PROVISIONS RELATING TO ISSUE OF SHARE CERTIFICATES UNDER COMPANIES ACT 2013

Share Certificates which are duly issued and held in compliance with provisions of law are deemed to be evidence of title of the person to the shares contained therein. It is for this reason that share certificates assume significant importance. In the present write up, we have put forth the provisions relating to issue of Share Certificates as contained in the Companies Act, 2013(Act) read with the relevant draft rules.

SHARE CERTIFICATE AS EVIDENCE OF TITLE

Section 46 of the Act contains that a certificate, issued under the common seal of the company, specifying the shares held by any person, shall be prima facie evidence of the title of the person to such shares. Further, where a share is held in depository form, the record of the depository is the prima facie evidence of the interest of the beneficial owner.

MANNER OF ISSUANCE OF SHARE CERTIFICATES

Notwithstanding anything contained in the Articles of Association of the company, share certificates have to be issued in the manner prescribed below:

Checks before issue of Share Certificates

· Share Certificates should be issued only pursuant to a resolution of the Board of Directors.

· Letter of allotment needs to be surrendered to the company except in cases of issues against letters of acceptance or of renunciation, or in cases of issue of bonus shares.

· In case the letter of allotment is lost or destroyed, the Board may impose such reasonable terms, if any, as to seek supporting evidence and indemnity and the payment of out-of-pocket expenses incurred by the company in investigating evidence, as it may think fit.

Format of Share Certificate

· Every certificate of share or shares shall be in Form No. 4.1 or as near thereto as possible and shall specify the name(s) of the person(s) in whose favor the certificate is issued, the shares to which it relates and the amount paid-up thereon.

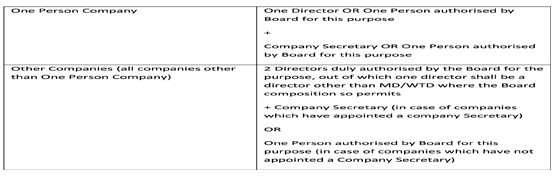

· Every Share Certificate has to be issued under the common seal of the company, which shall be affixed in presence of and signed by directors/authorised representatives in the manner prescribed below:

· Share certificates can be digitally signed by a director by electronic means or the signature of the director may be printed on the share certificate as a facsimile signature by means of any machine, equipment or other mechanical means such as engraving in metal or lithography, but not by means of a rubber stamp. However, the director concerned shall be personally responsible for permitting the affixation of his signature as aforesaid and the safe custody of any machine, equipment or other material used for the purpose.

Entry in Register of Members

· Particulars of every share certificate issued as above shall be entered in the Register of Members maintained in accordance with section 88 along with the name(s) of person(s) to whom it has been issued, indicating the date of issue.

ISSUANCE OF RENEWED/DUPLICATE SHARE CERTIFICATES

Circumstances in which duplicate share certificate may be issued

A duplicate certificate of shares may be issued, if—

1. Share certificate is proved to have been lost or destroyed; or

2. has been defaced, mutilated or torn or old, decrepit, worn out, or

3. where shares are sub-divided or consolidated, or

4. where the cages on the reverse for recording transfers have been duly utilized

Manner of issuance of duplicate share certificates

· Where original certificate is lost or destroyed –

o Prior consent of Board to be obtained for issuance of duplicate share certificate.

o Company to collect fees not exceeding rupees fifty per certificate and impose such reasonable terms, as the Board thinks fit, such as furnishing supporting evidence and indemnity and the payment of out-of-pocket expenses incurred by the company in investigating the evidence produced.

o The words “Duplicate” and “duplicate issued in lieu of share certificate No......” to be stated prominently on the face of the share certificate and also recorded in the Register maintained for the purpose.

· In all other cases -

o The certificate in lieu of which a duplicate is required to be issued should be surrendered to the company.

o The company may charge such fee as the Board thinks fit, not exceeding Rs. 20/- per certificate, issued on splitting or consolidation of share certificates or in replacement of share certificates that are defaced, mutilated, torn or old, decrepit or worn out.

o The words ““Issued in lieu of share certificate No..... sub-divided/replaced/on consolidation” shall be stated on the face of the duplicate share certificate and also recorded in the Register maintained for the purpose.

o A company may replace all the existing certificates by new certificates upon sub-division or consolidation of shares or merger or demerger or any reconstitution without requiring old certificates to be surrendered subject to compliance with other rules discussed above.

