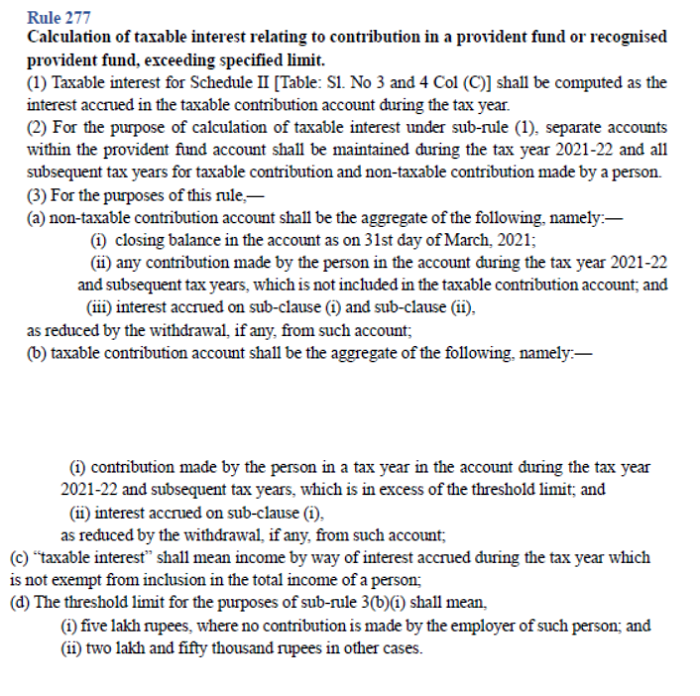

The Draft Income Tax Rules, 2026 have introduced Rule 277, providing a detailed framework for calculating taxable interest on contributions made to a provident fund or recognised provident fund when such contributions exceed the prescribed threshold limits. The rule aims to bring clarity and uniformity to the taxation of high provident fund contributions.

How Taxable Interest Will Be Calculated

As per Rule 277(1), taxable interest will be computed as the interest accrued during the tax year on the taxable contribution account. This means only the portion of contributions exceeding the specified limit will generate taxable interest, while interest on eligible contributions will continue to remain exempt.

Separate Accounts Mandatory

Rule 277(2) mandates maintaining separate accounts within the provident fund starting from tax year 2021-22 onwards:

- Taxable contribution account

- Non-taxable contribution account

This segregation ensures accurate tracking of contributions and interest for taxation purposes.

What Constitutes a Non-Taxable Contribution Account

Under Rule 277(3)(a), the non-taxable contribution account will include:

- Closing balance as on 31 March 2021

- Contributions made from FY 2021-22 onwards that are within the threshold limit

- Interest accrued on these amounts

Any withdrawals from this account will be reduced while computing the balance.

What Constitutes a Taxable Contribution Account

Rule 277(3)(b) specifies that the taxable contribution account will include:

- Contributions exceeding the threshold limit in a tax year

- Interest accrued on such excess contributions

Withdrawals, if any, will also be reduced from this account balance.

Meaning of Taxable Interest

The rule defines taxable interest as interest income accrued during the tax year that is not eligible for exemption and must be included in the total income of the taxpayer.

Threshold Limits Explained

Rule 277 sets two different thresholds depending on employer contribution:

- Rs 5 lakh where no employer contribution is made

- Rs 2.5 lakh in cases where employer contribution exists

Contributions above these limits will result in taxable interest.

Impact on High-Income Employees and Voluntary Contributors

Tax professionals believe the rule primarily affects high-income individuals and employees making large voluntary contributions to their provident funds. The requirement to maintain separate accounts ensures transparency and simplifies compliance for both taxpayers and tax authorities.

Why Rule 277 Matters

By formalizing the method of calculation, Rule 277 reduces ambiguity around taxation of provident fund interest and aligns administrative practices with the government’s intent to tax high contributions while preserving benefits for regular savers.

CAclubindia

CAclubindia