Input services ITC also eligible for refund under Inverted duty structure

Last updated: 12 September 2020

Court :

Gujarat High Court

Brief :

Input services ITC also eligible for refund under Inverted duty structure - Analysis of Gujarat HC decision & its impact

Citation :

Introduction:

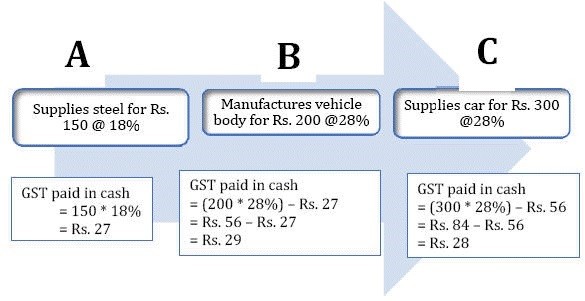

The fundamental principle of GST laws worldwide is that it is a multi-stage tax and tax on value addition, with final consumer alone ultimately bearing the tax. This is ensured by allowing the facility of input credit across the supply chain wherein the tax paid on the previous stage would be given as credit in the hands of the purchaser (popularly known as ‘Input tax credit’ or ITC). For example, Steel supplied by ‘A’ is used to manufacture the body of the vehicle by ‘B’ which is in turn used to manufacture a car by ‘C’. The GST rate on steel is 18%, the vehicle body is 28%, and the car is 28%. The ITC flow is depicted below:

The net effect of ITC facility is that the value addition only gets taxed at each stage in the form of the tax payment in cash.

Instead of the above example of the car, if the example of a tractor is considered and if, tractor attracts GST rate of 12% then ‘D’, a supplier of tractors will supply the tractor at Rs. 300 (value of supply) + Rs. 36 (GST@ 12% on Rs. .300) to the ultimate consumer, ‘D’, the supplier of the tractor would have availed input tax credit of Rs. 56 (tax paid to ‘B’, the supplier of the vehicle body). This ITC would be used to pay GST on tractors of Rs. 36. In such a case, there will be an accumulation of ITC of Rs. .20 (Rs. 56 -36) to C. This is arising due to fact that the GST rate on inward supplies i.e. tractor body is higher (being 28%) than the GST rate on outward supplies of Tractors (being 12%). The consequence that follows is that Rs.20 remains unutilised and keeps on accumulating with no use for taxpayer except showing it as an asset, which runs contrary to the very tenet of GST being consumption tax (namely, only tax in the entire chain is the tax charged to end customer and in the entire supply chain there should not be any sticking or unabsorbed ITC). To mitigate this anomaly, GST law provides for refund of accumulated & unutilised excess ITC.

In this background, Section 54(3) of the CGST Act, 2017 is enacted to provide a refund of the unutilized ITC when the tax rate on inputs being higher than the output. The conjoint reading of Section 54(3), ibid along with associated definitions thereto, all kinds of ITC is refundable irrespective of the category (be it inputs, input services or capital goods). However, the contrary to such clear & unambiguous position, the Rule 89(5) of the CGST Rules, 2017 limits the refund only to the inputs ITC and do not allow the refund of ITC on input services and capital goods. The initial framed Rule 89(5), ibid allowed the refund of ITC on the input services but the rule was retrospectively amended[1] w.e.f. 01.07.2017 to limit the refund of ITC on the inputs alone. The adverse implications of Rule 89(5), ibid is explained with an example:

- Inverted duty turnover: Rs.100 lakhs and liable for GST @12%

- Total tax payable is 12Lakhs

- ITC on inputs: Rs. 15 lakhs

- ITC on input services: Rs. 2 lakhs

- ITC on capital goods: Rs. 5 lakhs

|

S.N |

Scenario |

Eligible Refund (in Rs.) |

|

1 |

All categories of ITC are taken for a refund (Inputs, input services & capital goods) – as per the plain wording of section 54(3), ibid |

10 lakhs (22-12) |

|

2 |

Only inputs ITC is taken for refund calculation [as per the formula given u/r. 89(5)] |

3 Lakhs (15-12) |

|

3 |

Refund restricted (1-2) |

7 Lakhs |

As seen from the comparison above, the rule limiting the refund thereby not fully implementing the mandate of section 54(3) that unutilized ITC shall be refunded.

Recently, the Hon’ble High Court of Gujarat in case of VKC Footsteps India Pvt. Ltd vs. UOI 2020 (7) TMI 726 acknowledging the above anomaly held that Rule 89(5), ibid is ultra vires the provisions of section 54(3), ibid and read down the Rule 89(5), ibid to the extent it restricts the refund of input services ITC.

Implications of the above-said judgement:

- According to the above judgment, input services ITC also would be refundable for all eligible cases of inverted duty refunds.

- Though the Hon’ble HC has not dealt with refundability of capital goods ITC, the rationale & analogy can be adopted in the absence of any express restriction thereto. Consequently, all categories of ITC eligible for the refund.

- Further, the rationale of the said decision can also be adopted for the refund cases of Zero-rated supplies made under LUT wherein the similar restriction is placed on the refund of Capital goods ITC though the principal section 54(3), ibid do not provide for it.

- The CGST is a central law and in absence of any contrary ruling of any HC decision, the Hon’ble Gujarat HC decision can be adopted across India.

The suggested course of action:

While it is expected that the Government may appeal to the Hon’ble Supreme court, the Authors strongly believe that the law in vogue is unambiguous to allow the refund of input services & capital goods ITC. In this background, the suggested course of action is tabulated below:

|

S.N |

Status |

The suggested course of action |

|

1 |

Refund is yet to be applied |

Take total ITC including input services and capital goods while making the refund |

|

2 |

Refund applied but pending for the process |

Request the department to issue deficiency memo & file fresh application adding the total ITC while arriving the eligible refund |

|

3 |

Refund applied considering the inputs ITC alone and it was processed |

File another application covering the input services & Capital goods ITC under ‘any other category’. The readers may note that there is no bar on making an application for the same period twice |

|

4 |

Refund applied considering all types of ITC and it was processed denying the component of input services & Capital goods ITC |

File appeal against the rejection portion |

It is also suggested to make representation to the GST council and Government to amend Rule 89(5), ibid to make it in line with the intentions of the lawmakers.

The authors can also be reached at venkataprasad@hiregange.com, monika@hiregange.com

[1] Notification No. 26/2018 – Central Tax dated 13.06.2018

CA Venkatprasad Pasupuleti

Published in GST

Views : 158

Comments

Trending Online Classes

-

DT & Audit (Exam Oriented Fastrack Batch) - For May 26 Exams and onwards Full English

CA Bhanwar Borana & CA Shubham Keswani

CA Bhanwar Borana & CA Shubham Keswani

CAclubindia

CAclubindia