and EMEs, yields gradually eased, with country-specific variations. The US dollar has retreated from January peak and has eased further in the aftermath of the FOMC’s March meeting. On the other hand, the euro and the yen have appreciated, reacting perversely to exceptional accommodation. Currencies across EMEs have also appreciated as portfolio flows returned cautiously to local debt and equity markets. Gold prices have jumped 16 per cent in Q1 of 2016 on safe haven demand. Commodity prices, including oil, have picked up recently, though they still remain soft. However, the uneasy calm that prevails in financial markets could be dispelled easily by a sudden return of risk-off investor sentiment on incoming data, especially pertaining to China or to US inflation. 4. On the domestic front, gross value added (GVA) in agriculture and allied activities moderated in H2 of 2015-16, pulled down by the contraction in Q3 due to the year-on-year decline in kharif production. Turning to Q4, second advance estimates of the Ministry of Agriculture indicate that despite acutely low reservoir levels and a deficient north-east monsoon, rabi foodgrains production increased over its level a year ago – mainly in wheat and pulses – and compensated partly for the shortfall in kharif output. Unseasonal rains and hail in March are likely to have damaged some winter crops, particularly wheat, although full estimates of the crop loss await advance estimates. On the other hand, fertiliser production has picked up, and horticulture as well as allied activities have remained resilient, suggesting that the implicit estimate of GVA for agricultural and allied activities in Q4 in the CSO’s advance estimates is likely to be achieved, if not revised upwards. 5. Value added in industry accelerated in H2, led by manufacturing which benefited from the sustained softness in input costs. By contrast, industrial production remained flat with manufacturing output shrinking since November. Robust expansion in coal output has buoyed both mining activity and electricity generation and stemmed the weakening of industrial output. However, capital goods production fell into deep contraction since November, even after excluding lumpy and volatile items like rubber insulated cable. Weak demand and competition from imports have muted the capex cycle. Consumer non-durables production has been shrinking, with a pronounced decline in Q4. This reflects the continuing slack in rural demand. On the other hand, consumer durables remained strong, even after abstracting from favourable base effects, which suggests that urban demand is holding up. With improved perceptions on overall economic conditions and income, the Reserve Bank’s Consumer Confidence Survey of March 2016 shows marginal improvement in consumer sentiments. The March manufacturing purchasing managers’ index (PMI) continued in expansionary mode on the back of new orders, including exports. The Reserve Bank’s industrial outlook survey suggests that business expectations for Q1 of 2016-17 continue to be positive. 6. Services sector activity expanded steadily through the year, with trade, hotels, transport, communication and public administration, defence and related services turning out to be the main drivers in H2. The construction sector continues to be overburdened by unsold inventory in the residential space, although commercial real estate is being boosted by demand from information technology (IT) and IT-enabled services. Road construction has accelerated, including in terms of new awards. Cement production appears to have gained traction during H2, while steel consumption has increased at a steady pace. Various lead and coincident indicators such as air passenger traffic, air cargo volumes, foreign tourist arrivals and auto sales increased, while railway freight traffic marginally contracted. The services PMI remained in expansion mode during H2 on new business and expectations. The outlook for services in surveys is upbeat for Q1 of 2016-17. 7. Retail inflation measured by the consumer price index (CPI) dropped sharply in February after rising for six consecutive months. This favourable development was due to a larger than anticipated decline in vegetable prices, helped by prices of pulses starting to come off the surge that began in August, and effective supply management that helped limit cereal price increases. Accordingly, food inflation eased for the first time in the second half of 2015-16. Notably, this occurred on a decline in prices rather than favourable base effects, which were at work in the first half of the year. Inflation in the fuel group moderated across electricity, kerosene, cooking gas and firewood, the latter easing pressures on rural inflation. Three months ahead household inflation expectations declined to a single digit for the second consecutive round of the survey in response to these dynamics. 8. CPI inflation excluding food and fuel edged up in February, mainly under housing, education, personal care and transport and communication, suggesting capacity constraints in the services sector. Excluding petrol and diesel from this category, inflation stayed elevated and persistent at or above 5 per cent, indicating a possible resistance level for further downward movements in the headline. The stubborn underlying inflation momentum is unlikely to be helped by the 7th Pay Commission award and the effects of the one-rank-one-pension (OROP) award, or by the cost-push effect of the increase in the service tax rate. However, rural wage growth as well as the rate of increase in corporate staff costs was moderate. Also, input and output prices polled in purchasing managers’ surveys rose modestly for manufacturing and services. 