Dear all,

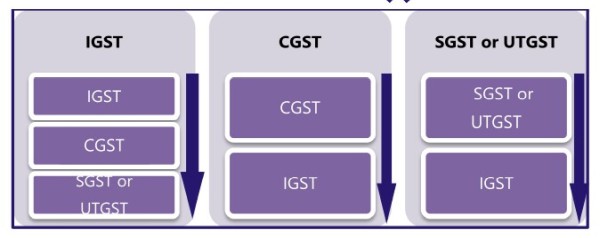

My input IGST =80000

Output IGST =12000

OUTPUT CGST = 45000

OUTPUT SGST =45000

What is my tax liability? How is set off?

Menu

set off tax liability

Replies (4)

Recent Topic

- Proprietor have 2 business. One is registered unde

- ITR-4 – Gross Receipts or Turnover for Secti

- Unrelated entries in AIS and Form 26as

- Payment to foreign national

- Internal reconstuction

- IDS Refund – Annexure B & GSTR-3B Match,

- Can i should STCG and LTCG as business income ?

- Capital contribution in Firm

- Form 3CD – Clause 20(b) | ESI Contribution &

- Capital Gains on Dissolution of Partnership

Related Topics

CAclubindia

CAclubindia