Asst Mgr-Taxation

6918 Points

Posted on 07 June 2017

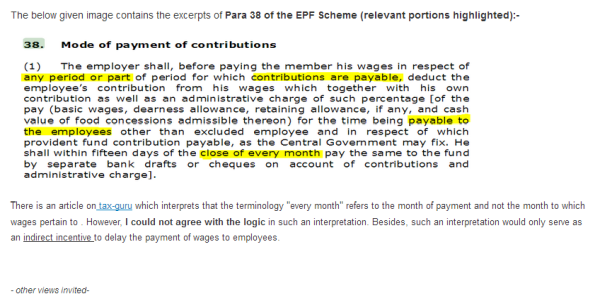

For determining the “due date” for payment of Provident Fund contributions, clause (1) of Paragraph 38 of Employees’ Provident Fund Scheme, 1952 is relevant. It reads as follows:

“The employer shall, before paying the member his wages in respect of any period or part of period for which contribution are payable, deduct the employee’s contribution from his wages which together with his own contribution as well as an administrative charge of such percentage [of the pay (basic wages, dearness allowance, retaining allowance, if any, and cash value of food concessions admissible thereon) for the time being payable to the employees other than an excluded employee and in respect of which provident fund contributions are payable, as the Central Government may fix], he shall within fifteen days of the close of every month pay the same to the Fund by separate Bank drafts or cheques on account of contributions and administrative charge.”

The term ‘month’ has not been defined in the Scheme. Whether “fifteen days from the close of the month” appearing in Paragraph 38 of Employees’ Provident Fund Scheme as to whether:-

- it should be reckoned from the month in which such contributions are received by the assessee from its employees; or

- from the month in respect of which such contributions are received by the assessee, in cases where wages are paid in subsequent month(s).

This ambiguity has been resolved in favour of the assessee, i.e fifteen days are to be reckoned from the close of the month in which employees contributions are recovered i.e the month of payment of wages.

Reliance is placed on the following decisions:-

- Fluid Air (India) Ltd. Vs. D.C.I.T. (1997) 63 ITD 182 (Mumbai)

- Madras Radiators & Pressings Ltd. Vs. D.C.I.T (1996) 59 ITD 515 (Mad.)/ (1996) 56 TTJ (Mad.) 662

CCI

Pro

CCI

Pro

CAclubindia

CAclubindia