9. Liquidity conditions, which had tightened since mid-December, were stretched further by the larger-than-usual accumulation of cash balances by the Government, unusually heightened and persistent demand for currency, a pick-up in bank credit and flatter deposit mobilisation at this time relative to past years. The Reserve Bank undertook liquidity operations to quell these pressures and supplemented normal operations with large amounts of liquidity injected through fine-tuning variable rate repo auctions in tenors ranging between overnight and 56 days. The average daily liquidity injection (including variable rate overnight and term repos) increased from ₹ 1,345 billion in January to ₹ 1,935 billion in March. Besides, durable liquidity was also provided through open market operations (OMOs) of the order of ₹ 514 billion and ₹ 375 billion through buy-back operations in February and March. The Reserve Bank also started conducting reverse repo and MSF operations on holidays in Mumbai to enable the frictionless functioning of the payment and settlement system. 10. Effective April 2, 2016 the statutory liquidity ratio (SLR) of scheduled commercial banks was reduced by 25 basis points from 21.5 per cent to 21.25 per cent of their NDTL. Also, from February 2016, banks were allowed to reckon additional government securities held by them up to 3 per cent of their NDTL within the mandatory SLR requirement as level 1 high quality liquid assets (HQLA) for the purpose of computing their liquidity coverage ratio (LCR), thereby taking the total carve-out from SLR available to banks equivalent to 10 per cent of their NDTL. These measures will create space for banks to increase their lending to productive sectors on competitive terms so as to support investment and growth. 11. FCNR(B) deposits and associated swaps undertaken in September 2013 are expected to mature starting September this year. It is important to note that these swaps are fully covered by the Reserve Bank’s forward purchases. Moreover, the Reserve Bank will monitor developments closely to contain any unanticipated market volatility associated with the repayment. 12. While exports declined in February in US dollar terms for the fifteenth successive month, the rate of contraction narrowed to a single digit for the first time in this period and volume growth turned positive. The decline in non-POL exports was even smaller, with gems and jewellery, drugs and pharmaceuticals, electronics and chemicals driving the upturn. The prolonged contraction in imports also slowed significantly, and non-POL non-gold import growth turned positive for the first time after seven months. This reflected a sizable upsurge in imports of machinery, supported by a pick-up in imports of pearls and precious stones and electronic goods. With gold imports falling in February and March, the continuing softness in crude prices working favourably in terms of conserving the POL import bill and some gains in terms of trade, the trade deficit narrowed to its lowest monthly level since September 2013. In turn, this has likely lowered the current account deficit (CAD) in Q4 below 1.3 per cent of GDP recorded in Q3, despite a moderation in net receipts from services exports and remittances. Net inflows in the form of foreign direct investment (FDI) were robust in Q4 (up to January), more than sufficient to fund the external financing requirement. Foreign portfolio investors (FPIs), who were net sellers in the domestic capital market up to February, became net buyers in March in both equity and debt segments. Policy Stance and Rationale 13. Inflation has evolved along the projected trajectory and the target set for January 2016 was met with a marginal undershoot. Going forward, CPI inflation is expected to decelerate modestly and remain around 5 per cent during 2016-17 with small inter-quarter variations (Chart 1). There are uncertainties surrounding this inflation path emanating from recent unseasonal rains, the likely spatial and temporal distribution of monsoon, the low reservoir levels by historical averages, and the strength of the recent upturn in commodity prices, especially oil. The persistence of inflation in certain services warrants watching, while the implementation of the 7th Central Pay Commission awards will impart an upside to the baseline through direct and indirect effects. On the other hand, there will be some offsetting downside pressures stemming from tepid demand in the global economy, Government’s effective supply side measures keeping a check on food prices, and the Central Government’s commendable commitment to fiscal consolidation.

14. The uneven recovery in growth in 2015-16 is likely to strengthen gradually into 2016-17, assuming a normal monsoon, the likely boost to consumption demand from the implementation of the 7th Pay Commission recommendations and OROP, and continuing monetary policy accommodation. After two consecutive years of deficient monsoon, a normal monsoon would work as a favourable supply shock, strengthening rural demand and augmenting the supply of farm products that also influence inflation. On the other hand, the fading impact of lower input costs on value addition in manufacturing, persisting corporate sector stress and risk aversion in the banking system, and the weaker global growth and trade outlook could impart a downside to growth outcomes going forward. The GVA growth projection for 2016-17 is accordingly retained at 7.6 per cent, with risks evenly balanced around it (Chart 2).

