Companies Act, 2013 for the first time had mandated electronic voting for all listed companies and other unlisted public companies having not less than 1000 shareholders and the AGMs held for the financial year ended 31.03.2014 witnessed the application of these provisions. However, for the AGM to be held for financial year ended 31.03.2015, the requirements of e-voting have undergone complete change by virtue of the Companies (Management and Administration) Amendment Rules, 2015 issued by MCA on 19th March, 2015.

Given below is a detailed analysis of the concept of e-voting mandated by the Companies Act, 2013 read with Companies (Management and Administration Rules), 2014 and the Listing Agreement as applicable on date.

MEANING OF SOME IMPORTANT TERMS

Voting by Electronic Means

“Voting by electronic means” includes remote e-voting and voting at the general meeting through an electronic voting system which may be the same as used for remote e-voting.

Electronic voting system

‘‘electronic voting system’’ means a ‘secured system’ based process of display of electronic ballots, recording of votes of the members and the number of votes polled in favour or against, in such a manner that the entire voting exercised by way of electronic means gets registered and counted in an electronic registry in a centralized server with adequate cyber security.

Remote e-voting

''remote e-voting'' means the facility of casting votes by a member using an electronic voting system from a place other than venue of a general meeting;

Cut-off Date

"cut-off date" means a date not earlier than seven days before the date of general meeting for determining the eligibility to vote by electronic means or in the general meeting;

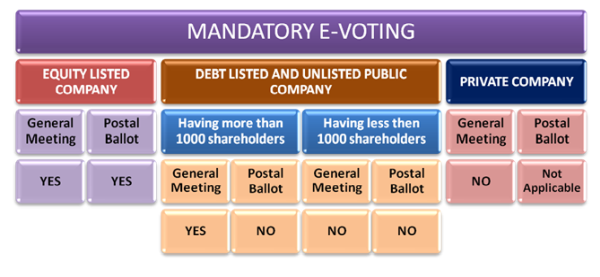

WHEN AND FOR WHOM E-VOTING IS MANDATORY?

a. As per Rule 20 of Companies (Management and Administration) Rules, 2014, as amended by the Companies (Management and Administration) Amendment Rules, 2015 e-voting is mandatory in case of all general meetings of

i. Every company other than a company referred to in chapter XB or chapter XC of the SEBI ICDR Regulations 2009 having its equity shares listed on a recognised stock exchange; and

ii. a company having not less than 1000 shareholders

b. As per clause 35B of equity listing agreement (amended vide SEBI Circular No. CFD/POLICY CELL/2/2014, DATED 17-4-2014), e-voting is mandatory in respect of all shareholders' resolutions, to be passed at General Meetings or through postal ballot.

This means that in case of companies whose equity shares are listed on a recognized stock exchange, e-voting facility needs to be necessarily provided both in case of convening a general meeting physically as well as resolutions being passed through postal ballot process.

REQUIREMENTS AND PROCEDURE TO BE FOLLOWED FOR PROVIDING

E-VOTING FACILITY IN RELATION TO ANNUAL GENERAL MEETINGS

1. Appointment of scrutinizer to scrutinize the e-voting process

a. Board of Directors has to appoint a scrutinizer after ascertaining his/her availability and willingness to be appointed as scrutinizer to scrutinize the e-voting process.

b. Any Company Secretary, Chartered Accountant, Cost Accountant, in practice, or an advocate, or any other person who is not in employment of the company and is a person of repute who, in the opinion of the Board can scrutinise the voting and remote e-voting process in a fair and transparent manner.

2. Finalisation of notice of general meetings

Additional requirements relating to notice:

a. Notice can be sent only through registered post, speed post, courier or through electronic means at the registered email Id.

b. Notice has to be placed on the website of the company and of the agency which is providing the e-voting platform, forthwith after it is sent to the members.

