Date : Aug 06, 2021

On the basis of an assessment of the current and evolving macroeconomic situation, the Monetary Policy Committee (MPC) at its meeting today (August 6, 2021) decided to:

- keep the policy repo rate under the liquidity adjustment facility (LAF) unchanged at 4.0 per cent.

Consequently, the reverse repo rate under the LAF remains unchanged at 3.35 per cent and the marginal standing facility (MSF) rate and the Bank Rate at 4.25 per cent.

- The MPC also decided to continue with the accommodative stance as long as necessary to revive and sustain growth on a durable basis and continue to mitigate the impact of COVID-19 on the economy, while ensuring that inflation remains within the target going forward.

These decisions are in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent, while supporting growth.

The main considerations underlying the decision are set out in the statement below.

Assessment

Global Economy

2. Since the MPC’s meeting during June 2-4, 2021 the pace of global recovery appears to be moderating with the resurgence of infections in several parts of the world, especially from the delta variant of the virus. In June and July, global purchasing managers’ indices (PMIs) slipped from the highs scaled in May. The growing consensus is that the recovery is occurring on a diverging two-track mode. Countries that are ahead in vaccination and have been able to provide or maintain policy stimulus are rebounding strongly. Growth in other economies remains subdued and vulnerable to new waves of infections. There has been a slowing of momentum in global trade volumes in Q2:2021, with elevated shipping charges and logistics costs posing headwinds.

3. There has been a considerable hardening of commodity prices, particularly of crude oil. The latest agreement within the Organisation of Petroleum Countries (OPEC) plus to raise oil production for a likely restoration of output to the pre-pandemic levels by September 2022 imparted transient softening to spot and future crude prices from the recent peak in early July. Headline inflation has ratcheted up in several advanced economies (AEs) as well as most emerging market economies (EMEs), prompting a few central banks in EMEs to tighten monetary policy. In contrast, sovereign bond yields have softened across AEs as markets seem to have acquiesced to the views of central banks that inflation is largely transitory. In EMEs, bond yields remain relatively high on inflation concerns and country-specific factors. In the foreign exchange market, EME currencies have depreciated in the wake of portfolio outflows since mid-June as risk appetite ebbed, while the US dollar has strengthened.

Domestic Economy

4. On the domestic front, economic activity picked up pace in June-July as some states eased pandemic containment measures. As regards agriculture, the south-west monsoon regained intensity in mid-July after a lull; the cumulative rainfall up to August 1, 2021 was one per cent below the long-period average. The pace of sowing of kharif crops picked up in July along with some high frequency indicators of rural demand, notably tractor and fertiliser sales.

5. Reflecting large base effects, industrial production expanded in double digits year-on-year (y-o-y) in May 2021 on top of the massive jump in April, but it was still 13.9 per cent below its May 2019 level. The manufacturing purchasing managers’ index (PMI) that had dropped into contraction to 48.1 in June for the first time in 11 months, rebounded well into expansion zone with a reading of 55.3 in July. High-frequency indicators – e-way bills; toll collections; electricity generation; air traffic; railway freight traffic; port cargo; steel consumption, cement production; import of capital goods; passenger vehicle sales; two wheeler sales –posted strong growth in June/July, reflecting adaptations to COVID related protocols and easing of containment. Services PMI remained in contractionary zone due to COVID-19 related restrictions, though the pace eased to 45.4 in July from 41.2 in June 2021. Initial quarterly results of non-financial corporates for Q1:2021-22 show healthy growth in sales, wage growth and profitability led by information technology firms.

6. Headline CPI inflation plateaued at 6.3 per cent in June after having risen by 207 basis points in May 2021. Food inflation increased in June primarily due to an uptick in inflation in edible oils, pulses, eggs, milk and prepared meals and a pick-up in vegetable prices. Fuel inflation moved into double digits during May-June 2021 as inflation in LPG, kerosene, and firewood and chips surged. After rising sharply to 6.6 per cent in May, core inflation moderated to 6.1 per cent in June, driven by softening of inflation in housing, health, transport and communication, recreation and amusement, footwear, pan, tobacco and other intoxicants (as the effects of the one-off post-lockdown taxes imposed a year ago waned), and personal care and effects (due to sharp reduction in inflation in gold).

7. System liquidity remained ample, with average daily absorption under the LAF increasing from ₹5.7 lakh crore in June to ₹6.8 lakh crore in July and further to ₹8.5 lakh crore in August so far (up to August 4, 2021). Auctions for a cumulative amount of ₹40,000 crore in Q2:2021-22 so far under the secondary market government securities acquisition programme (G-SAP) evened liquidity across illiquid segments of the yield curve. Reserve money (adjusted for the first-round impact of the changes in the cash reserve ratio) expanded by 11.0 per cent y-o-y on July 30, 2021 driven by currency demand. As on July 16, 2021, money supply (M3) and bank credit by commercial banks grew by 10.8 per cent and 6.5 per cent, respectively. India’s foreign exchange reserves increased by US$ 43.1 billion in 2021-22 (up to end-July) to US$ 620.1 billion.