15. In its bi-monthly monetary policy statement of February 2, 2016, the Reserve Bank indicated that it awaits further data on inflation as well as on structural reforms in the Union Budget that boost growth while controlling spending. Given recent data, forecasts in Chart 1 indicate that inflation will trend towards the 5 per cent target in March 2017 under reasonable assumptions. The changes to the RBI Act to create a Monetary Policy Committee will further strengthen monetary policy credibility. In the Union Budget for 2016-17, the Government has adhered to the path of fiscal consolidation and this will support the disinflation process going forward. The Government has also set out a comprehensive strategy for reinvigorating demand in the rural economy, enhancing the economy’s social and physical infrastructure, and improving the environment for doing business and deepening institutional reform. The implementation of these measures should improve supply conditions and allow efficiency and productivity gains to accrue. Given weak private investment in the face of low capacity utilisation, a reduction in the policy rate by 25 bps will help strengthen activity and aid the Government’s initiatives. 16. Perhaps more important at this juncture is to ensure that current and past policy rate cuts transmit to lending rates. The reduction in small savings rates announced in March 2016, the substantial refinements in the liquidity management framework announced in this policy review and the introduction of the marginal cost of funds based lending rate (MCLR) should improve transmission and magnify the effects of the current policy rate cut. The stance of monetary policy will remain accommodative. The Reserve Bank will continue to watch macroeconomic and financial developments in the months ahead with a view to responding with further policy action as space opens up. Part B: Developmental and Regulatory Policies 17. This part of the Statement reviews the progress on various developmental and regulatory policy measures announced by the Reserve Bank in recent policy statements and also sets out new measures to be taken for further refining the liquidity management framework; strengthening the banking structure; broadening and deepening financial markets and extending the reach of financial services to all. I. Liquidity Framework for Monetary Policy Operations 18. The Reserve Bank’s liquidity framework was changed significantly in September 2014 in order to implement key recommendations of the Expert Committee to Revise and Strengthen the Monetary Policy Framework (Chairman: Dr. Urjit R Patel). With over six quarters of implementation history, it is appropriate to review the experience, with a view to making necessary adjustments as well as to more fully implement the report of the Expert Committee. 19. Liquidity management is driven by two objectives: first, the need to supply or withdraw short term liquidity from the market so as to accommodate seasonal and frictional liquidity needs such as the build-up of Government balances and demand for cash; and second, the need to supply durable liquidity in the economy so as to facilitate growth, while ensuring that the monetary policy stance is supported. 20. The Reserve Bank has kept the system in an ex ante deficit mode on average, with a liquidity shortfall equivalent to one per cent of banks’ NDTL. The rationale has been that the banking system would borrow from the Reserve Bank’s liquidity facilities, ensuring that the repo rate guided short term money market rates and thereby was effective as the policy rate. 21. The first objective of meeting short term liquidity needs has been accomplished through the provision of liquidity by the Reserve Bank under its regular facilities - variable rate 14-day/7-day repo auctions equivalent to 0.75 per cent of banking system NDTL, supplemented by daily overnight fixed rate repos (at the repo rate) equivalent to 0.25 per cent of bank-wise NDTL. Frictional and seasonal mismatches that move the system away from normal liquidity provision are addressed through fine-tuning operations, including variable rate repo/reverse repo auctions of varying tenors. The weighted average call money rate has tracked the policy rate more closely than in the past, suggesting that short term liquidity needs have been adequately met. 22. The Reserve Bank aims to meet the second objective by modulating net foreign assets (NFA) and net domestic assets (NDA) growth over the course of the year, broadly consistent with the demand for liquid assets to meet transaction needs of the economy. This will ensure adequate availability of durable liquidity, regardless of short term seasonal and frictional fluctuations. The Reserve Bank tries to smooth this growth over the year. So, for example, in periods when the Reserve Bank purchases significant quantities of NFA, the growth of NDA may have to be commensurately lower and may even have to be negative through the open market sale of domestic bonds. 