The notice of the meeting shall clearly state that:

a. company is providing facility for voting by electronic means and the business may be transacted through such voting;

b, that the facility for voting either through electronic voting system or ballot or polling paper shall also be made available at the meeting and members attending the meeting who have not already cast their vote by remote e-voting shall be able to exercise their right at the meeting;

c. that the members who have cast their vote by remote e-voting prior to the meeting may also attend the meeting but shall not be entitled to cast their vote again;

The notice shall

a. clearly indicate the process and manner for voting by electronic means;

b. indicate the time schedule including the time period during which the votes may be cast by remote e-voting;

c. provide the details about the login ID;

d. specify the process and manner for generating or receiving password and for casting of vote in a secure manner.

3. Publication of newspaper advertisement

Company has to publish a newspaper advertisement immediately on completion of despatch of notices for the meeting but at least 21 days before the date of general meeting, at least once in a vernacular newspaper in the principle vernacular language and at least once in an English newspaper in English Language about having sent the notice of the meeting and the advertisement should also contain the following details:

a. statement that the business may be transacted through voting by electronic means;

b. the date and time of commencement of remote e-voting;

c. the date and time of end of remote e-voting;

d. cut-off date;

e. the manner in which persons who have acquired shares and become members of the Company after the despatch of notice may obtain the login ID and password;

the statement that –

a. remote e-voting shall not be allowed beyond the said date and time;

b. the manner in which the company shall provide for voting by members present at the meeting; and

c. a member may participate in the general meeting even after exercising his right to vote through remote e-voting but shall not be allowed to vote again in the meeting; and

d. a person whose name is recorded in the register of members or in the register of beneficial owners maintained by the depositories as on cut-off date shall only be entitled to avail the facility of remote e-voting as well as voting in the general meeting;

e. website address of the company, if any, and of the agency where notice of the meeting is displayed; and

f. name, designation, address, email id and phone number of the person responsible to address the grievances connected with facility for voting by electronic means.

The public notice as above has to be placed on the website of the company and of the e-voting agency.

4. Period for which e-voting has to be remain open

a. E-voting shall remain open for a minimum of 3 days.

b. E-voting has to be close at 5.00 P.M. on the date preceding the date of the general meeting.

c. All the shareholders, whether holding shares in physical mode or Demat mode as on cut-off date can cast their votes through remote e-voting during the period which remote e-voting remains open.

d. Votes once cast cannot be recast or changed thereafter.

e, A member may participate in the general meeting even after exercising his right to vote through remote e-voting but shall not be allowed to vote again

5. Procedure on closure of remote e-voting period

a. On closing of the remote e-voting period, the facility should be blocked forthwith.

b. If a company opts to provide the same electronic voting system as used during remote e-voting during the general meeting, the said facility shall be in operation till all the resolutions are considered and voted upon in the meeting and may be used for voting only by the members attending the meeting and who have not exercised their right to vote through remote e-voting.

c. During the general meeting, at the end of the discussion on the resolutions on which voting is to be held, the Chairman should allow voting with the assistance of scrutinisers by use of ballot or polling paper or by using an electronic voting system for all those shareholders who are present at the general meeting but have not cast their votes through remote e-voting.

d. The manner in which members have cast their votes, that is, affirming or negating the resolution, shall remain secret and not available to the Chairman, Scrutiniser or any other person till the votes are cast in the meeting.

e. The scrutiniser shall, immediately after the conclusion of voting at the general meeting, first count the votes cast at the meeting, thereafter unblock the votes cast through remote e-voting in the presence of at least 2 witnesses not in the employment of the company and make, not later than 3 days of conclusion of the meeting, a consolidated scrutiniser's report of the total votes cast in favour or against, if any, to the Chairman or a person authorised by him in writing who shall countersign the same.

