Provision of Ratification of Auditor: {First Provision of 139(1)}

Act Language: The Company shall place the matter relating to such appointment for Ratification by members at every Annual General Meeting.

Rule 3(7) Proviso: Appointment of Statutory Auditor shall be subject to ratification in every annual general meeting till the sixth such meeting by way of passing of an ordinary resolution

“As per the above proviso Companies are required to ratify the appointment of Statutory Auditors who was appointed in last AGM for 5 financial years. Therefore from this year, every year in AGM an Ordinary Resolution is to be passed for ratification to continue as Statutory Auditor of the Company.”

If the Statutory Auditor is not ratified in AGM then it will be consider as CASUAL VACANCY.

|

FAQ’S |

|

|

A. |

Whether it is power in the hand of shareholders to ratify continuation of Statutory Auditors. |

|

Yes, This is power in the hand of Shareholders to ratify continuation of Auditor or Not. {As per provision of 139(1) first proviso) |

|

|

B. |

If at AGM Ratification is not made by the Shareholder then how it will consider. |

|

It will consider as casual Vacancy. {Section 139(8)(i)} |

|

|

C. |

How to Appoint new auditor in case of non ratification? |

|

Appoint auditor as filing of casual vacancy. Process in detail discussed below. |

|

|

D. |

What will be the term of auditor appointed due to Casual Vacancy? |

|

Term of such appointment will be upto conclusion of next Annual General Meeting. |

|

|

E. |

Whether the dis-continue auditor need to file ADT-3 with ROC not. |

|

Discontinue auditor will not file ADT-3 because it’s not resignation of Auditor. |

|

|

F. |

Whether need to file any form for appointment of proposed auditor |

|

Yes, ADT-1 required to file within 15 days of passing of Board Resolution. |

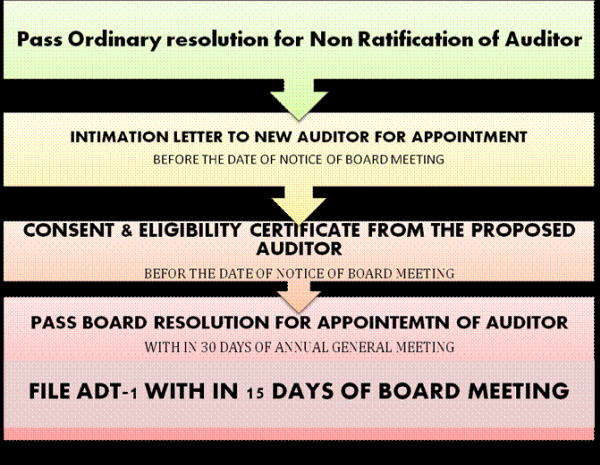

PROCESS FOR RATIFICATION OF AUDITOR

PROVISIONS RELATING TO CASUAL VACANCY

Power of Appointment:

The Board of Directors of a Company has the power to fill up any casual vacancy in the office of an auditor except casual vacancy caused by resignation of an auditor.

Term of such Appointment:

Such Statutory Auditor shall hold office till the conclusion of the next Annual General Meeting.

Filing Requirement:

The Company shall inform the Auditor concerned of his appointment and file a notice of such appointment in e-form ADT-1 with the ROC within 15 days of the meeting in which the auditor is appointed.

DRAFTS FOR THE REFERENCE:

Draft board resolution:

“RESOLVED THAT M/s ABC & Company, the Chartered Accountants, (FRN:___________) Delhi- 110085, be and are hereby appointed as Statutory Auditor of the Company to fill up the casual vacancy caused by the resignation of the M/s. PQR & Associates, the Chartered Accountants, (FRN: ____________), until the conclusion of the next Annual General Meeting of the Company at a remuneration of Rs. . . . . . . Plus reimbursement of any out- of- pocket expenses that may be incurred, in connection with the audit.”

CAclubindia

CAclubindia