23. Experience suggests that the provision of short term liquidity does not substitute fully for needed durable liquidity, though durable liquidity can substitute for short term liquidity needs. Going forward, the Reserve Bank intends to first meet requirements of durable liquidity, and then use its fine-tuning operations to make short term liquidity conditions consistent with the intended policy stance. This may result in seemingly anomalous situations in which the Reserve Bank injects durable liquidity even when it is using short term instruments to withdraw excess short term liquidity, but such actions will be consistent with our dual objectives of liquidity management. 24. Finally, given that new instruments such as variable rate reverse repo auctions allow the Reserve Bank to suck out excess short term liquidity from the system without the excess liquidity being deposited with the Reserve Bank through overnight fixed rate reverse repo, it is possible for the Reserve Bank to keep the system closer to balance on average without the operational rate falling significantly. Thus, the past rationale for keeping the system in significant average liquidity deficit no longer is as compelling, especially when the policy stance is intended to be accommodative. Moreover, given that the Reserve Bank’s market operations rather than depositing or borrowing at standing facilities determine the operational interest rate, the policy rate corridor can be narrowed, as suggested by the Expert Committee. 25. Therefore, it has been decided to:

Detailed guidelines are being issued separately. The Reserve Bank will monitor the consequences of these changes as it modernises the country’s liquidity framework. II. Banking Structure 26. Large Exposures: Taking into account the views and suggestions received from stakeholders on the discussion paper on ‘Large Exposures Framework and Enhancing Credit Supply through Market Mechanism’, a fresh discussion paper will be issued by April 30, 2016 on large borrowers meeting a part of their funding requirements from markets. A draft circular on the Large Exposures Framework will be issued for public comments in June 2016 (to be implemented by January 1, 2019). 27. Revision of regulatory framework: The Basel Committee on Banking Supervision (BCBS) has issued final standards on the standardised approach for measuring counterparty credit risk (SA-CCR), a revised framework for the capital treatment of bank exposures to central counterparties (CCPs) and final rules on revised Pillar 3 disclosure requirements. These standards will be implemented by January 1, 2017 by BCBS member jurisdictions. The Reserve Bank proposes to issue draft guidelines on these standards by May 31, 2016. The Reserve Bank will also undertake revision of the guidelines on the securitisation framework in the light of the BCBS revisions to the securitisation framework which is to be implemented by January 2018. It is proposed to issue draft guidelines on the revised securitisation framework by June 2016. 28. Rationalisation of Branch Authorisation Policy: Currently, banks provide services through a variety of business outlets – branches; extension counters; satellite offices; mobile branches; ultra small branches and the like. The current policy approach is to facilitate adequate outreach of banking outlets in unbanked areas while at the same time providing autonomy to banks to decide their business strategy. Given that regulations are written in terms of branches, with a view to facilitating financial inclusion and providing flexibility on the choice of delivery channel, it is proposed to redefine branches and permissible methods of outreach keeping in mind the various attributes of the banks and the types of services that are sought to be provided. 29. Differentiated Licensing of Banks: In addition to recently licensed differentiated banks such as payments banks and small finance banks, the Reserve Bank will explore the possibilities of licensing other differentiated banks such as custodian banks and banks concentrating on whole-sale and long-term financing. A paper in this regard will be put out for comments by September 2016. 30. Margin Requirements for Over the Counter (OTC) Derivatives: In March 2015, the BCBS and the International Organisation of Securities Commissions (IOSCO) finalised a framework on margin requirements for non-centrally cleared derivatives. A consultative paper outlining the Reserve Bank’s approach to implementation of these requirements will be issued by end-April 2016 with a target of finalising the framework by end-July 2016. 31. Countercyclical Capital Buffers (CCCB): A review and empirical testing of CCCB indicators was carried out by the Reserve Bank to assess whether activation of the CCCB is warranted and it has been decided that it is not necessary to activate CCCB at this point in time. 32. Supervisory Enforcement Framework: Changes in the domestic and international financial sector environment necessitate formalisation of an improved supervisory framework for taking enforcement action against scheduled commercial banks for non-compliance of instructions and guidelines issued by the Reserve Bank. The framework, which is intended to meet the principles of natural justice and global standards of transparency, predictability, standardisation, consistency, severity and timeliness of action, will be formalised by June 2016. 