6. Declaration of result

a. The Chairman or a person authorised by him in writing shall declare the result of the voting forth once the report by Scrutiniser is tendered.

b. The results declared along with the report of the scrutiniser shall be placed on the website of the company, if any, and on the website of the agency immediately after the result is declared by the Chairman.

c. The company shall, simultaneously, forward the results to the concerned stock exchange or exchanges where its equity shares are listed and such stock exchange or exchanges shall place the results on its or their website.

d. Subject to receipt of requisite number of votes, the resolution shall be deemed to be passed on the date of the relevant general meeting.

e. A resolution proposed to be considered through voting by electronic means shall not be withdrawn.

VOTING BY POLL

ON WHOSE REQUEST/DEMAND POLL WILL BE TAKEN?

a. On Chairman’s own motion, or

b. In case of company having share capital, on a demand raised by members present either in person or proxy, where allowed, and having not less than 1/10th of the total voting power or holding shares on which an aggregate sum of not less than Rs. 5 Lakhs or such higher amount as may be prescribed has been paid-up; and

The demand for a poll may be withdrawn at any time by the persons who made the demand.

WHEN CAN POLL BE DEMANDED?

Poll can be demanded at any time before or on the declaration of result of voting by show of hands.

WITHIN WHAT TIME POLL HAS TO BE TAKEN?

A poll demanded for adjournment of the meeting or appointment of Chairman of the meeting shall be taken forthwith.

A poll demanded on any question other than adjournment of the meeting or appointment of Chairman shall be taken at such time, not being later than 48 hours from the time when the demand was made, as the Chairman of the meeting may direct.

BRIEF PROCEDURE FOR TAKING POLL

a. Chairman of the meeting has the power to regulate the entire poll process and he shall appoint scrutinizer(s) to scrutinize the poll process.

b. The scrutinizer will be provided with all the necessary papers and he shall arrange for polling papers and distribute them to the members and proxies present at the meeting.

c. The Scrutinizers shall count the votes cast on poll, prepare a report thereon addressed to the Chairman and submit the same to the chairman who shall countersign the same.

d. The Chairman shall declare the result of Voting on poll.

VOTING BY POSTAL BALLOT

DEFINITION OF POSTAL BALLOT

Section 2(65) of the Companies Act, 2013 defines postal ballot as below:

“postal ballot” means voting by post or through any electronic mode;

Even though the above definition is not very clear, it gives a fair idea about the meaning of postal ballot and also provides clarity that the Companies Act, 2013 has recognized the medium of e-voting for the purpose of postal ballot.

APPLICABILITY OF POSTAL BALLOT

Provisions regarding postal ballot are primarily contained in Section 110 of the Act read with Rule 22 of Companies (Management and Administration) Rules, 2014.

In respect of certain items of business to be transacted by certain companies, the Act mandates that the approval of members has to be sought only by means of a postal ballot. Thus the mandatory applicability needs to be understood from two angles; one from the angle of nature of item of business to be transacted and secondly from the point of view of class of the company. We list below both the dimensions as under:

CLASS OF COMPANIES FOR WHOM POSTAL BALLOT IS MANDATORY:

Except a One Person Company and other companies having upto 200 members, all other companies shall transact the items of business listed below only by means of voting through a postal ballot.

ITEMS OF BUSINESS WHICH NEED TO BE MANDATORILY TRANSACTED THROUGH POSTAL BALLOT:

1. Alteration of the objects clause of the memorandum and in the case of the company in existence immediately before the commencement of the Act, alteration of the main objects of the memorandum;

2. Alteration of articles of association in relation to insertion or removal of provisions which, under sub-section (68) of section 2, are required to be included in the articles of a company in order to constitute it a private company;

3. Change in place of registered office outside the local limits of any city, town or village as specified in sub-section (5) of section 12;

4. Change in objects for which a company has raised money from public through prospectus and still has any unutilized amount out of the money so raised under sub-section (8) of section 13;

5. Issue of shares with differential rights as to voting or dividend or otherwise under sub-clause (ii) of clause (a) of section 43;