Outlook

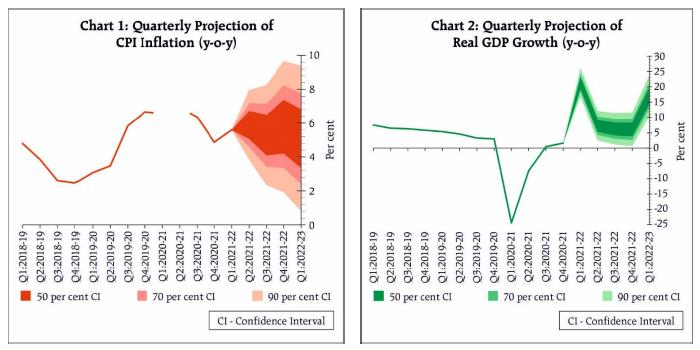

8. Going forward, the revival of south-west monsoon and the pick-up in kharif sowing, buffered by adequate food stocks should help to control cereal price pressures. High frequency indicators suggest some softening of price pressures in edible oils and pulses in July in response to supply side interventions by the Government. Input prices are rising across manufacturing and services sectors, but weak demand and efforts towards cost cutting are tempering the pass-through to output prices. With crude oil prices at elevated levels, a calibrated reduction of the indirect tax component of pump prices by the Centre and states can help to substantially lessen cost pressures. Taking into consideration all these factors, CPI inflation is now projected at 5.7 per cent during 2021-22: 5.9 per cent in Q2; 5.3 per cent in Q3; and 5.8 per cent in Q4 of 2021-22, with risks broadly balanced. CPI inflation for Q1:2022-23 is projected at 5.1 per cent (Chart 1).

9. Domestic economic activity is starting to recover with the ebbing of the second wave. Looking ahead, agricultural production and rural demand are expected to remain resilient. Urban demand is likely to mend with a lag as manufacturing and non-contact intensive services resume on a stronger pace, and the release of pent-up demand acquires a durable character with an accelerated pace of vaccination. Buoyant exports, the expected pick-up in government expenditure, including capital expenditure, and the recent economic package announced by the Government will provide further impetus to aggregate demand. Although investment demand is still anaemic, improving capacity utilisation and congenial monetary and financial conditions are preparing the ground for a long-awaited revival. Firms polled in the Reserve Bank surveys expect expansion in production volumes and new orders in Q2:2021-22, which is likely to sustain through Q4. Elevated levels of global commodity prices and financial market volatility are, however, the main downside risks. Taking all these factors into consideration, projection for real GDP growth is retained at 9.5 per cent in 2021-22 consisting of 21.4 per cent in Q1; 7.3 per cent in Q2; 6.3 per cent in Q3; and 6.1 per cent in Q4 of 2021-22. Real GDP growth for Q1:2022-23 is projected at 17.2 per cent (Chart 2).

10. Inflationary pressures are being closely and continuously monitored. The MPC is conscious of its objective of anchoring inflation expectations. The outlook for aggregate demand is improving, but still weak and overcast by the pandemic. There is a large amount of slack in the economy, with output below its pre-pandemic level. The current assessment is that the inflationary pressures during Q1:2021-22 are largely driven by adverse supply shocks which are expected to be transitory. While the Government has taken certain steps to ease supply constraints, concerted efforts in this direction are necessary to restore supply-demand balance. The nascent and hesitant recovery needs to be nurtured through fiscal, monetary and sectoral policy levers. Accordingly, the MPC decided to keep the policy repo rate unchanged at 4 per cent and continue with an accommodative stance as long as necessary to revive and sustain growth on a durable basis and continue to mitigate the impact of COVID-19 on the economy, while ensuring that inflation remains within the target going forward.

11. All members of the MPC – Dr. Shashanka Bhide, Dr. Ashima Goyal, Prof. Jayanth R. Varma, Dr. Mridul K. Saggar, Dr. Michael Debabrata Patra and Shri Shaktikanta Das – unanimously voted to keep the policy repo rate unchanged at 4.0 per cent.

12. All members, namely, Dr. Shashanka Bhide, Dr. Ashima Goyal, Dr. Mridul K. Saggar, Dr. Michael Debabrata Patra and Shri Shaktikanta Das, except Prof. Jayanth R. Varma, voted to continue with the accommodative stance as long as necessary to revive and sustain growth on a durable basis and continue to mitigate the impact of COVID-19 on the economy, while ensuring that inflation remains within the target going forward. Prof. Jayanth R. Varma expressed reservations on this part of the resolution.

13. The minutes of the MPC’s meeting will be published on August 20, 2021.

14. The next meeting of the MPC is scheduled during October 6 to 8, 2021.

(Yogesh Dayal)

Chief General Manager

Press Release: 2021-2022/644

CAclubindia

CAclubindia

Guest

Notification No : PR : 2021-2022/644Published in Community & General

Source : https://www.rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=52011