33. Cyber Risks - Supervisory Assessment of Preparedness of Banks: The Reserve Bank has commenced detailed examination of IT used by banks on a pilot basis during the current year. IT examination reports are being issued separately so as to strengthen the information security preparedness of banks as well as to assess the effectiveness of IT adoption by banks. Moving forward, it is planned to cover major banks in 2016-17 and all banks from 2017-18. The Reserve Bank has constituted an Expert Panel (Chairperson: Smt. Meena Hemachandra) on IT Examination and Cyber Security to provide broad guidance on its approach. 34. Technology Support to Urban Cooperative Banks (UCBs): As a part of the Memorandum of Understanding with the State Governments/Central Government on UCBs, the Reserve Bank had agreed to provide technology support to UCBs with the objective of financial inclusion and ensuring implementation of standardised core banking solutions (CBS). It has been decided to prescribe standards and benchmarks for CBS in UCBs and provide financial assistance and technical support through the Institute for Development and Research in Banking Technology (IDRBT). The initial set-up cost in this regard will be borne by the Reserve Bank while the recurring cost will be borne by the UCBs. A circular in this regard is being issued separately. III. Financial Markets 35. Introduction of Money Market Futures: The Working Group on Enhancing Liquidity in the Government Securities and Interest Rate Derivatives (Chairman: Shri R. Gandhi) had recommended introduction of interest rate futures based on the overnight call money borrowing rate. It is important to develop such market segments which could signal expectations of market participants, while allowing hedging of asset-liability mismatches. It has been decided to allow futures on an appropriate money market rate. The contract specifications will be decided in consultation with market participants and the Securities and Exchange Board of India (SEBI) by end-September 2016. 36. Easier Market Access to Gilt Account Holders: With a view to easing the process of investment by gilt account holders, it will be made incumbent on custodians to provide all gilt account holders access to the NDS-OM web facility to enable them to trade directly on the platform. A similar facility is also proposed to be extended to foreign portfolio investors (FPIs). Detailed guidelines in this regard will be issued by end-June 2016. 37. Broadening Market Participation - Electronic Trading Platforms: In order to broaden participation in OTC derivatives and to provide a safe trading environment, it is proposed to put in place a policy framework for authorisation of electronic platforms with linkage to an approved central counterparty for settlement. The framework will also cover forex platforms to facilitate hedging by small and retail customers. The draft framework will be placed on the website for wider feedback by end-September 2016. Furthermore, in order to make participation in OTC derivative markets through electronic platforms more broad-based, it is proposed to review the existing guidelines on OTC derivatives. Guidelines will be issued by end-May 2016. 38. Tripartite Repo in Government Securities Market: The Working Group on Enhancing Liquidity in the Government Securities and Interest Rate Derivatives (Chairman: Shri R. Gandhi) had recommended introduction of tripartite repo to develop a term repo market. In this context, it has been decided to undertake a comprehensive review of collateralised money market segments, including introduction of tripartite repo, in consultation with market participants. The review will be placed on the Reserve Bank’s website by September 2016 for wider feedback. 39. Review of Guidelines for Commercial Paper (CP): With a spurt in the issuance of CPs, market participants and the Fixed Income Money Market and Derivatives Association (FIMMDA) have expressed the need for greater transparency and better dissemination of information. Accordingly, it is proposed to undertake a comprehensive review of guidelines with the objective of, inter alia, strengthening disclosure requirements by issuers of CPs, reviewing the role of issuing and paying agents (IPAs) and putting in place an information dissemination mechanism. Draft guidelines in this regard will be issued by end-July 2016 for wider feedback. 40. Guidelines for Accounting of Repo/Reverse Repo Transactions with the Reserve Bank: It is proposed to align the accounting norms to be followed by market participants for repo/reverse repo transactions under the liquidity adjustment facility (LAF) and the marginal standing facility (MSF) with the accounting guidelines prescribed for market repo transactions. Guidelines in this regard will be issued by end-May 2016. 