6. Variation in the rights attached to a class of shares or debentures or other securities as specified under section 48;

7. Buy-back of shares by a company under sub-section (1) of section 68;

8. Election of a director under section 151 of the Act;

9. Sale of the whole or substantially the whole of an undertaking of a company as specified under sub-clause (a) of sub-section (1) of section 180;

10. giving loans or extending guarantee or providing security in excess of the limit specified under sub-section (3) of section 186

The mandatory applicability of postal ballot can be summarized as under:

List of items of business which cannot be transacted through postal ballot

The Act specifies certain items of business which cannot be transacted by means of postal ballot, i.e. which should be transacted only in a duly convened meeting of the members. These are –

All items of business which are deemed as Ordinary Business at an Annual General Meeting, i.e.

(i) the consideration of financial statements and the reports of the Board of Directors and auditors;

(ii) the declaration of any dividend;

(iii) the appointment of directors in place of those retiring;

(iv) the appointment of, and the fixing of the remuneration of, the auditors;

Any business in respect of which directors or auditors have a right to be heard at any meeting, like removal of a director or auditor etc.

All other items of business other than the aforementioned businesses can be transacted through postal ballot, instead of transacting such business at a general meeting.

If a resolution is assented to by the requisite majority of the shareholders by means of postal ballot, it shall be deemed to have been duly passed at a general meeting convened in that behalf.

The position with regards to transaction of business through postal ballot/general meeting can be summarized as under:

a. Certain items of business as listed above in case of companies having 200 or more shareholders need to be mandatorily transacted though postal ballot.

b. Certain items of business as listed above require to be transacted only at duly convened general meetings.

c. All other items of business can either be transacted through a general meeting or through postal ballot.

d. Companies having less than 200 shareholders are not mandated to transact any business through postal ballot.

METHOD OF VOTING FOR POSTAL BALLOT

The definition of postal ballot states that postal ballot means voting by post or through any electronic means. This means that a postal ballot exercise recognizes both methods of voting i.e. physical voting through post and e-voting through electronic means.

Section 108 of the Act read with Rule 20 of Companies (Management and Administration) Rules, 2014 which provides for voting by electronic means states that certain companies have to mandatorily provide e-voting facility in case of voting at a general meeting.

Section 110 of the Act read with Rule 22 of Companies (Management and Administration) Rules, 2014, which contains provisions dealing with postal ballot, do not contain any clear stipulation regarding mandatory requirement of voting through electronic means in case of a postal ballot except that it is stated in Rule 22 that “The provisions of rule 20 regarding voting by electronic means shall apply, as far as applicable, mutatis mutandis to this rule in respect of the voting by electronic means.”

Clause 35B of the listing agreement as amended vide SEBI Circular No. CFD/POLICY CELL/2/2014, dated 17-4-2014 provides that e-voting is mandatory in respect of all shareholders' resolutions, to be passed at General Meetings or through postal ballot. This means that in case of listed companies, e-voting facility needs to be necessarily provided both in case of convening a general meeting physically as well as resolutions passed through postal ballot process.

A snapshot of the mandatory requirement of e-voting for general meetings and for voting through postal ballot considering the provisions of both Companies Act, 2013 and listing agreement are given below:

PROCEDURE FOR CONDUCTING POSTAL BALLOT

PROCEDURE FOR CONDUCTING POSTAL BALLOT

1. Passing of Board resolution for the purpose of approval of draft notice of postal ballot and other related documents and appointment of scrutinizer and appointment of agency to provide e-voting platform in case e-voting facility is being provided.

2. Printing of Postal ballot notice and postal ballot form and other related documents for despatch to those shareholders to whom documents have to be sent by physical means.

3. Completion of despatch of postal ballot notice and related documents to all shareholders. As per Rule 20(2), the notice shall be sent either (a) by Registered Post or speed post, or (b) through electronic means like registered e-mail id or (c) through courier service for facilitating the communication of the assent or dissent of the shareholder to the resolution.

