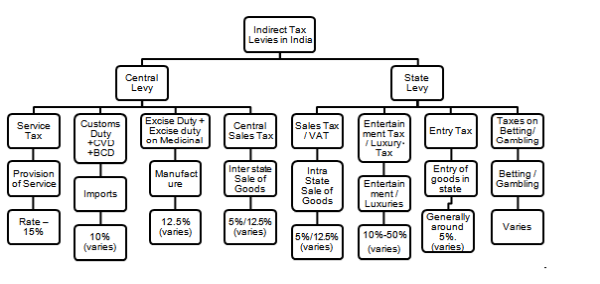

GST Overview

GST stands for Goods and Services Tax, which will be levied on the supply of goods or services or both in India. The introduction of Goods and Services Tax (GST) would be a very significant step in the field of indirect tax reforms in India. By Combining a large number of Central and State taxes into a single tax, it would mitigate cascading or double taxation in a major way and pave the way for a common national market. Introduction of GST would also make Indian products competitive in the domestic and international markets. It would be easier to administer because of its transparent and self-policing character.

Features of GST

- Destination based Consumption Tax

- GST to be levied on supply of goods or services except-

- Exempted goods / services - common list for CGST & SGST

- Goods / services outside the purview of GST

- Transactions below threshold limit

- Dual Administration

- Levied and Collected by Center - CGST

- Levied and Collected by State - SGST

- PAN Based Registration.

- Registration only if turnover more than Rs.20 lakhs.

- System of floor GST rating compliance for standard goods and services.

- Option of Voluntary Registration and Deemed Registration in three days

- Input Tax Credit available on taxes paid on all procurements (except few specified items) and Cross utilization of IGST Credit first as IGST and then as CGST or SGST /UTGST.

- Set of auto-populated Monthly returns and Annual Return

- CGST & SGST on intra-State supplies of goods / services in India

- IGST levied and collected by the Centre, which applies to

- Inter-State supplies of goods / services in India

- Inter-State stock transfers of goods

- Import of goods / services

- Export of goods / services

- All goods or services likely to be covered under GST except:

- Alcohol for human consumption - State Excise + VAT

- Electricity - Electricity Duty

- Sale / purchase of Real Estate - Stamp Duty + Property Taxes

- Petroleum Products (to be bought under GST from a later specified date)

- Tobacco Products - under GST + Central Excise

- Optional Compounding scheme for taxpayers having taxable turnover up to a certain threshold above the exemption.

- GSTN and GST Suvidha Providers (GSPs) to provide technology based assistance.

- Separate electronic ledgers for cash and credit.

- Tax can be deposited by internet banking, NEFT / RTGS, Debit/ credit card and over the counter.

- Refund to be granted within 60 days.

- Export of goods / services - Zero rated and Provisional release of 90% refund to exporters within 7 days.

- Interest payable if refund not sanctioned in time and Refund to be directly credited to bank accounts

Why GST?

GST brings the following Benefits to Industry, Government and Consumers

1. Reduction in Multiplicity of Taxes, Cascading and Double Taxation

GST is a destination based consumption tax. Tax credit available at every stage of transaction will eliminate cascading or double taxation of taxes.

2. Common National Market with Uniform Tax Rates and Procedures

3. Reduction in Cost of goods & services to consumers due to elimination of cascading which in turn makes products and services globally competitive.

4. Input Tax Credit Mechanism: GST allows set-off of prior stage taxes for the next stage of transactions and by allowing cross utilization of input tax credits results in reduction of working capital requirement.

5. Simpler Tax System: Harmonization of laws, procedures and rates of tax will make compliance easier and simple. There would be common definitions, common forms/formats, common interface through GST portal, which results in reduction of compliance costs.

6. Transparency in taxation system: As it operates online through GSTN, various process such as registration, returns, refunds, tax payments, etc. will be simplified and automated procedures. And Electronic matching of input tax credit across India will make the process more transparent and accountable.

7. Increase in employment opportunities: GST is expected to create more opportunities for domestic business, which in turn creates more employment.

8. It is expected to increase in exports due to zero rate exports and reduce imports which will cost more or equivalent to domestic goods. Reduces prices resulting in more consumption, which in turn means more production and thereby boosting the growth of industry.

GST Rates

|

Rates |

Goods |

Services |

|

0% |

Food grains |

Education |

|

Cereals |

Healthcare |

|

|

Milk |

Residential accommodation |

|

|

Jaggery |

Hotel/ Lodges with tariff below INR 1000 |

|

|

Common Salt |

||

|

5% |

Coal |

Goods transport |

|

Sugar |

Rail tickets (other than sleeper class) |

|

|

Tea & Coffee |

Economy class air tickets |

|

|

Drugs & Medicine |

Cab aggregators |

|

|

Edible Oil |

Selling space for advertisements in print media |

|

|

Indian Sweets |

||

|

12% |

Fruit Juices |

Works contract |

|

Vegetable Juices |

Business Class air travel |

|

|

Beverages containing milk |

Telecom services |

|

|

Bio-gas fuel |

Financial services |

|

|

Fertilizers |

Restaurant services |

|

|

18% |

Capital goods |

Hotel/ Lodges with tariff between INR 1000 and 5000 |

|

Industrial intermediaries |

||

|

Hair Oil |

||

|

Soap |

||

|

Toothpaste |

||

|

28% |

Air conditioner, Refrigerators |

Cinema tickets, Betting, Gambling, |

|

Hotel/ Lodges with tariff above INR 5000 |

||

|

28% + Cess |

Small cars (1% / 3% cess) |

|

|

Luxury cars(15% cess) |

Hope you all had an informative read.

To be continued.

CAclubindia

CAclubindia