41. Easing of Restrictions on Plain Vanilla Forex Options: Currently, plain vanilla currency options require adherence to stringent suitability and appropriateness norms although they are considered a generic product, while forward contracts are exempt from the same. It is proposed to bring plain vanilla forex options bought by bank clients at par with forex forwards on regulatory requirements. Detailed guidelines will be issued by end-September 2016. 42. Forex Benchmark-RBI Reference Rate: The Reserve Bank calculates and notifies the reference rate of the rupee (INR) against the US dollar and also publishes INR rates against the euro, the pound sterling and the yen every day around 1:30 P.M. These rates are based on quotes polled from a select list of contributing banks. As recommended by the Committee on Financial Benchmarks (Chairman: Shri P. Vijaya Bhaskar), it has been decided to move over to a process of determining the reference rate based on actual market transactions on volume weighted basis with effect from May 2, 2016. 43. Allowing Non-Resident Indians (NRIs) to Participate in the Exchange Traded Currency Derivatives (ETCD) Market: It has been decided to permit NRIs to participate in the ETCDs, subject to limits and other conditions that are stipulated by the exchanges recognised by the SEBI. Guidelines in this regard will be issued by the Reserve Bank in consultation with the SEBI by end-June 2016. 44. Initiatives for Start-ups: In the Sixth Bi-Monthly Monetary Policy Statement for 2015-16 and the press release dated February 2, 2016 the Reserve Bank had highlighted the steps being taken with respect to the Government’s initiatives to promote ease of doing business for start-ups. Guidelines/clarifications have already been issued in areas such as online submission of Form A2 for outward remittances up to certain thresholds, issue of shares without cash payments and acceptance of payments by the Indian start-ups on behalf of their overseas subsidiaries. In addition, guidelines in respect of deferred payment through escrow/ indemnity arrangement for transfer of shares, enabling investment by foreign venture capital investors (FVCIs) in start-ups and overseas investment operations for start-ups will be issued soon in consultation with the Government. Furthermore, the simplification of process for dealing with delayed reporting of FDI transactions and provisions for an enabling external commercial borrowing regime for start-ups are being examined by the Government and the Reserve Bank. IV. Non-banking Financial Sector, Financial Inclusion and Payment and Settlement 45. Simplification of Process of Registration of New Non-banking Financial Companies (NBFCs): In order to make the process of registration of new NBFCs smoother and hassle free, it has been decided to simplify and rationalise the process of registering new NBFCs. The new application forms will be simpler and the number of documents required to be submitted will be reduced to a minimum. 46. Peer to Peer Lending (P2P): P2P lending has shown accelerated growth over the last one year. While encouraging innovations, the Reserve Bank cannot be oblivious to the risks posed by such institutions to the system. A Concept Note on P2P lending will be put up on the Reserve Bank’s website for public comments by April 30, 2016 and based on the feedback, the contours of regulating P2P lending will be decided in consultation with the SEBI. 47. Strengthening Business Correspondent (BC) Infrastructure: The BC model offers significant scope for further strengthening. Accordingly, the following initiatives are proposed:

48. Micro, Small and Medium Enterprises (MSMEs): The Reserve Bank will lay down a framework by September 2016 for accreditation of credit counsellors who can act as facilitators for entrepreneurs to access the formal financial system with greater ease and flexibility. Credit counsellors will also assist MSMEs in preparing project reports in a professional manner which would, in turn, help banks make more informed credit decisions. 49. Payment and Settlement Systems in India – Vision 2018: The Reserve Bank will publish Vision 2018 for the payment and settlement systems in the country by end-April 2016. Vision 2018 will continue to focus on migrating to a “less-cash” and more digital society. The endeavour would be to make regulations more responsive to technological developments and innovations in the payments space. This would be complemented by enhanced supervision of payment system operators, improvement in customer grievance redressal mechanisms and for the strengthening of the payments infrastructure. 50. The second bi-monthly monetary policy statement will be announced on June 7, 2016; the third bi-monthly monetary policy statement on August 9, 2016; the fourth bi-monthly monetary policy statement on October 4, 2016; the fifth bi-monthly monetary policy statement on December 6, 2016; and the sixth bi-monthly monetary policy statement on February 7, 2017. Sangeeta Das |

CAclubindia

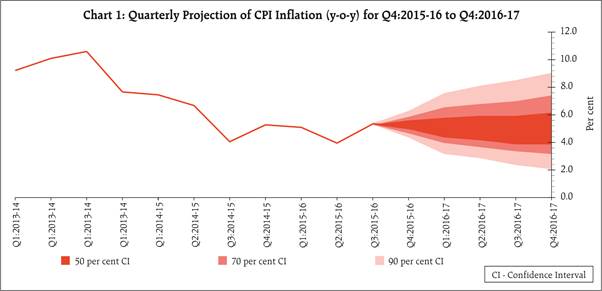

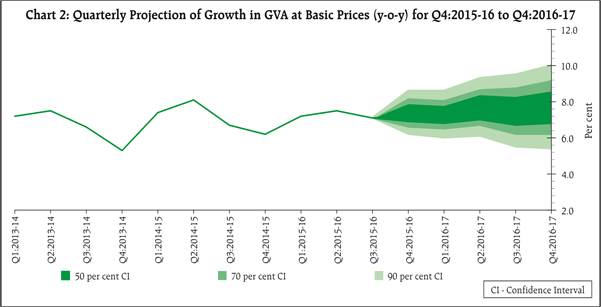

CAclubindia