4. The Share holders are required to given their assent or dissent in writing within a period of 30 days from the date of dispatch of the notice. The assent or dissent received after 30 days from the date of issue of notice shall be treated as if reply from the member has not been received.

5. Posting of the notice of postal ballot on the website of the company forthwith after the notice is sent to the members and such notice shall remain on such website till the last date for receipt of the postal ballots from the members.

6. Intimating the stock exchanges where the securities of the company are listed regarding completion of despatch of postal ballot notices.

7. Publication of an advertisement at least once in a vernacular newspaper in the principal vernacular language of the district in which the registered office of the company is situated, and having a wide circulation in that district, and at least once in English language in an English newspaper having a wide circulation in that district, about having dispatched the ballot papers and specifying therein, inter alia, the following matters, namely:-

a. statement to the effect that the business is to be transacted by postal ballot which includes voting by electronic means;

b. the date of completion of dispatch of notices;

c. the date of commencement of voting;

d. the date of end of voting;

e. the statement that any postal ballot received from the member beyond the said date will not be valid and voting whether by post or by electronic means shall not be allowed beyond the said date;

f. a statement to the effect that members, who have not received postal ballot forms may apply to the company and obtain a duplicate thereof; and

g. contact details of the person responsible to address the grievances connected with the voting by postal ballot including voting by electronic means.

8. Postal ballot received back from the shareholders shall be kept in the safe custody of the scrutinizer and after the receipt of assent or dissent of the shareholder in writing on a postal ballot, no person shall deface or destroy the ballot paper or declare the identity of the shareholder.

9. On closure of the voting period, the scrutinizer shall assess the result of the voting, both through physical ballot papers and through e-voting and shall maintain a register either manually or electronically to record the assent or dissent received, mentioning the particulars of name, address, folio number or client ID of the shareholder, number of shares held by them, nominal value of such shares, whether the shares have differential voting rights, if any, details of postal ballots which are received in defaced or mutilated form and postal ballot forms which are invalid.

10. The scrutinizer shall submit his report as soon as possible after the last date of receipt of postal ballots but not later than 7 days thereof.

11. The results shall be declared by placing it, along with the scrutinizer’s report, on the website of the company.

12. Intimating stock exchange where the securities of the company are listed regarding result of postal ballot.

13. If a resolution is assented to by the requisite majority of the shareholders by means of postal ballot, it shall be deemed to have been duly passed at a general meeting convened in that behalf.

14. The postal ballot and all other papers relating to postal ballot including voting by electronic means, shall be under the safe custody of the scrutinizer till the chairman considers, approves and signs the minutes and thereafter, the scrutinizer shall return the ballot papers and other related papers or register to the company who shall preserve such ballot papers and other related papers or register safely.

15. The minutes of resolutions passed through postal ballot have to be recorded and maintained as per the requirements specified in Section 118 and 119 of the Act read with the Rules made thereunder

16. Relevant forms need to be filed with the Registrar of Companies for intimating passing of resolutions by the members as applicable.

WRAP UP

The Companies (management and Administration) Amendment Rules, 2015 have brought enormous changes in the provisions and procedure relating to e-voting. For Equity Listed Companies, the Listing Agreement clearly specifies that e-voting is mandatory for all shareholders’ resolutions be it through a general meeting or through postal ballot. However, this type of clarity seems to be missing in the Companies Act, 2013 due to the reason that the Act states that e-voting has to be necessarily provided in relation to general meetings of equity listed companies and those companies having more than 1000 shareholders but for postal ballot it merely states that postal ballot means voting by post or any electronic means. This creates a grey area regarding the mandatory applicability of e-voting in case of postal ballot for Companies whose only debt securities are listed or unlisted companies having more than 1000 shareholders.

CAclubindia

CAclubindia