Practicing CA

7756 Points

Posted on 15 June 2017

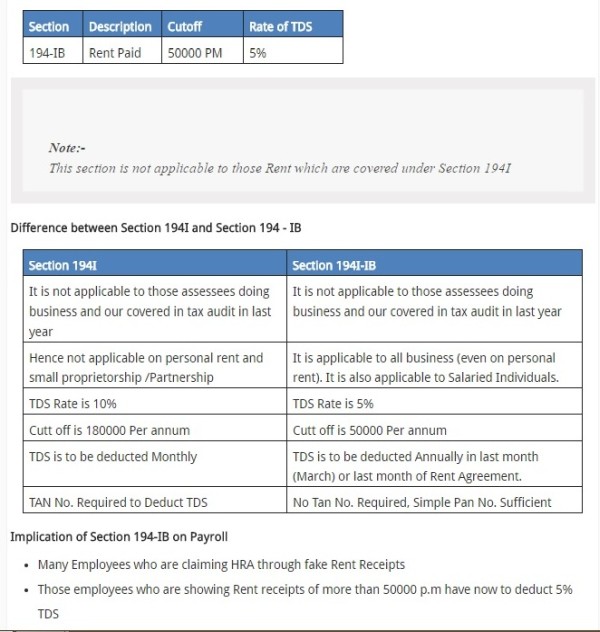

The Finance Bill, 2017 proposes to insert new section 194-IB to provide that an Individual or a HUF (other than those covered under clause (a) 85 (b) of section 44AB of the Act), responsible for paying to a resident any income by way of rent exceeding fifty thousand rupees for a month or part of month during the previous year, shall deduct an amount equal to five per cent. of such income as income-tax thereon. -

CAclubindia

CAclubindia