What is GST?

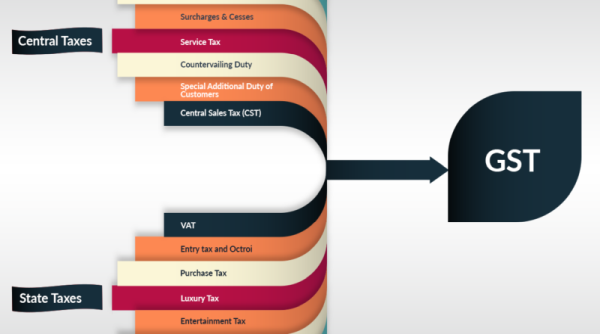

Goods and Service Tax (popularly known as GST) is an Indirect Tax which has subsumed various Indirect such as excise duty, service tax, VAT etc. GST Act was successfully passed in the Indian Parliament on 29th of March, 2017. Though the GST Act came into force from 1st of July 2017; GST Law is a multi-stage, comprehensive, destination-based tax levied at every stage of value addition. In other words, we can say GST in an advance version of VAT applicable on a national level. As the Slogan of GST is given "One Nation, One Tax", GST is one indirect tax for the whole country.

Under the GST system, the tax will be charged at every point of supply of goods or services. In the case of intra-state sales i.e. the location of the supplier and the place of supply are in the same state, CGST and SGST will be levied. However, in Inter-state sales i.e. the location of the supplier and place of supply are in different states, IGST will be levied on the supply.

What are the components of GST?

There are 3 taxes under this GST regime: CGST, SGST/UTGST & IGST.

1. SGST/UTGST: Levied on an intra-state sale (Eg: Within Uttar Pradesh/Chandigarh) and collected by the State Government.

2. CGST: Levied on an intra-state sale (Eg: Within Maharashtra) and collected by the Central Government.

3. IGST: Levied on inter-state sale and collected by the Central Government (Eg: West Bengal to Tamil Nadu)

|

Transaction |

GST Regime |

Old Regime |

Fundamental of GST Regime |

|

Sale within the State i.e. Intra-state Supply |

SGST + CGST |

Central Excise/Service tax + VAT |

Revenue collected will be shared equally between the Central and the State governments |

|

Sale to another State i.e. Inter-state Supply |

IGST |

Excise/Service Tax + CST |

Only IGST will be levied on such supply. The Central then will share the IGST revenue based on the destination of goods. |

Advantages Of GST

As mentioned above that the Goods and Service Tax will subsume most of the indirect taxes and will comprehensively remove the Cascading effect on the supply of goods and services. The Removal of cascading effect i.e. tax on tax will help in reducing the cost of goods.

One of the greatest factors that will make GST operations more user-friendly and effective is the technology. GST is a technology-driven taxing mechanism. All activities such as registration, invoicing, filing returns, refund applications and response to notice will be done through GST online Portal. This will surely speed up the whole processes.

Illustration:

- Let us suppose that a dealer in Karnataka had sold the goods to a dealer in Haryana worth Rs. 10,000. The GST rate is 18% comprising the only IGST. In this case, the supplier will collect Rs. 1,800 as IGST. This revenue will go to the Central Government.

- The same dealer sold goods to a retailer in Karnataka worth Rs. 20,000. The rate of GST on the goods supplied is 12%. This GST rate comprises SGST at 6% and CGST at 6%. The dealer has to collect Rs. 2,400 as GST (Rs.1200 as CGST and Rs.1200 as SGST). Rs. 1,200 will go to the Central Government and an equal amount of Rs. 1200 will go to the Karnataka government as the sale is within the state.

CAclubindia

CAclubindia