What is Transfer Pricing ?????

Transfer pricing relates to the pricing of transactions

(such as transfer of goods, services, intangibles and funds)

It takes place within affiliate segments of a group company in different tax jurisdictions.

It is typically used in situations where Multinational Enterprises (MNEs) seek to cut their tax base by artificially shifting the profits from higher tax jurisdictions to lower tax jurisdictions without a considerable change in business operations.

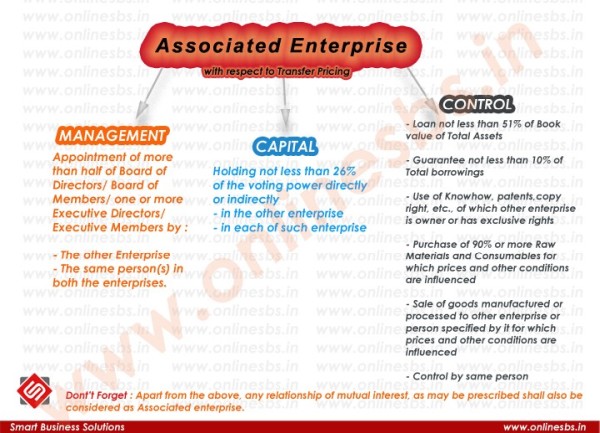

‘International transaction’ means any of the following nature of transactions between

two or more “Associated enterprise” where, either or both of whom are non-residents

In other words if both or all the enterprises executing the transaction are residents,

then it is not an “International Transaction” for the purpose of these provisions

a. purchase,

b. sale,

c. lease of tangible or intangible property,

d. provision of services,

e. lending or borrowing money, or

f. any other transaction having a bearing on the profits, income, losses or

g. assets of such enterprise

What is Transfer pricing as per Tax Perspective?

The price at which one person transfer physical goods and intangibles or provide services to another Associated person

Why This Transfer Pricing?

With the increasing Globalization, the related party transaction between Multinational Enterprise saw a huge revolution; the increase of related party transaction grew so strongly that it was almost 60% of all International transactions. With the rapid rise of multinational trade, the opening of several significant developing economies and transfer pricing’s increased impact on corporate income taxation.

The use of this Transfer Pricing tax strategy attracted a huge level of international attention,

This led to the opening of several significant developing economies and transfer pricing’s increased impact on corporate income taxation. The lopsided distribution of economic resources between different countries is the basis of international trade.

When is Transfer Pricing used?

Transfer Pricing is generally used in situations where Multinational Enterprises seek to cut their taxes by artificially shifting the profits from higher tax jurisdictions to lower tax jurisdictions without a considerable change in business operations.

The TP regime may even be manipulated by small organizations engaging in cross border transactions with affiliated entities.

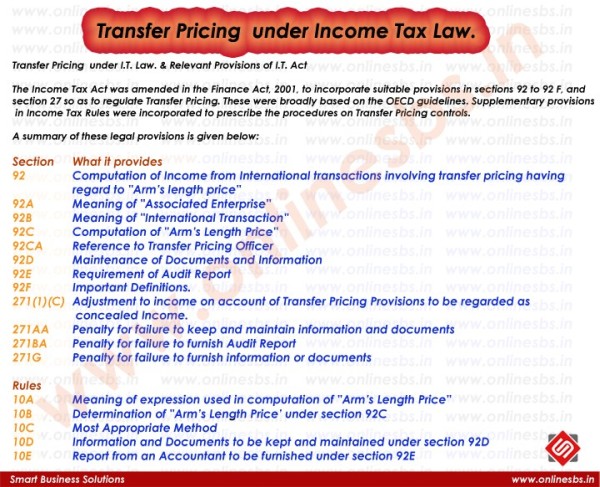

In order to cover such tendencies of MNEs section 92A to 92F have been enacted and section 271AA, 271BA and 271G have been incorporated and section 271 has been amended providing for penal provisions in this regard.

Which Country Suffer ?

A less developed country is more likely to suffer due to TP manipulation than a developed country because of the lack of adequate resources and the inability to monitor transactions. The result is revenue loss and also a drain on foreign exchange reserves

Factors Effecting Transfer Pricing

-

Internal factors:

a. Performance Measurement and

b. Evaluation

-

External Factors:

-

Accounting Standard

-

Income Tax

-

Custom Duty

-

Currency Fluctuations

-

The Issue

1. Pricing Issue

TP relates to the pricing of transactions (such as transfer of goods, services, intangibles and funds) that take place within affiliate segments of a group company in different tax jurisdictions.

Suppose a company LG India (resident of country India which has a tax rate of, say, 40%) manufacture Mobile for Rs.10000/- and sells it to its associated company LG British (resident of country British which has a tax rate of 20%) for Rs.20000/-, who in turn sells in the open market for Rs.40000/-. Had LG India sold it direct, it would have made a profit of 30000 rupees that would have been taxed at 40%. But by routing it through Y, it restricted it to Rs.10000/-, permitting LG British to appropriate the balance to be taxed at 20% only. The transaction between LG India and LG British is arranged and not governed by market forces. The profit of Rs.20000/- is, thereby, shifted to the country LG British. The goods is transferred on a price (transfer price) which is arbitrary or dictated (Rs.20000/-), but not on the market price (Rs.40000/-) so, in effect, the company in country India will have lower profits and therefore a lower tax incidence whereas the company in country British is affected in the opposite manner.

2. Double Taxation Issue (see Diagram)

FOR COMPLETE INFORMATION CLICK HERE

CAclubindia

CAclubindia