Register of Renewed and Duplicate Share Certificates

· Register of renewed and duplicate share certificates to be maintained in Form No. 4.2, mentioning therein following details:

o name(s) of the person(s) to whom the certificate is issued,

o the number and date of issue of the share certificate in lieu of which the new certificate is issued, and

o necessary changes indicated in the Register of Members by suitable cross-references in the “Remarks” column.

· Such register shall be kept at the registered office of the company or at such other place where the Register of Members is kept.

· The register shall be preserved permanently and shall be kept in the custody of the secretary of the company or any other person authorized by the Board for the purpose.

· All entries made in the Register of Renewed and Duplicate Share Certificates shall be authenticated by the secretary or such other person as may be authorized by the Board for purposes of sealing and signing the share certificates.

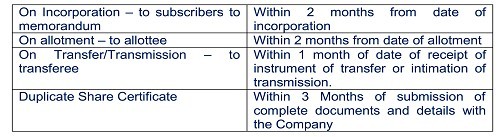

TIME LIMIT FOR ISSUANCE OF SHARE CERTIFICATES

· As per Section 56(4), every company shall, unless prohibited by any provision of law or any order of Court, Tribunal or other authority, deliver the certificates of all securities allotted, transferred or transmitted within the time lines mentioned below –

· Where the shares are dealt with in a depository, the company shall intimate the details of allotment of shares to depository immediately on allotment of such shares.

MAINTENANCE OF SHARE CERTIFICATE FORMS AND RELATED BOOKS AND DOCUMENTS

· All blank forms to be used for issue of share certificates shall be printed and the printing shall be done only on the authority of a resolution of the Board.

· The blank forms shall be consecutively machine-numbered and the forms and the blocks, engravings, facsimiles and hues relating to the printing of such forms shall be kept in the custody of the secretary or such other person as the Board may authorize for the purpose; and the secretary or other person aforesaid shall be responsible for rendering an account of these forms to the Board.

· Maintenance, preservation and safe custody of all books and documents relating to the issue of share certificates, including the blank forms of share certificates shall be the responsibility of the Company Secretary, where the company has a company secretary, otherwise a Director specifically authorized by the Board for such purpose (where the company has no company secretary).

· All books referred as above shall be preserved in good order permanently.

· All certificates surrendered to a company shall immediately be defaced by stamping or printing the word “cancelled” in bold letters and may be destroyed after the expiry of 3 years from the date on which they are surrendered, under the authority of a resolution of the Board and in the presence of a person duly appointed by the Board in this behalf except in case of dematerialization of securities.

PENALTY FOR FRAUDULENT ISSUE OF SHARE CERTIFICATES

If a company with intent to defraud, issues a duplicate certificate of shares, the company shall be punishable with fine which shall not be less than five times the face value of the shares involved in the issue of the duplicate certificate but which may extend to ten times the face value of such shares or Rs. 10 Crores whichever is higher and every officer of the company who is in default shall be liable for action under section 447.

SERVICE TAX UPDATES

· Services provided by a canteen, in relation to serving food or beverages, maintained in a Factory covered under the Factories Act 1948 having the facility of Central Air conditioning or central Air-heating are exempted vide notification no.14/2013-ST dt. 22nd October 2013 by way of amendment to Mega exemption.

· Clarification has been given vide circular no.173/8/2013-ST dt.7th October 2013 in respect of the services provided by canteens in relation to serving of food beverages, eating joints or mess having the facility of central Air-conditioning or central Air-heating attracts the levy of service tax subject to the above exemption. However, service provided by a canteen in relation to serving of food or beverages not having the facility of central Air-conditioning or central Air-heating do not attract levy of service tax.

· IMPORTANT: Service Tax Department is making specific request to all the eligible assessees to avail the benefit of Voluntary Compliance Encouragement Scheme 2013 and take benefit of interest and penalty and subsequent prosecution.

CAclubindia

CAclubindia