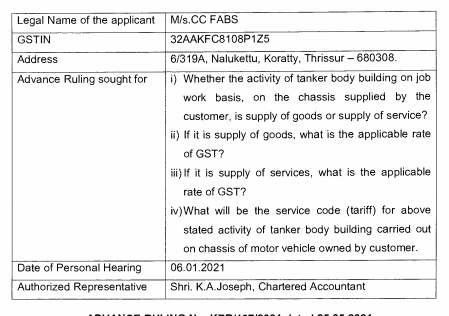

Is activity of tanker body building on job work basis, a supply of goods or services? M/S CC FABS

Court :

KERALA AUTHORITY FOR ADVANCE RULING GOODS AND SERVICES TAX DEPARTMENT

Brief :

The applicant is engaged in tanker body fabrication on the chassis given by the customer on job work basis. The customers purchase chassis and hand over to the applicant for fabricating the tanker body.

Citation :

KER/107/2021

KERALA AUTHORITY FOR ADVANCE RULING

GOODS AND SERVICES DEPARTMENT TAX, TAX TOWER,

OF :Shri. KARAMANA, THIRUVANANTHAPURAM — 695002

BEFORE THE AUTHORITY Sivaprasad S, IRS& : Shri. Senil A K Rajan

The applicant is engaged in tanker body fabrication on the chassis given by the customer on job work basis. The customers purchase chassis and hand over to the applicant for fabricating the tanker body. On receipt of chassis, a work order with the specifications of the tanker body will be raised and on acceptance of the same by customer, the materials used for structural fabrication of tanker will be procured and tanker body will be built on the chassis. The processes involved in the manufacturing activity are; (a) receiving chassis at workshop; (b) purchase of raw steel; (c) cutting and bending of raw materials; (d) welding of all cut and bend parts; (e) assembly of all fabricated parts and statutory parts; and (f) final product on chassis and delivery of the tanker with license.

Please find attached the enclosed file for the full judgement

FAQ :

Poojitha Raam Vinay

Published in GST

Views : 238

downloaded 226 times

Comments

Trending Online Classes

-

DT & Audit (Exam Oriented Fastrack Batch) - For May 26 Exams and onwards Full English

CA Bhanwar Borana & CA Shubham Keswani

CA Bhanwar Borana & CA Shubham Keswani

CAclubindia

CAclubindia