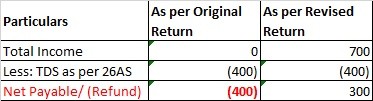

if in original return refund has been claimed and received in assessee,' account and there is some other amount to b reported in revised return on the basis of which there is tax liability than is there liability to pay refund received earlier in original return ,? how to show it in revised return?

Menu

How to show refund to be deposit in revised return

Replies (11)

Recent Topic

- Can i should STCG and LTCG as business income ?

- Capital contribution in Firm

- Form 3CD – Clause 20(b) | ESI Contribution &

- Capital Gains on Dissolution of Partnership

- GST Payment through DRC-03 by cash against notice

- Schedule EI for ITR1

- INCOME TAX DEPARTMENT: DOUBLE STANDARDS

- ITR-4,under presumptive Taxation

- TDS data mismatch with SFT

- Resale of under construction Residential Flat part

Related Topics

CAclubindia

CAclubindia